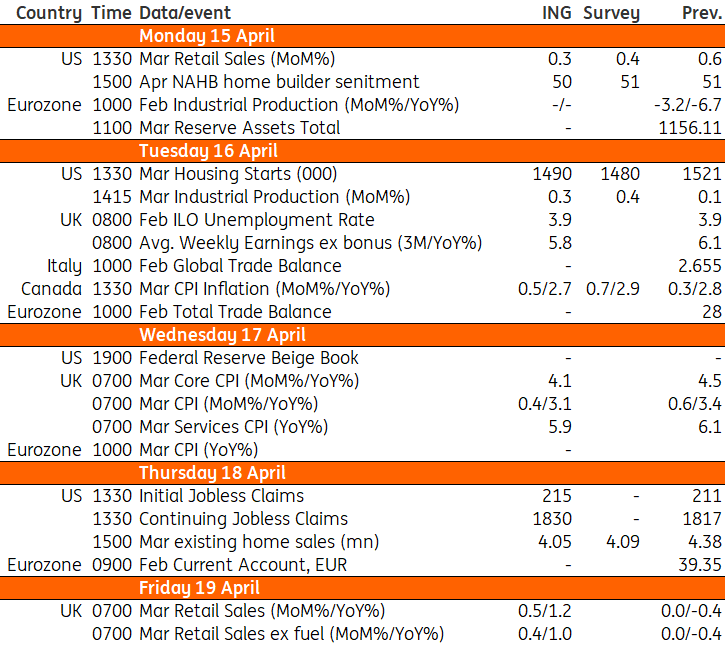

Key events in developed markets and EMEA next week

Retail sales and production data are next week’s focus in the US after unexpectedly strong inflation data pushed back the anticipated start date of the Fed easing cycle. We’ll also get services inflation and wage growth in the UK, which will help shape the debate on whether the BoE cuts rates in June or August.

Retail Sales in focus after sticky inflation data

With inflation and strong jobs confirming little prospect of an interest rate cut from the Federal Reserve before September, we expect a calmer period for markets over the coming week. The highlights in the US will be retail sales, industrial production and housing data. Retail sales is a nominal figure, so with inflation running hot our 0.3% month-on-month forecast implies that volumes will remain subdued. We have already had auto volume figures, which disappointed, while the weekly credit card numbers from the Bureau for Economic Analysis have been subdued and data from Opentable suggests restaurant dining has been weak. With loan delinquency rates on the rise and an increasing number of people making only the minimum payment on their loans, there is evidence of increased stress and this is likely to get worse in the near term with inflation running hotter than income growth, especially for those on social security.

An improvement in the ISM index suggests we should look for a decent increase in industrial production, but the rise in mortgage rates means that we expect weakness in housing transaction numbers. This feeds into retail sales given the strong correlation with home sales and retail activity tied to household appliances, furniture and furnishings and building supplies – when moving home people often want new items in their new property.

UK inflation and wage data in focus as investors weigh June rate cut

In contrast to the Federal Reserve, the Bank of England looks like it's still on track for a rate cut either in late spring or summer. The Bank has told us that the timing hinges on the next few releases of services inflation and wage growth, both of which we get next week and are set to show some further limited progress. Headline inflation should tick lower too, although this will be tempered by the recent rise in petrol prices.

Irrespective of the outcome, we think May's meeting is too early for a cut. However, a material downside surprise to next week's data – which we stress is not our base case – might convince the Bank to use that meeting as an opportunity to signal its preference for cutting rates in June.

For the time being though, we think an August start date is narrowly more likely, and that's because we think both the March and April services inflation figures could come in a little above BoE forecasts. Our new Fed call for a September rate cut also adds weight to the idea the BoE will wait slightly longer before cutting for the first time.

Key events in developed markets next week

Source: Refinitiv, ING

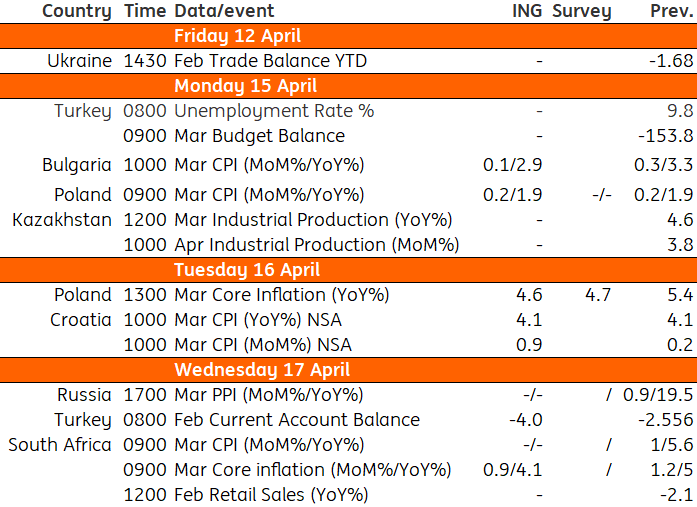

Key events in EMEA next week

Source: Refinitiv, ING

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.