Is the risk rally about to roll over as consolidation sets in ahead of payrolls? [Video]

![Is the risk rally about to roll over as consolidation sets in ahead of payrolls? [Video]](https://editorial.fxstreet.com/images/TechnicalAnalysis/ChartPatterns/Candlesticks/high-resolution-stock-exchange-evolution-panel-55741958_XtraLarge.jpg)

Market Overview

The initial moves of a recovery in risk appetite have shown signs of stalling in the past 24 hours. Perhaps it is simply down to consolidation ahead of today’s Non-farm Payrolls data, but the momentum of the recovery from earlier this week has lost its impetus. This comes as consolidation begins to set in on bond yields (a slight renewed flattening of the US yield curve since Wednesday’s close) and safe have assets such as the yen and gold begin to find their feet again. The narrative on the Coronavirus has not changed. The virus continues to spread at an accelerating rate as do the number of deaths (now confirmed at 636). The PBoC is promising measures to help support the economy, and whilst analysts are slashing forecasts of growth in Q1, the expectation remains that by Q3 there will be renewed activity which will mitigate much of the impact. Looking across markets, there is still a bias to buy the dollar. A hybrid of safety and also a degree of economic resilience has pulled the Dollar Index to test four month highs. The China Trade Balance for January is still yet to be announced and is expected to be fairly negative +$38.6bn exp, (+$46.8bn in December) with Chinese exports -4.8% exp (+7.6% in December) and Chinese imports -6.0% exp (+16.3% in December). Once out, this data could drive sentiment this morning. However, as the session goes on attention will turn to the January US jobs report. After the ADP numbers came in hot on Wednesday, another indication that the start of 2020 has been decent. A positive surprise would add fuel to the dollar strength but also with no prospect of any change to Fed policy (in the next few meeting at least), aid a risk recovery too.

Wall Street closed mildly higher as the S&P 500 hit all-time highs +0.3% at a close of 3345. US futures are tentatively lower today -0.1% which has seen a mixed session in Asia (Nikkei -0.2% and Shanghai Composite +0.3%). In Europe, there is a slip back in early moves with the FTSE futures -0.2% and DAX futures also -0.2%. In forex, there is a mild bias back towards safe havens again today with JPY performing well and the commodities currencies (AUD and NZD) weaker. In commodities, there is consolidation on gold and oil.

The US labor market report dominates the economic calendar today. The US Employment Situation report is at 1330GMT and is expected to see the headline Non-farm Payrolls grow by 160,000 jobs in January (+145,000 in December). Average Hourly Earnings are expected to grow by +0.3% on the month which would improve the year on year wage growth to +3.0% (+2.9% in December). US Unemployment is expected to remain at 3.5% again (3.5% in December).

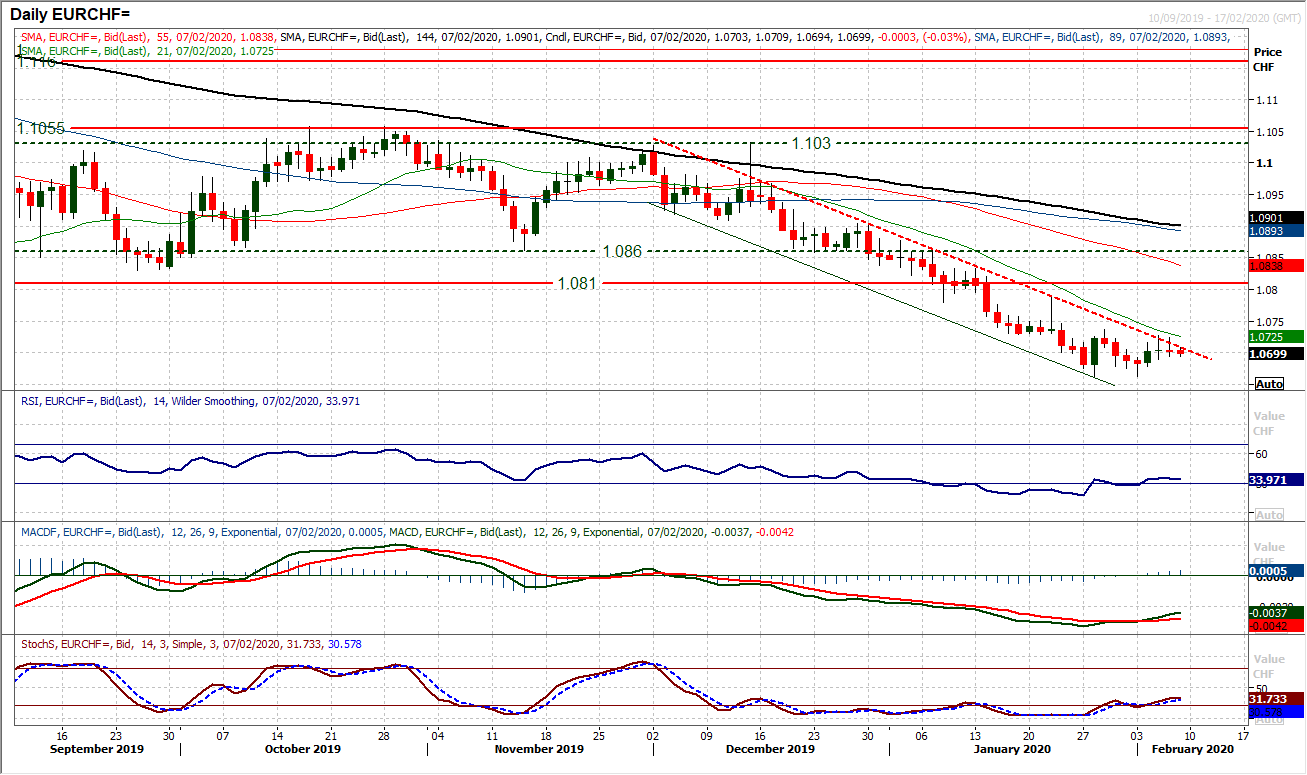

Chart of the Day – EUR/CHF

We have discussed the safe haven bias on forex majors of recent weeks during the Coronavirus. However, there are signs that the market is just beginning to switch out of safety. This is reflected in what looks to be a slowing of the negative momentum on Euro/Swiss. The cross has been in a tight downtrend channel for almost two months now, but in the past few sessions there have been marked positive divergences forming across momentum indicators. The RSI is now around five week highs (confirmation of a recovery would be the RSI closing above 40). Furthermore, the MACD lines have bull crossed and are now advancing. These all look to be lead indicators for a potential rally on EUR/CHF. There has been a degree of consolidation with some very neutral, small-bodied candles on Wednesday and Thursday, but the very well-defined downtrend is now being tested. Watch the 21 day moving average (today at 1.0725) which has been flanking the decline since mid-December and if broken would again be a positive signal. For a shift in the outlook there would need to be a move above initial resistance at 1.0735. This would be a small base pattern up from the lows at 1.0662 and imply a recovery back towards the key 1.0810 old floor. The hourly chart shows initial support at 1.0690.

WTI Oil

The prospect of a recovery was just put on ice yesterday as what had looked to be a second consecutive positive candle was dragged back into the close. A false start in the rally. However, the strong downtrend of the past few weeks has now been broken, whilst momentum indicators are threatening recovery signals. The importance of the near term resistance now around $52.15 is key. This pivot area would mark the completion of a small base pattern (which would then imply a recovery towards the more considerable resistance around $54.35/$54.75) if the bulls can decisive clear it. Once more, also there will be a focus on $50.50/$51.00 as support. A decisive breach would defer the near term recovery hopes and put pressure back on the recent low at $49.30.

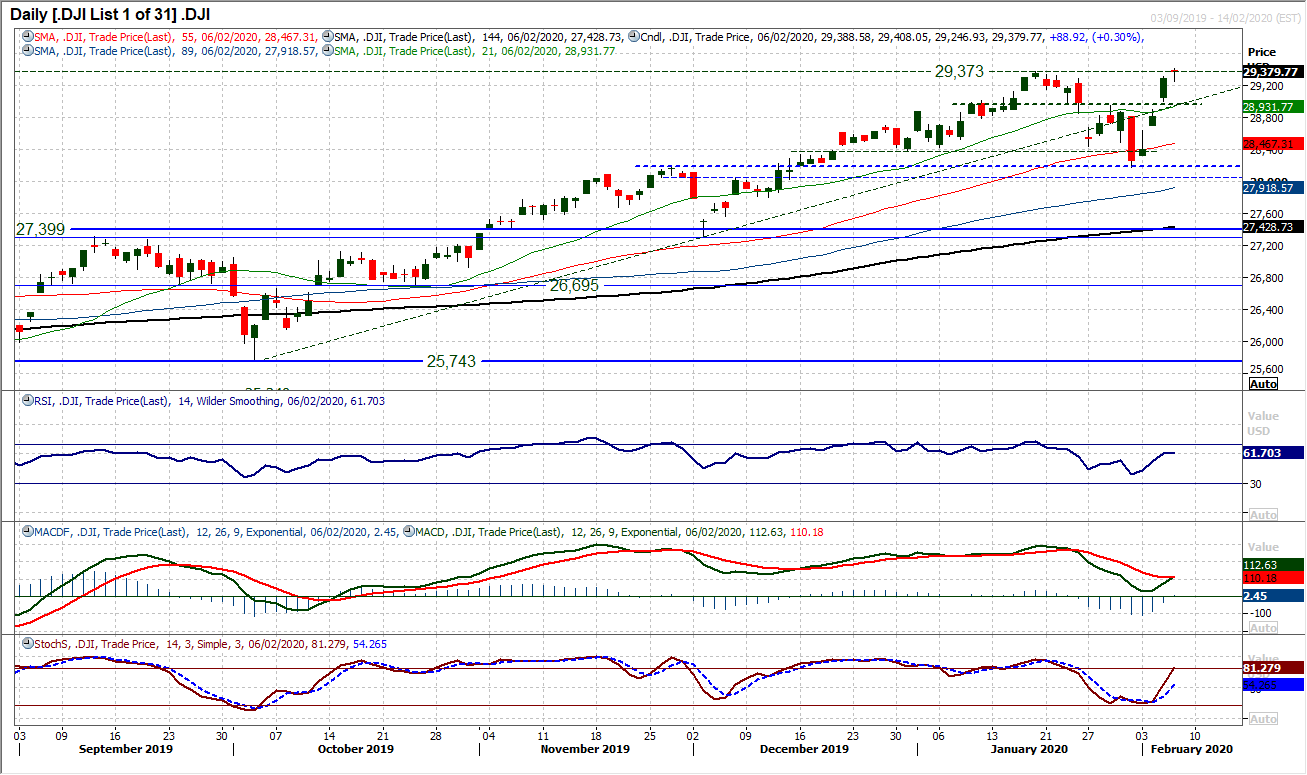

Dow Jones Industrial Average

Another positive session has taken the Dow to a new all-time high. However, after the positive candlesticks of previous sessions this week, Thursday’s move was a little muted. Whilst the bulls have been running decisively higher, where filling the opening gaps has not even been contemplated, yesterday’s gap fill could harbour a slowing of the buying impetus. At least, on a very near term basis. Furthermore, the market only crept meekly to an all-time high (by just 6 ticks). Although daily momentum remains very positive and seemingly with upside potential, there could be the prospect of a near term retreat brewing. The hourly chart shows a little fatigue hinting on hourly MACD and hourly RSI both just fading slightly. Essentially, this is once more a very strong looking market and the outlook remains positive, but within this, weakness is still a chance to buy. There is a near term pivot band of support 28,950/29,000 which is an area the bulls will be looking at initially. We anticipate further all-time highs will be seen and a close decisively clear opens 30,000.

Author

Richard Perry

Independent Analyst