Japan’s retail army is short the Dollar and betting Tokyo has a bigger plan

- Japanese retail traders have built a record dollar short largely by front-running official action near the low-to-mid 160s.

- Intervention may struggle to hold because retail profit-taking and importer demand would create fresh dollar buying below spot.

- The GPIF debate matters because even modest changes in foreign-asset hedging or allocation could give the yen a more durable flow story.

- Marine Day on Monday, July 20 creates a thin-liquidity intervention window, while a failure to act could leave USD/JPY vulnerable to a sharp short squeeze.

Japan’s retail army is short the Dollar

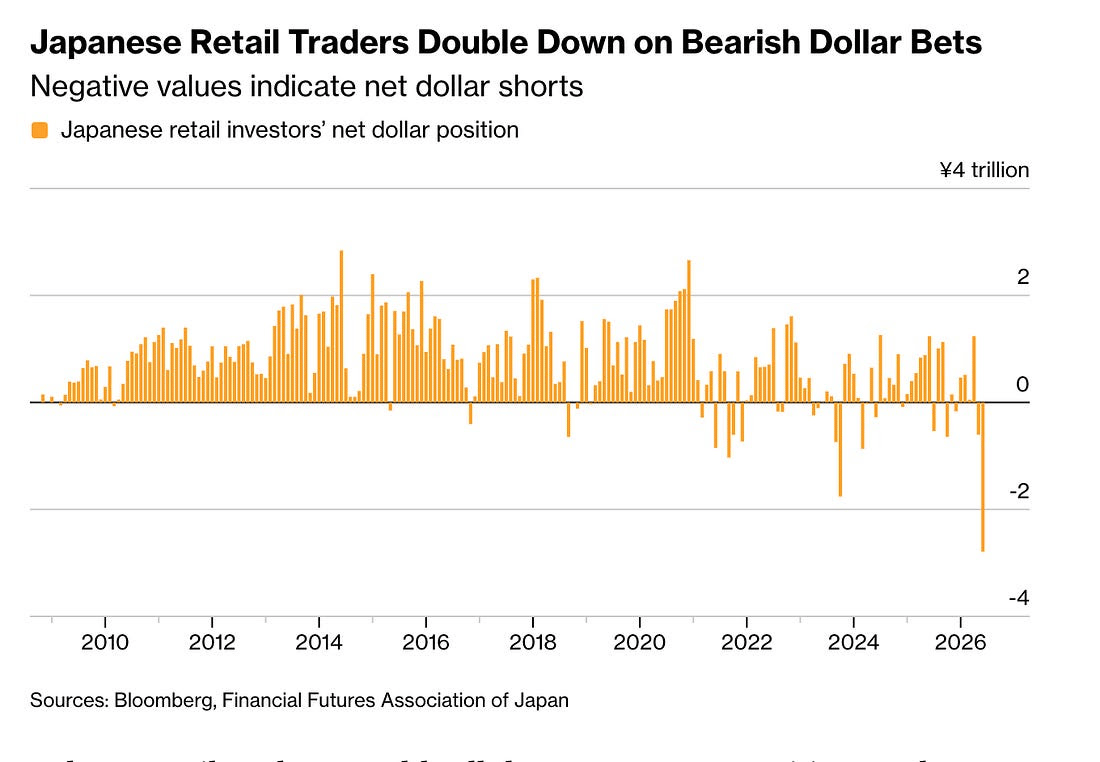

Japanese retail traders have built their largest net dollar short position since records began in 2008, putting one of the most crowded trades in global FX directly beneath USD/JPY.

According to Bloomberg’s Masaki Kondo ( and confirmed by the Financial Futures Association of Japan), net dollar shorts held by Japanese retail accounts more than quadrupled in June to ¥2.79 trillion, or roughly $17.2 billion. While some of those positions may sit against currencies other than the yen, the scale of open interest in USD/JPY leaves little doubt about where the main wager is concentrated.

This is intervention front-running, but not only in the old-fashioned sense.

Japanese retail traders know the rate differential still favours the dollar. They know the carry is painful. They also know Tokyo has already shown a willingness to spend heavily when the yen becomes politically uncomfortable.

The Ministry of Finance spent ¥11.73 trillion through May 27 supporting the currency. The operation knocked USD/JPY sharply lower, but the broader trend eventually reasserted itself as US yields remained high, the Bank of Japan stayed cautious and Japanese importers returned to buy dollars.

For policymakers, that episode underlined the limits of intervention.

For retail traders, it proved that a sudden official strike can still pay.

That is why the short position has continued to grow. Traders are not necessarily calling the end of the dollar cycle. They are betting that the Ministry of Finance will eventually deliver a sufficiently violent reversal to cover the carry and hand them a profitable exit.

Japanese retail accounts have always had a taste for fading extremes. They sell strength, buy weakness and lean against markets that appear to have travelled too far. With USD/JPY above 162 and official concern rising, the temptation to stand in front of the move has become almost irresistible.

The trade, however, becomes more interesting when the GPIF enters the frame.

Recent remarks from Japan’s finance minister have revived speculation that the Government Pension Investment Fund could review its portfolio if necessary. There has also been discussion around encouraging more household savings into domestic government bonds through tax-advantaged accounts.

Neither development amounts to a formal repatriation plan. The GPIF has not announced a wholesale retreat from foreign assets, nor is there evidence that Tokyo is preparing to force the pension giant into a dramatic currency shift.

But the direction of travel matters.

Japan’s persistent capital outflow has been one of the deeper forces weighing on the yen. Pension funds, insurers, households and corporations have spent years allocating abroad in search of yield and diversification. Intervention can shock the market for a day. A change in institutional behaviour can alter the flow for months.

That is why the GPIF debate deserves attention.

With assets of roughly ¥250 trillion and a large allocation to foreign bonds and equities, even a modest change in hedging behaviour or portfolio composition could create meaningful yen demand. The market would not need a complete overhaul. It would only need evidence that Japan is beginning to turn part of its domestic capital pool back toward home markets.

That possibility gives the retail short a second layer.

The first layer is familiar: wait for the Ministry of Finance to sell dollars and force USD/JPY lower.

The second is more structural: position for a policy shift that changes the capital-flow backdrop behind the yen.

That does not mean retail traders have discovered a hidden master plan. It means the market is beginning to wonder whether Tokyo is finally looking beyond one-off intervention.

The distinction matters because the current positioning could blunt the impact of another official operation.

Bloomberg cited Hideki Shibata of Tokai Tokyo Intelligence Laboratory, who noted that retail traders would likely buy dollars to close profitable shorts if intervention drives USD/JPY lower. Japanese importers would also be waiting beneath the market to secure dollars at better levels.

That creates a natural rebound mechanism.

Tokyo sells dollars. USD/JPY falls. Retail traders take profit. Importers step in. The market starts climbing back.

This is why intervention alone may struggle to produce lasting results. The official order can punch a hole through the market, but commercial demand and short covering can quickly begin filling it.

The GPIF angle changes that calculation. A credible shift in institutional flows would make the move harder to dismiss as another temporary ambush. It would give the yen something intervention has repeatedly lacked: follow-through.

There is also a near-term calendar wrinkle.

Monday, July 20 is Marine Day, a Japanese national holiday. Domestic participation will be lighter, liquidity thinner and the Asian session potentially more vulnerable to a large official order.

Marine Day is not the reason Japanese retail traders built the record short. The position was already substantial before the holiday came into view. But the timing is useful.

Friday, July 17 is the final positioning session before the long weekend. Monday is the actual holiday-liquidity window.

The Ministry of Finance would authorize any intervention, with the Bank of Japan executing the order on its behalf. In thinner conditions, the same amount of dollar selling could produce a larger move than it would during a normal Tokyo session.

That may be enough to keep some retail traders in the trade despite the carry bleed.

The real risk, however, is what happens if Tokyo does nothing.

With retail accounts already carrying the largest dollar short in the history of the data, a clean break above the low-to-mid 160s could force a disorderly round of short covering. Traders waiting for intervention would suddenly become dollar buyers, adding fuel to an already rising market.

The trade is therefore tightly wound.

Below USD/JPY sits the risk of official selling, importer demand and the possibility of broader domestic repatriation.

Above it sits a record short position that could become its own accelerant.

Japanese retail traders are not simply betting on a stronger yen. They are betting that Tokyo is nearing the point where warnings, intervention and domestic capital policy begin pulling in the same direction.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.