Japanese industrial production strengthens as Retail Sales disappoint

March activity data was a mixed bag in Japan. Weak manufacturing weighed on growth in the first quarter of the year, but we think that consumption is likely to improve on the back of a healthy labour market.

Despite a rebound for IP, Manufacturing output contracted in the first quarter

Industrial production saw stronger-than-expected gains at 3.8% month-on-month seasonally adjusted in March (vs 3.3% market consensus). Even so, this isn't enough to fully offset the declines of the previous two months (-0.6% in February, -6.7% in January). The comparison contracted -5.3% three-month on three-month sa in March (vs 1.1% in December), and weak manufacturing activity could have had a negative impact on first quarter GDP.

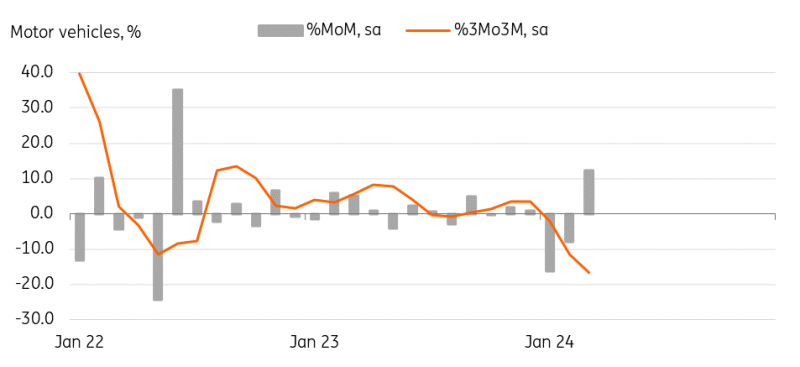

However, as production stoppages due to the safety scandal issue have normalised since March, we believe that there could be a few more months of catch-up production. Production output forecasts for April and May also rose 4.1% month-on-month sa and 4.4% each, which suggests that the growth momentum in manufacturing activity is likely to continue in the second quarter. By item, motor vehicle production rebounded 9.6% and electronic parts and devices also rose 9.2%.

Motor vehicle production sets to normalise over the next few months

Source: CEIC

Retail Sales fell -1.2% MoM sa in March (vs 1.7% in February, -0.2% market consensus)

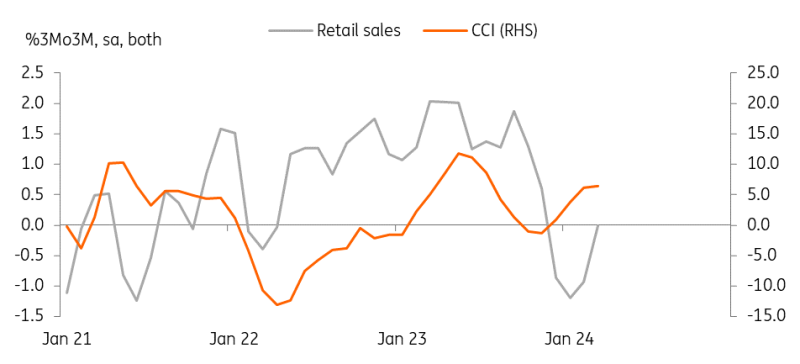

Disappointingly, retail sales dropped more than expected in March, but February retail sales were revised up to 1.7% from their previous 1.5%. Quarterly growth therefore improved from the previous quarter. Service activity remained strong in the first quarter of the year, and overall private consumption should positively contribute to GDP in that period. By item, motor vehicle sales rebounded 2.5% after three months of decline. Food (0.6%) and fuel (5.7%) consumption also rose sharply.

On the back of positive consumer sentiment and tight labour market conditions, we continue to believe that household consumption should improve further in the current quarter.

Retail Sales improved in 1Q24

Source: CEIC

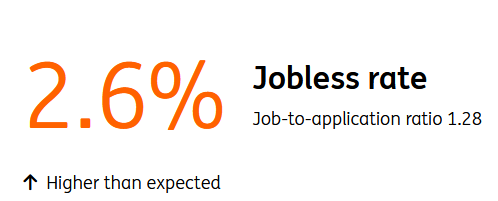

Labour market conditions remain healthy in March

The unemployment rate remained at 2.6% for a second month, slightly shy of the maket consensus of 2.5%. The job-to-application ratio rebounded for the first time in 17 months. We believe the recovery of auto outputs and ongoing solid demand for services are both likely to support healthy labour market conditions. Combined with the strong wage negotiation results, the tight labour maket will boost private consumption and support sustained inflation.

GDP forecasts

Based on monthly activity and survey data, we expect first quarter GDP for 2024 to make a small gain of 0.1% quarter-on-quarter sa (vs 0.1% in the final quarter of 2023) Manufacturing should be the main drag for first quarter GDP but we expect to see solid recoveries in private spending and investment. However, once auto production normalises over the next few months, growth is expected to accelerate in the current quarter.

Read the original analysis: Japanese industrial production strengthens as Retail Sales disappoint

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.