India MPC cuts repo rate by 75 bps, reverse repo rate by 90 bps

The enormous liquidity injected by central banks seems to be beginning to pump asset prices, especially equities. The Dow has seen the largest 3 day surge in 90 years. The Dow rallied another 6.4% overnight and has recovered 4300 pts from recent lows. This is despite a record rise in US jobless claims reported yesterday to 3.28mn against expectations of 1.5mn. (2 weeks earlier jobless claims were at 50 year lows).

The finance minister yesterday announced a Rs 1.7lakh cr stimulus to help the economy tide over the crisis. The stimulus includes food security measures and direct cash transfers targeted at lower income groups.

Like other major global central banks, RBI today went with emergency rate cut of 75 bps and reduced reverse repo by 90 basis points to make it unattractive for banks to park funds with RBI. Launch of Tltro worth 25000 crore, 1% reduction In CRR and raising MSF to inject more liquidity will be an additional boost to stimulate the economy.

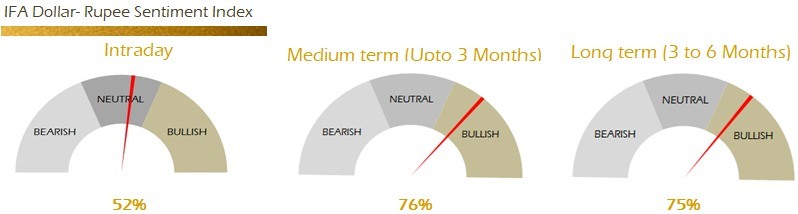

Strategy: Exporters are advised to hold. Importers are advised to go for back to back hedging or through RR option strategy (Buy Call, Sell Put). The 3M range for USDINR is 73.00 - 77.00 and the 6M range is 72.0 – 78.00 considering the panic situation amid coronavirus spread.

Author

Abhishek Goenka

IFA Global

Mr. Abhishek Goenka is the Founder and CEO of IFA Global. He pilots the IFA Global strategic direction with a focus on relentlessly improving the existing offerings while constantly searching for the next generation of business excellence.