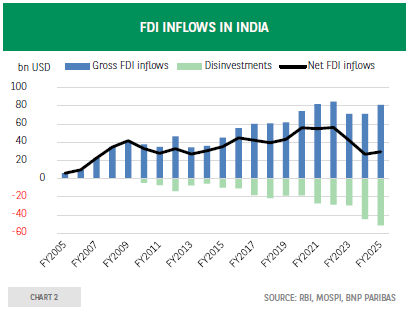

India attracts FDI but fails to retain it

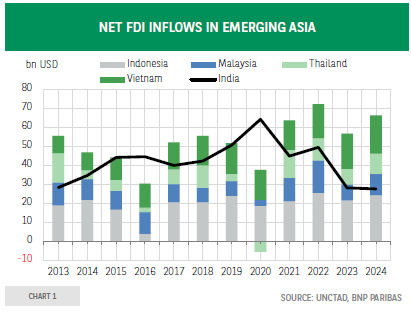

Asia is the leading recipient of foreign direct investment. East and South Asia is the leading recipient of foreign direct investment (FDI) among emerging countries (59.9% of the total in 2024), a level commensurate with their weight in the global economy. According to UNCTAD, apart from China and Singapore (a financial centre through which capital transits), India, Indonesia and Vietnam were the main recipients of FDI in emerging Asia in 2024 (Chart 1).

While FDI inflows into Southeast Asia have been higher on average since 2021 than in the 2016–2019 period, they have declined in China and India. As a share of GDP, net FDI inflows to India (non-resident FDI inflows minus disinvestment) reached only 0.7% of GDP in 2024, the lowest level since 2012 (they stood at 4.2% of GDP in Vietnam). This decline is all the more surprising given that, according to UNCTAD, the value of greenfield FDI projects announced in the country has been rising sharply since 2022.

India, a major recipient of gross FDI, is unable to retain it. Between 2017 and 2024, gross FDI inflows into India increased by a factor of 1.3, while disinvestments increased by a factor of nearly 2.9 (Chart 2). Foreign companies sold their assets or repatriated their earnings without reinvesting them in the country.

Neither the deterioration of the economic environment nor the unstable political environment is behind this phenomenon. Excluding the pandemic period, real GDP growth has been robust (higher than the growth seen in Southeast Asian countries), economic prospects have been favourable and macroeconomic risks have been contained.

The disinvestment is due to the business environment and structural constraints weighing on the development of foreign companies in India. Since 2017, infrastructure quality has improved significantly, but corruption, which was already high, has increased and governance is fragile.

India is characterised above all by a much more rigid labour market than in Southeast Asia. The labour law reform (adopted in 2020), which aimed to liberalise the labour market, has still not been implemented and may not be implemented before 2026 (at best). Furthermore, land acquisition remains highly problematic and is a barrier to business establishment and development.

The short-term outlook depends on reforms. FDI flows from China are expected to remain low for the foreseeable future, given the complex political relations between China and India. US investment (14.9% of gross FDI received) could be hampered by the tightening of US trade policy. Investment from the European Union (15.2% of FDI), on the other hand, should accelerate with the signing of a free trade agreement (expected by the end of the year). The challenge for India is to implement reforms that offer more favourable conditions for foreign companies in order to encourage them to set up long-term operations.

In Southeast Asian countries, in the short term, FDI trends will depend on bilateral trade negotiations with the US. “Connector” countries should continue to benefit from Chinese FDI, provided that they are not taxed much more than other countries that supply the US.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.

![How Wall Street rigs the game [Video]](https://editorial.fxsstatic.com/images/i/market-chaos-01.jpg)