Indian Rupee rebounds from record lows: Relief rally or real reversal?

The Indian Rupee has rebounded from the all-time low against the US Dollar, helped by coordinated action by the Reserve Bank of India and the government to attract foreign inflows.

The measures already offered some support to the Rupee and suggest that the latest sell-off may be finding a floor. However, the package doesn’t fully solve the external pressures that sent the Indian currency above 97.00 per Dollar.

The question here is whether this recovery is just relief or the beginning of a full reversal.

RBI steps in to defend embattled Rupee

The RBI announced that it was expanding the universe of “specified securities” under the Fully Accessible Route (FAR), which allows non-residents to invest in specific Government of India securities (G-Secs) without any quantitative limits. It now includes Sovereign Green Bonds as well as all new issuances of 15-, 30-, and 40-year tenor G-secs.

In addition, Foreign Portfolio Investors (FPIs) investing through the General Route will no longer be required to comply with short-term investment limits, security-wise limits, and concentration limits. The RBI has also merged the earlier sub-categories of investment limits – “general” and “long-term” – into a single consolidated limit for both Central and State G-Secs.

In simple terms, the RBI is making it more attractive for foreign investors to buy Indian assets.

Government scraps tax on overseas bond investors

Besides the RBI, the government has also taken steps to facilitate foreign capital inflows. Namely, it has exempted foreign investors from income tax on any interest or capital gains. The benefit is applicable retrospectively from the beginning of the current tax year, April 1, 2026.

The RBI also decided to double the limits for investment by Non-Resident Indians (NRIs) and Overseas Citizens of India (OCIs) in equity instruments traded on the stock market without SEBI registration from 5% to 10%. The facility extends to all individual Persons Resident Outside India (PROIs). Moreover, the central bank raised the combined investment limit for all such overseas investors from 10% to 24% of the company's paid-up capital.

RBI offers a concessional USD-INR swap facility

The RBI also operationalised its concessional US Dollar-Rupee swap facility to support overseas foreign currency borrowings (OFCBs) by banks and external commercial borrowings (ECBs) by Public Sector Undertakings (PSUs). Furthermore, the RBI will bear the full hedging cost of fresh 3-5 year Foreign Currency Non-Resident (FCNR) deposits mobilised by an authorised bank.

All these measures addressed key concerns – improving capital flows and shore up forex reserves. RBI Governor Sanjay Malhotra said during a press conference on June 5 that this will allow for a much better Balance of Payments (BoP) this year than what would have been otherwise, easing pressure on the domestic currency.

"Overall, these steps are incrementally positive for India’s balance of payments and could lift market sentiment, providing near-term support to INR,” said analysts at OCBC in a research note.

Will these measures be enough?

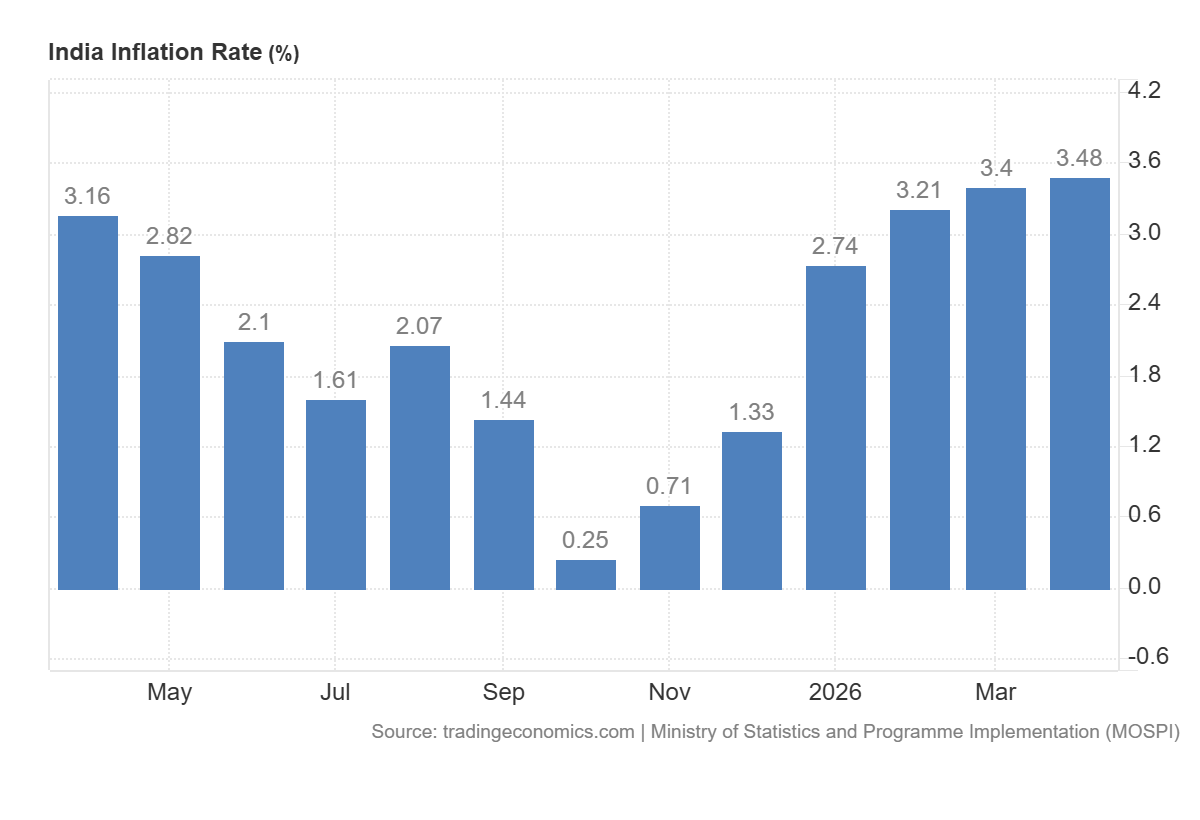

The conflict in West Asia and the prospects of below normal monsoon pose risks to inflation this year. Going forward, retail inflation is expected to rise as higher energy prices partially pass through to domestic pump prices.

Taking this into consideration, the RBI revised up CPI inflation forecast for FY27 to 5.1% from 4.6% earlier and core inflation (excluding food and fuel) to 4.7% from 4.4% earlier. Despite the upwardly revised figures, these remain well within the RBI’s target band of 2% to 6%.

On growth, the RBI noted that the economy has held up well since the start of the conflict, with both private consumption and investment demand showing resilience. However, the outlook remains clouded due to elevated energy prices and supply chain disruptions.

Relief, but not out of danger

Even though growth risks are tilted modestly to the downside, the likelihood of aggressive rate hikes appears limited as inflation is expected to remain within the RBI’s tolerance band.

The expected increase in foreign inflows due to steps taken by the RBI and the government suggests that the depreciation pressure on the Indian Rupee should be limited.

That said, there are some factors that the RBI and the Indian government can’t control. A prolonged closure of the Strait of Hormuz could lead to Oil prices rising even further, worsening the current account deficit. Effects from El Niño could also result in higher consumer prices and trigger a fresh leg down in the Indian Rupee.

The Rupee may have won the latest battle, but the war isn’t over.

Indian Rupee FAQs

The Indian Rupee (INR) is one of the most sensitive currencies to external factors. The price of Crude Oil (the country is highly dependent on imported Oil), the value of the US Dollar – most trade is conducted in USD – and the level of foreign investment, are all influential. Direct intervention by the Reserve Bank of India (RBI) in FX markets to keep the exchange rate stable, as well as the level of interest rates set by the RBI, are further major influencing factors on the Rupee.

The Reserve Bank of India (RBI) actively intervenes in forex markets to maintain a stable exchange rate, to help facilitate trade. In addition, the RBI tries to maintain the inflation rate at its 4% target by adjusting interest rates. Higher interest rates usually strengthen the Rupee. This is due to the role of the ‘carry trade’ in which investors borrow in countries with lower interest rates so as to place their money in countries’ offering relatively higher interest rates and profit from the difference.

Macroeconomic factors that influence the value of the Rupee include inflation, interest rates, the economic growth rate (GDP), the balance of trade, and inflows from foreign investment. A higher growth rate can lead to more overseas investment, pushing up demand for the Rupee. A less negative balance of trade will eventually lead to a stronger Rupee. Higher interest rates, especially real rates (interest rates less inflation) are also positive for the Rupee. A risk-on environment can lead to greater inflows of Foreign Direct and Indirect Investment (FDI and FII), which also benefit the Rupee.

Higher inflation, particularly, if it is comparatively higher than India’s peers, is generally negative for the currency as it reflects devaluation through oversupply. Inflation also increases the cost of exports, leading to more Rupees being sold to purchase foreign imports, which is Rupee-negative. At the same time, higher inflation usually leads to the Reserve Bank of India (RBI) raising interest rates and this can be positive for the Rupee, due to increased demand from international investors. The opposite effect is true of lower inflation.

Author

Haresh Menghani

FXStreet

Haresh Menghani is a detail-oriented professional with 10+ years of extensive experience in analysing the global financial markets.