Is extending loan maturities an effective way to improve access to home ownership?

The British example tends to suggest otherwise. Its impact on monthly payments remains modest compared to that of interest rates and rising property prices, and is offset by the higher total cost of the loan. In addition, longer loan maturities are likely to fuel the rise in property values.

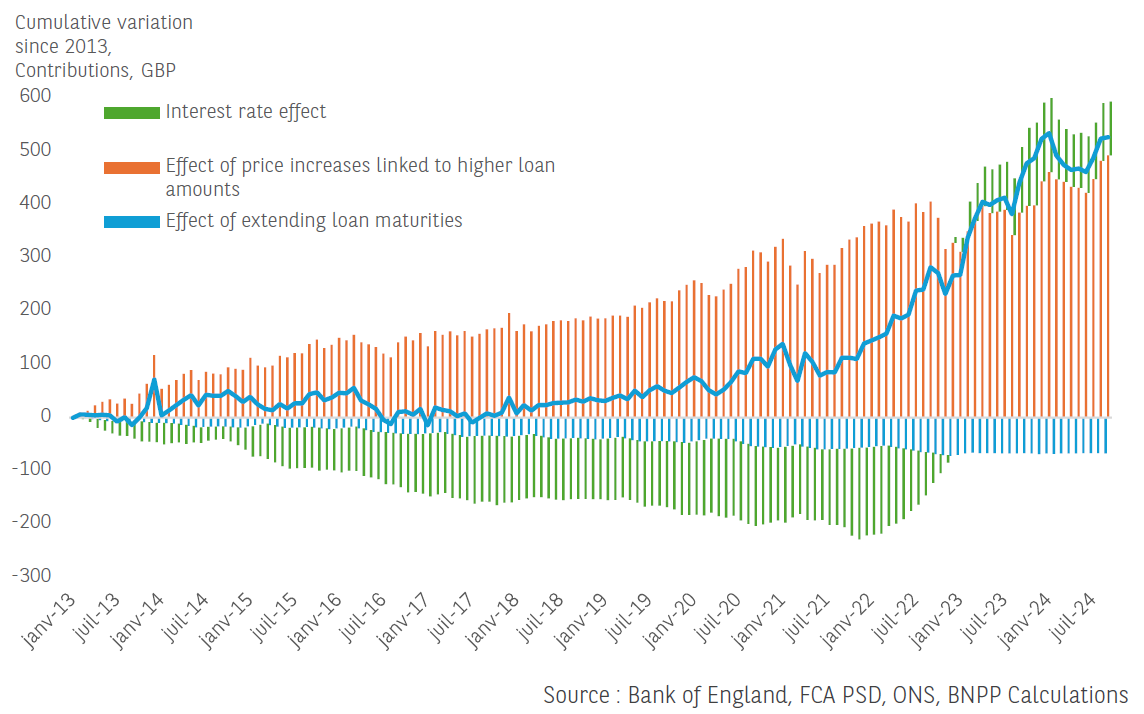

Changes in average monthly mortgage payments in the United Kingdom

Over the past fifteen years, the mortgage maturities in the UK have been significantly extended. An increasing proportion of new mortgages now have terms barely imaginable in France, where mortgages are limited to 25 years, in accordance with the rules laid down by the Haut Conseil de Stabilité Financière [High Council for Financial Stability] (HCSF) in a decision of 2021[1]. In 2024, over 50% of new UK mortgages were taken out with terms of more than 30 years, compared to just 10% in 2005. Mortgages with a term of 40 years or more represented nearly 10% of new loans in the first quarter of 2024.

At first glance, extending maturities seems an attractive idea for facilitating access to home ownership. All things being equal, spreading instalments over a longer term reduces monthly payments, which improves households’ ability to meet these payments and can thus help them access credit. According to our calculations, by keeping the interest rate and the average amount borrowed constant, extending maturities would have reduced the average monthly payments for new loans[2] by around 10% between January 2013 and September 2024. In practice, these monthly payments remained relatively stable between 2013 and 2019, as the effects of lower interest rates, longer maturities and higher amounts borrowed due to higher property prices have, on average, offset each other. At the same time, the average UK household benefited from an increase of around 23% in its gross disposable income, and its affordability rate at loan origination fell to 18% on average in 2019 (compared to 20.3% on average in 2013).

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.