Investment Theme – Commodity currencies struggle on faltering Trumpflation trade

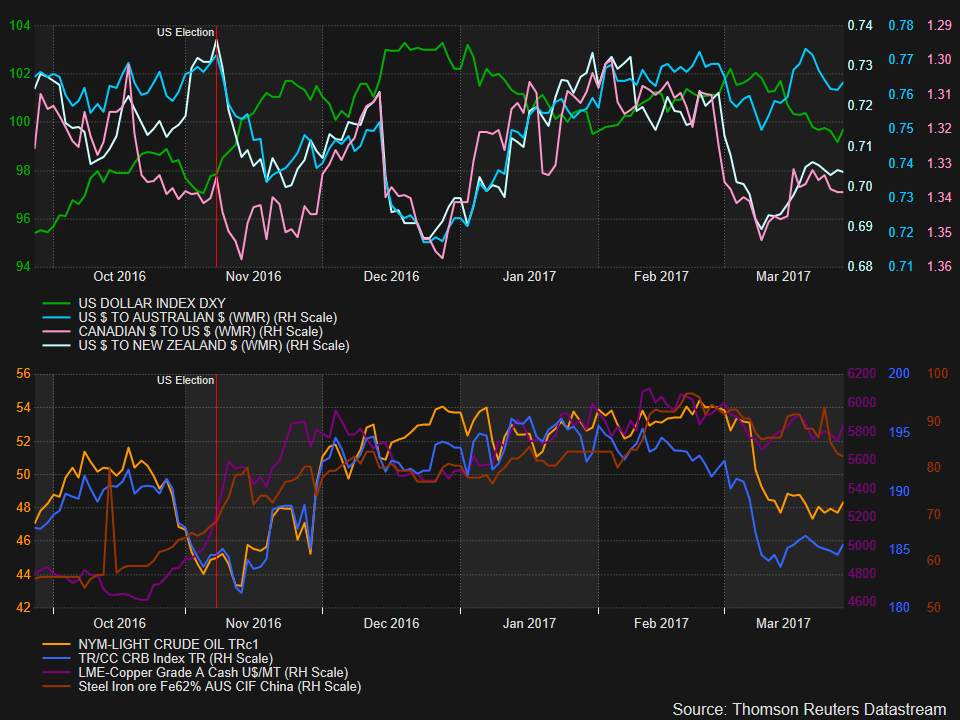

The pullback in the US dollar over the past two weeks has brought little relief to commodity-linked currencies, as their resilience against the resurgent greenback had been underpinned by the Trumpflation trade, which came close to being fully unwound this week. Currencies such as the Australian, New Zealand and Canadian dollars have come under pressure in the past week on fears that the reflation trade inspired by Trump has come to an end.

Market expectations that Donald Trump’s presidency would usher in an era of big infrastructure spending and large tax cuts, boosting economic growth and inflation in the US, had lifted commodity prices in addition to equities and the dollar. Commodity prices had risen sharply on expectations that higher infrastructure spending and stronger growth from tax reforms would raise demand for metals such as copper and iron ore, as well as for energy commodities.

The Australian dollar posted gains of about 8% between December and February as the rally in iron ore prices gathered pace. The aussie has a strong positive correlation with iron ore as Australia is a major exporter of metal resources. Other metal prices like copper are also up sharply since the US election, with increased demand from China adding further support.

However, more recently there have been signs that Chinese stockpiles are rising, indicating a possible glut being formed. This has weighed on the aussie, preventing it from advancing beyond the critical resistance area around $0.7750. While a more neutral Reserve Bank of Australia has provided some support to the Australian dollar, future gains will depend on whether or not a fiscal stimulus in the US will materialize and how well metal demand from China holds up. Despite the recent correction though, the aussie looks set to end the first quarter of 2017 with gains of 6% against the US dollar.

The New Zealand dollar isn’t as sensitive to metal prices but has sharply pared its year-to-date gains following the deterioration in risk sentiment. But other fundamentals have also been driving the kiwi lower, namely, the renewed weakness in dairy prices and a more dovish Reserve Bank of New Zealand. The kiwi is on track to end the quarter around 1.5% firmer against its US counterpart.

Meanwhile, the oil-linked Canadian dollar has fared even worse as the crude oil rally has stumbled and fears of trade tariffs by the Trump administration have also hurt the loonie. The output deal agreed by OPEC and some non-OPEC countries has yet to achieve its objective of rebalancing the market and it’s looking increasingly likely that it will have to be extended beyond the initial six month period in order to have a more substantial effect. Part of the problem has been rising production from the US. The new administration’s more relaxed policies on new drillings is further dampening the outlook. Without a fresh upside push in oil prices, the loonie is unlikely to divert from its current neutral bias and will end the quarter little changed against the US currency.

On a broader level, commodity prices have now completely erased the post-election gains. The Thomson Reuters/Core Commodity CRB index, which rallied by 6% immediately after Trump’s win, is now back to the level it was prior to the election. Whether or not the bull market will return for commodities depends on the success of President Trump’s pro-growth policies as well as on the condition that growth in trouble spots such as the Eurozone and Japan continues to gather momentum. However, a potential downside from a major fiscal boost in the US is that it would lead to more aggressive tightening by the Fed and a resumption of the dollar rally, and this would likely cap significant gains in commodity prices.

Author

Mr Boyadjian graduated from the London School of Economics in 1999 with a BSc in Business Mathematics and Statistics. Following graduation, he joined PricewaterhouseCoopers in the Business Recoveries team, where he was responsibl