July CPI and the real inflation story

The July CPI data indicated moderate price inflation and boosted optimism for a September interest rate cut, even though monetary inflation is on the upswing.

There were no big surprises in the July CPI data, with the numbers generally coming in as forecast. Markets tend to interpret “meeting expectations” as good news, even if the expectations weren't particularly good to begin with.

In this case, the numbers were akin to cold oatmeal. They weren’t great, but you can stomach them and gain some sustenance, especially if you are hoping for interest rate cuts.

July CPI by the numbers

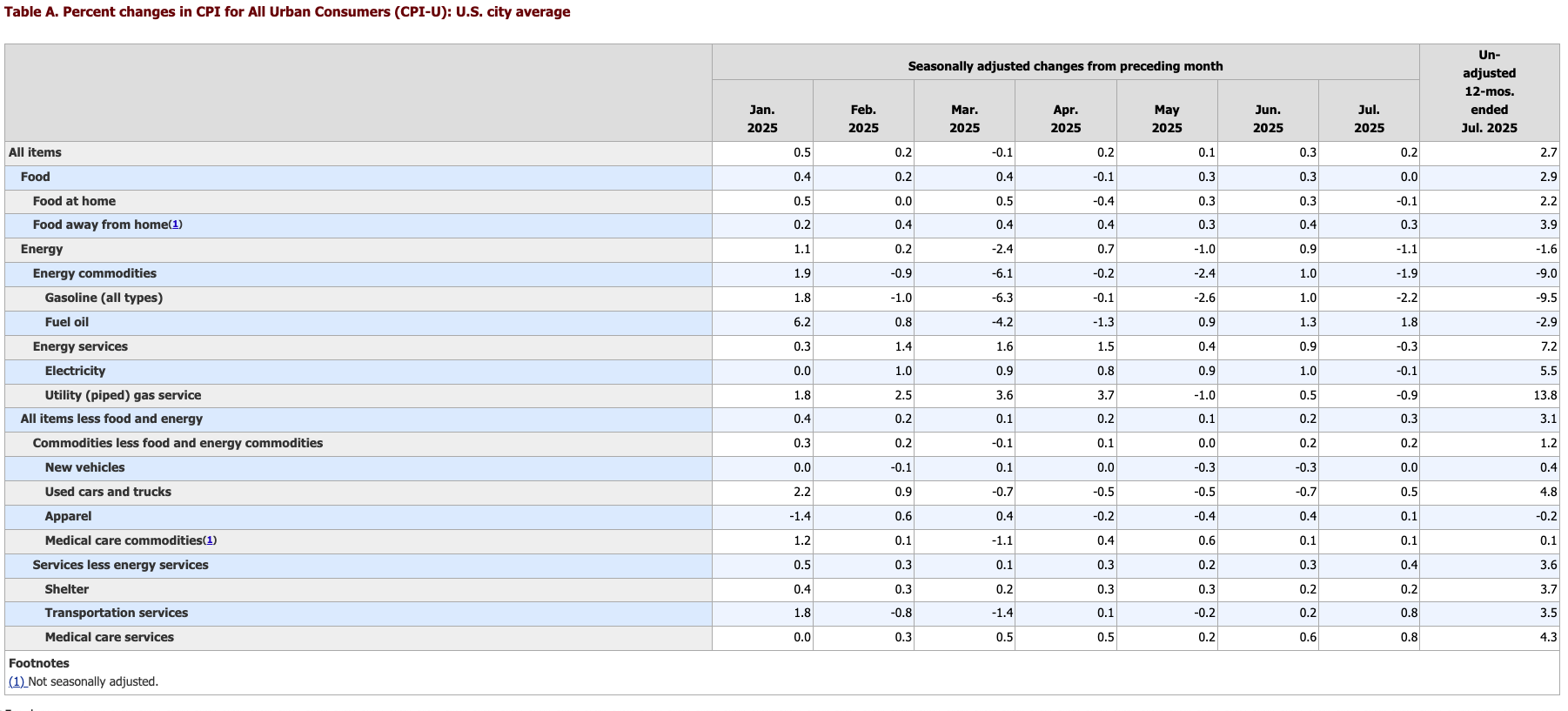

Price inflation rose 2.7 percent in July, the same rate reported in June, according to the BLS data. The expectation was for the headline annual number to tick up to 2.8 percent.

On a monthly basis, prices rose 0.2 percent. That was a tad cooler than June’s 0.3 percent reading and right on the forecast.

Excluding more volatile food and energy prices, core CPI rose 0.3 percent month-on-month, heating a tad compared to June’s 0.2 percent increase and hitting the forecast.

On an annual basis, core CPI rose 3.1 percent. That was up sharply from 2.9 percent in June. The expectation was for a 3.0 percent gain.

CNBC noted that, “Federal Reserve officials generally consider core inflation to be a better reading for longer-term trends.”

Well, that core number has remained stubbornly high for months. It dropped as low as 2.8 percent in March but began creeping up again in June.

Note that none of these numbers is close to the Fed’s mythical 2 percent target.

As you parse the data, keep in mind that the CPI doesn’t tell the entire story of inflation. The government revised the CPI formula in the 1990s so that it understated the actual rise in prices. Based on the formula used in the 1970s, CPI is closer to double the official numbers. So, if the BLS used the old formula, we’d be looking at CPI closer to 6 percent. And using an honest formula, it would probably be worse than that.

The recent massive revisions to the BLS employment data have also cast some doubt on the veracity of government number-crunching.

However, this is the formula the government uses, and it drives decision-making.

It is also important to note that a federal government hiring freeze has reportedly stretched the BLS thin, and the agency recently reduced data collection and expanded a process known as “imputation,” which uses modeling to fill in incomplete data. In April, the BLS announced it was “reducing sample in areas across the country” and suspended data collection in Lincoln, Nebraska; Provo, Utah; and Buffalo, New York.

Digging more deeply into the CPI data, we find that the falling energy prices once again helped pull the overall index lower. The energy index fell by -1.1 percent month-on-month, with gasoline prices dipping by -2.2 percent.

However, prices in most categories rose modestly. Shelter was once again a big driver of price inflation, rising by 0.2 percent since June. Other indexes that increased over the month include medical care, airline fares, recreation, household furnishings and operations, and used cars and trucks. Lodging away from home and communication were among the few major indices that decreased in July.

Market reaction

The markets read this as a positive CPI report. The CNBC headline trumpeted that prices rose “less than expected,” which generally wasn’t true. USA Today tells us that “inflation held steady.” CBS News said, “Inflation was cooler than expected.

Stock futures rose on the news, as did gold, as the perception of cooler-than-expected inflation ramped up hope for an interest rate cut.

Media outlets reported that tariffs don’t seem to have bled into consumer prices, at least not yet. CNBC summed it up this way.

“Tariffs did appear to show up in several categories. For instance, household furnishings and supplies showed a 0.7 percent increase after rising 1 percent in June. However, apparel prices were up just 0.1 percent and core commodity prices increased just 0.2 percent. Canned fruits and vegetables, which generally are imported and also sensitive to tariffs, were flat.”

Future market pricing seems to be leaning strongly toward a September interest rate cut. CME Group’s FedWatch increased the odds of a cut to 93.9 percent in September. The chance of an October cut also moved up from 55 percent to 67 percent.

The real inflation story

Everybody focuses on prices, but that only tells part of the inflation story. More precisely defined, inflation isn’t just rising prices. It is the increase in money and credit. One of the results of monetary inflation is price inflation.

Henry Hazlitt is best known for his brilliant book Economics in One Lesson. In another essay titled “Inflation in One Page,” he explained why using a more precise definition of inflation is crucial.

“Inflation is an increase in the quantity of money and credit. Its chief consequence is soaring prices.

“Therefore inflation—if we misuse the term to mean the rising prices themselves—is caused solely by printing more money. For this, the government’s monetary policies are entirely responsible.” (Emphasis added)

No matter how you choose to parse the CPI data, inflation is already increasing, and a rate cut will accelerate that trend.

After the last Fed meeting, Chairman Jerome Powell called the current monetary policy “modestly restrictive.”

This characterization is debatable.

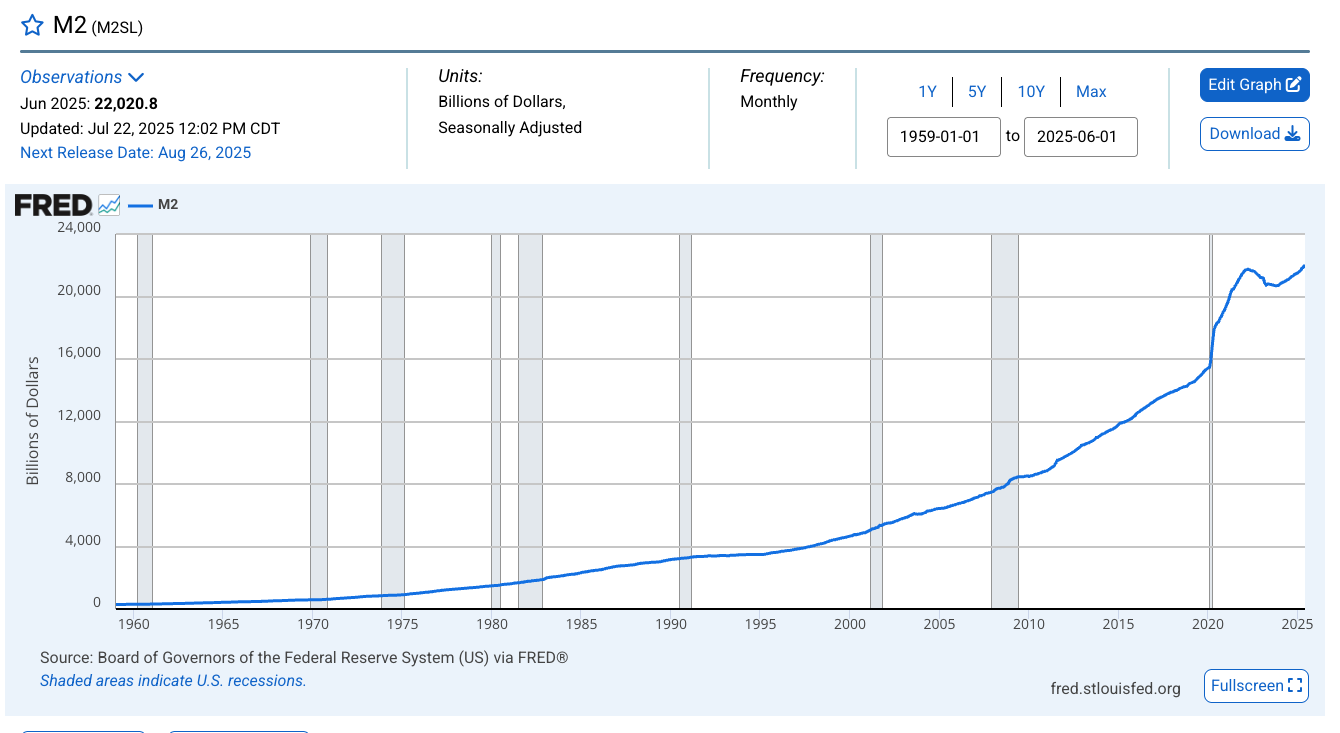

As of the end of June, the money supply had expanded by more than $600 billion since its low point in mid-2023.

As of June, the M2 money supply stood at $22 trillion and is above the peak reached during the pandemic.

We can’t overstate this fact: this IS inflation.

During the Fed’s inflation fight, the M2 money supply contracted. This is exactly what needs to happen to wring out inflation from the economy. The money supply bottomed a little over a year ago at $20.60 trillion.

That sounds like an impressive inflation fight, until you realize that the money supply would need to fall by at least another $3 trillion to get back to the trend of 2019. Clearly, that’s not the trajectory.

While the Federal Reserve tightened monetary policy enough to rein in rising prices, it never did enough to slay the inflation dragon. In fact, inflation (properly defined as an increase in the money supply) has been going up for over a year.

That means there is a plausible case for holding rates steady. You could even argue that rates should be higher.

On the other side of the coin, President Trump and those pushing for rate cuts can point to this CPI data and plausibly argue that price inflation remains muted. The tariffs have not impacted consumer prices significantly. And while you could parse the data and argue that price inflation is heating up, it remains cool compared to the numbers a year ago.

Meanwhile, the U.S. economy is buried in debt (incentivized by more than a decade of artificially low interest rates), and it really can’t function long-term in a higher-rate environment.

That means there is a plausible argument for rate cuts.

But even insists the Fed should cut rates based on the CPI, it's important to remember that this is actually a push to increase inflation.

Given the fact that the money supply is expanding, and financial conditions are loose from a historical standpoint, caution in cutting is warranted. Just taking the CPI at face value should signal caution. After all, none of the metrics are at the mythical 2 percent target.

However, President Trump and others pushing for rate cuts aren’t wrong either.

A higher interest rate environment will eventually crack the debt-riddled economy and pop the bubbles. The economy needs its easy money drug.

So, when you boil it all down, it appears the central bank needs to simultaneously keep rates higher for longer and cut rates. That’s quite a Catch-22.

To receive free commentary and analysis on the gold and silver markets, click here to be added to the Money Metals news service.

To receive free commentary and analysis on the gold and silver markets, click here to be added to the Money Metals news service.

Author

Mike Maharrey

Money Metals Exchange

Mike Maharrey is a journalist and market analyst for MoneyMetals.com with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.