How sensitive are emerging markets to rising yields?

Summary

In recent weeks, the theme of reflation has dominated global financial markets. With inflation expectations firming, U.S. Treasury yields have spiked. While the rise in Treasury yields should be interpreted as market participants becoming more confident in the recovery prospects of the global economy, higher yields have also resulted in elevated financial market volatility over the past few weeks, particularly within the emerging markets. The rise in yields has drawn comparisons to the 2013 Taper Tantrum, an episode where emerging market assets sold off significantly amid a sudden push higher in U.S. Treasury yields. There are some key differences between the recent rise in yields and the Taper Tantrum episode, however, and while Fed monetary tightening is likely still far off, current developments raise the question of which emerging market countries could experience funding pressure and sharp currency deprecations if yields continue to rise and financial market volatility stays elevated.

While we do not believe we are entering a new Taper Tantrum scenario just yet, we see value in providing early guidance on where sovereign yields could rise the most, and which emerging market currencies could be vulnerable. In that context, we offer a sensitivity framework and incorporate key variables we believe help determine sensitivity to the current reflation theme. Countries in emerging Asia and emerging Europe, Middle East and Africa (EMEA) have become less sensitive relative to the Taper Tantrum episode, while Latin America remains stable, leading us to believe the emerging markets in general are less sensitive to the current period of rising yields. However, there are some countries that could be vulnerable from both a yield and currency perspective, most notably South Africa and Mexico. In addition, sovereign debt has become more sensitive in Peru and Russia compared to the 2013 Taper Tantrum, while Hungarian yields could rise less significantly today relative to a decade ago. As for currency vulnerability, the Indian rupee has become a less sensitive currency in 2021 relative to 2013 as underlying economic fundamentals and politics in India have improved significantly. In the event of another interest rate shock and large selloff in the emerging markets, we would expect rupee depreciation to be much more contained.

Reflation Prospects Weighing on Emerging Markets

In recent weeks, the theme of reflation has dominated global financial markets. Persistent monetary and fiscal policy support has started to filter down to real economies around the world, supporting consumer spending, economic activity and price acceleration. Low interest rates and asset purchase programs are also likely to remain in place for the foreseeable future, both of which have boosted inflation prospects for the global economy. With the disinflationary impulse of the pandemic diminishing, financial market participants are beginning to assess the possibility of a sharp upturn in inflation, especially within the United States. To that point, CPI inflation in the U.S. is already above its pre-COVID trend, despite output in the United States still being below pre-pandemic levels. These dynamics suggest the backdrop for inflation may be starting to shift toward an environment of faster price growth.

Recent U.S. data provide further evidence that the inflation outlook for the U.S. economy could be firming going forward. January retail sales beat consensus forecasts by a wide margin, while February ISM data broadly beat expectations. In addition, we believe another $1.5 trillion fiscal support package is in the pipeline and expect a further round of direct checks to be delivered to households in the near future. Given the better-than-expected data and additional fiscal support, we now believe the U.S. economy can expand 6.2% this year, up from a previous forecast of 5.3%. Faster growth could also result in quicker inflation.

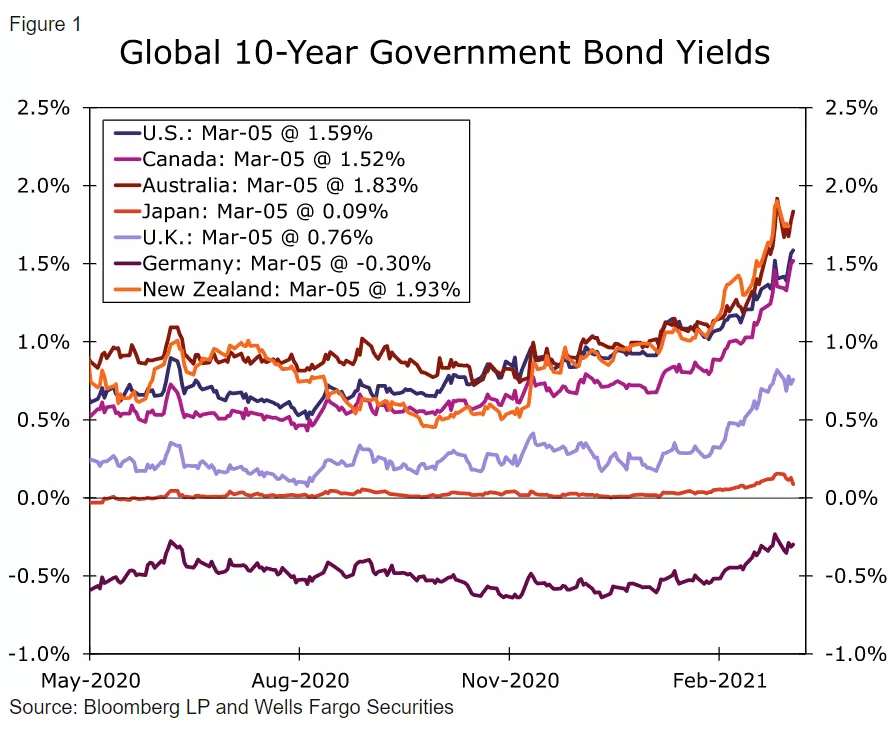

An improving U.S. economic growth and firming inflation outlook has resulted in a sharp selloff in U.S. Treasury bonds. In March, U.S. Treasury yields rose above 1.60%, up from 1.07% at the beginning of March, reflecting increased optimism around reflation in the United States. These dynamics are prevalent internationally as well, as government bond yields across the G10 have also risen materially over the course of this year (Figure 1). Typically, a rising interest rate environment places pressure on emerging market asset prices. When yields in the United States begin to rise, market participants may not feel as compelled to "search for yield" in riskier places like the emerging markets. Capital outflows from emerging markets tend to follow rising U.S. Treasury yields as investors shift capital back into the United States and other major economies. As a result, the U.S. dollar tends to outperform and emerging market currencies broadly come under pressure. These dynamics have played out over the past few weeks as the rise in U.S. rates resulted in renewed volatility across EM financial markets as equities and currencies sold off significantly and the U.S. dollar outperformed. In addition, sovereign yields across Latin America, emerging Europe Middle East and Africa (EMEA) and Asia broadly increased.

Author

Wells Fargo Research Team

Wells Fargo