Goldman Sachs maps the Trump-Xi tactical trade

- Goldman sees the upcoming Trump-Xi summit as more of a tactical stabilizer than a transformational geopolitical reset, with incremental trade and technology concessions viewed as the most realistic outcome.

- Investor positioning toward China remains relatively cautious, creating the potential for a positive sentiment squeeze if the meeting delivers even modestly constructive headlines.

- Offshore Chinese equities could outperform in the short run, given cheaper valuations, higher geopolitical beta, and stronger sensitivity to global liquidity flows.

- Structural themes continue to dominate investor attention, particularly around Chinese AI, technology self-sufficiency, shareholder returns, and Beijing’s long-term industrial policy roadmap.

- The market is increasingly treating China not as a pure macro trade, but as a collection of strategic themes where policy direction, innovation, and capital flows matter more than headline diplomacy alone.

The Trump-Xi tactical trade

With the reported meeting between President Trump and President Xi approaching, here are Goldman’s market thoughts on this subject in the following investor FAQs:

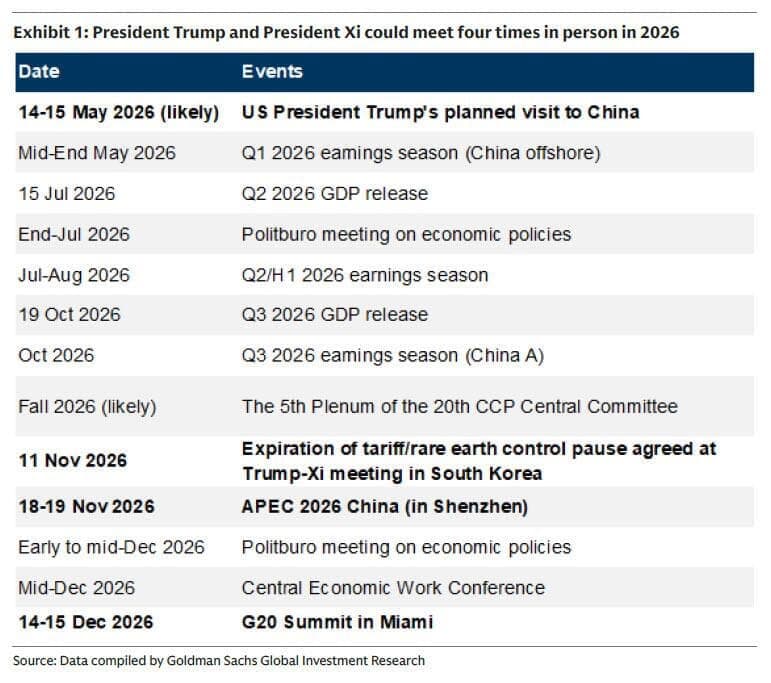

- What’s going to happen? President Trump could meet with President Xi in Beijing on May 14 and 15. If it proceeds, it will mark the first of potentially four in-person talks between the two leaders in 2026.

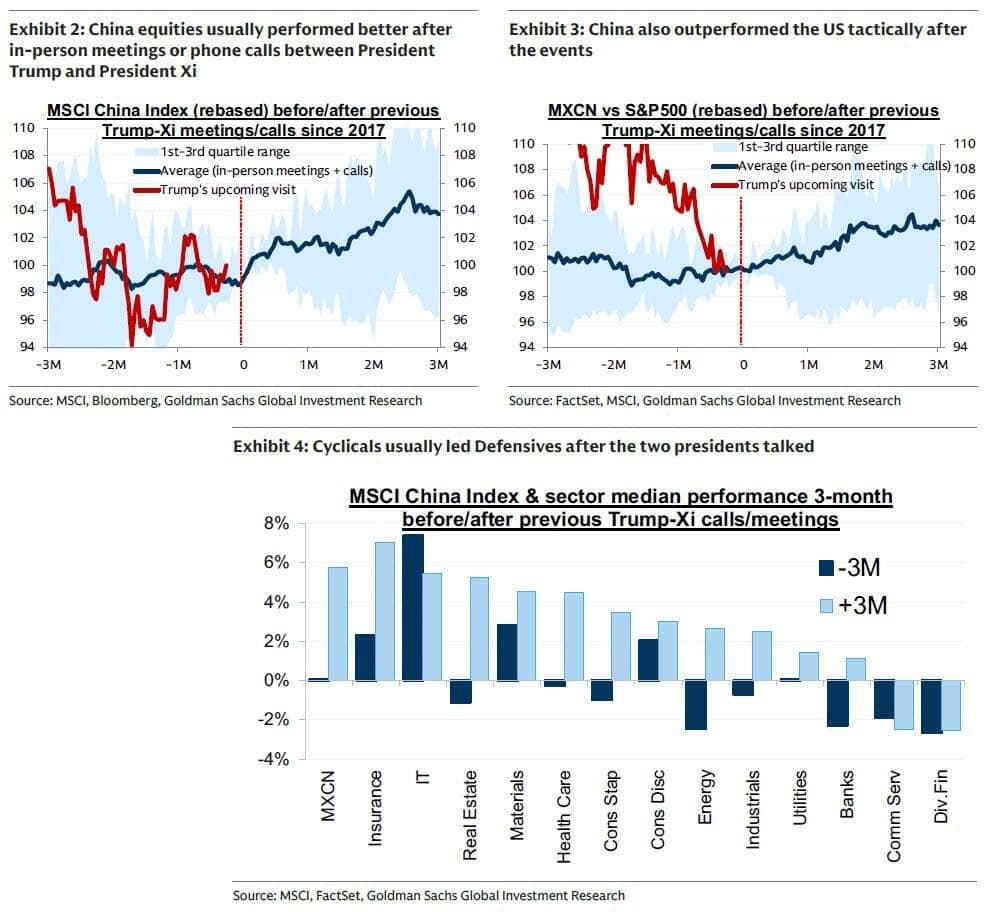

- How did Chinese equities trade around previous Trump/Xi interactions? The two presidents have conducted 6 face-to-face meetings and 12 phone calls since 2017. Chinese equities typically range-traded ahead of the dialogues but performed well thereafter, averaging 2%/4% returns in the next 1/3 months and outperforming SPX tactically post the events.

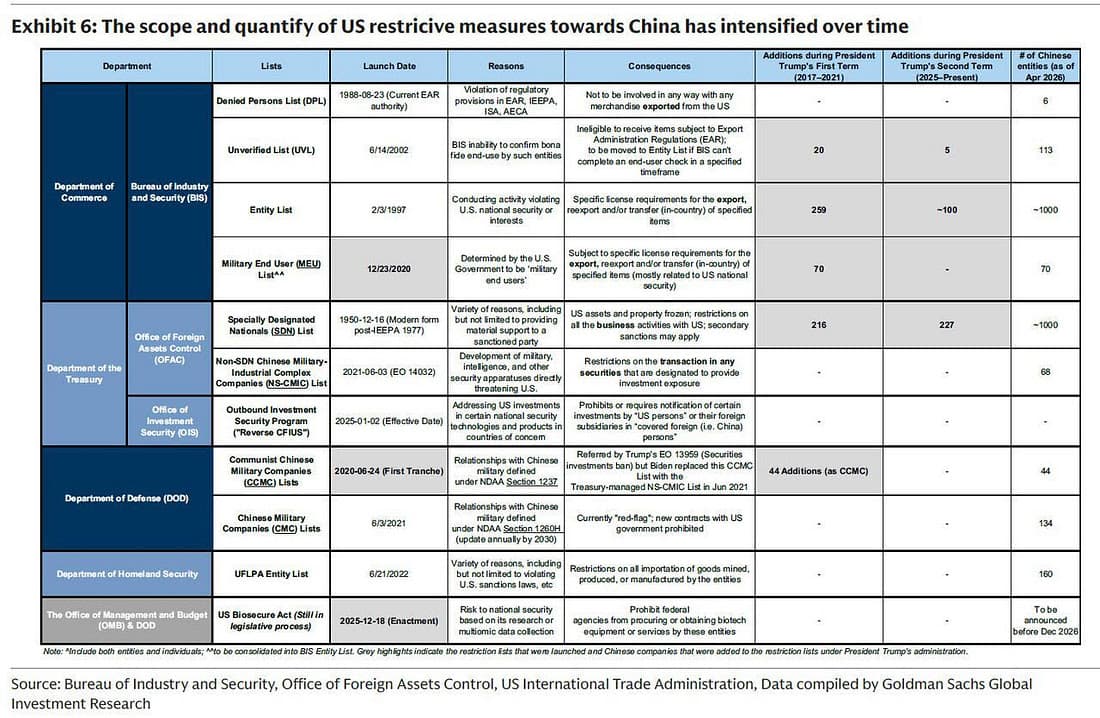

- What were the deliverables in the prior meetings? The agreements/deals were mostly trade- and commerce-oriented. From the end of Trump’s first term, tariffs on China have risen and the scope of US restrictions on Chinese companies has expanded.

- What could be discussed at the meeting? Goldman’s textual analysis suggests that the US could focus more on trade, while China may stress on technology/semiconductors and Taiwan issues.

- What’s GS expectation going into the meeting? GS economists expect China to buy more US farm goods, energy and manufactured products in exchange for fewer tech restrictions and slightly lower tariffs. A “grand bargain” is unlikely.

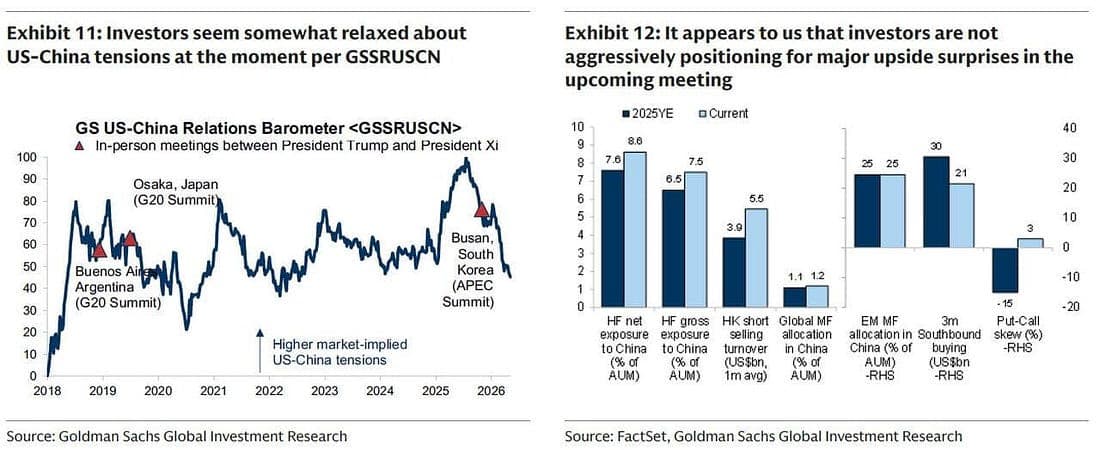

- What’s the market expectation going into the meeting? Low market expectations for positive surprises, given conservative investor positioning and flows. Goldman’s proprietary indicator suggests that US-China tensions are probably not a dominant market-driving factor at the moment.

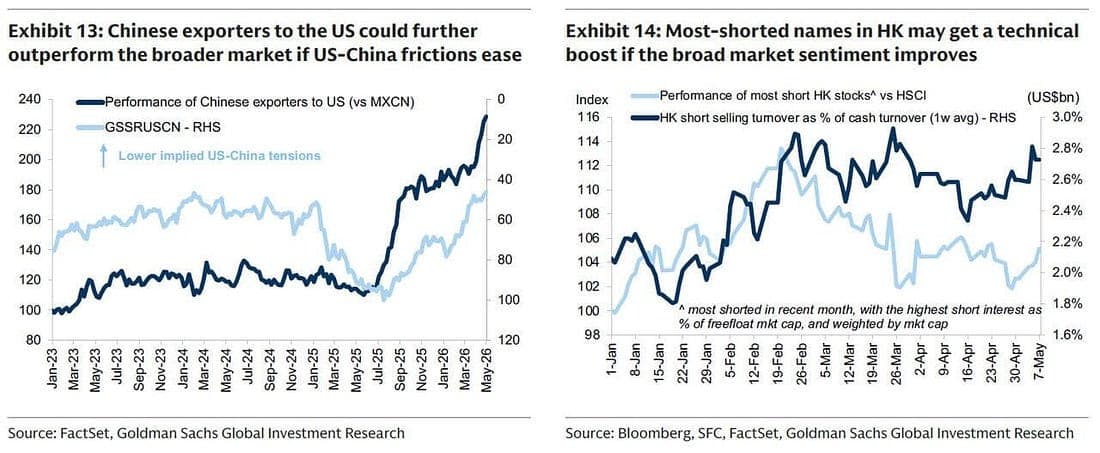

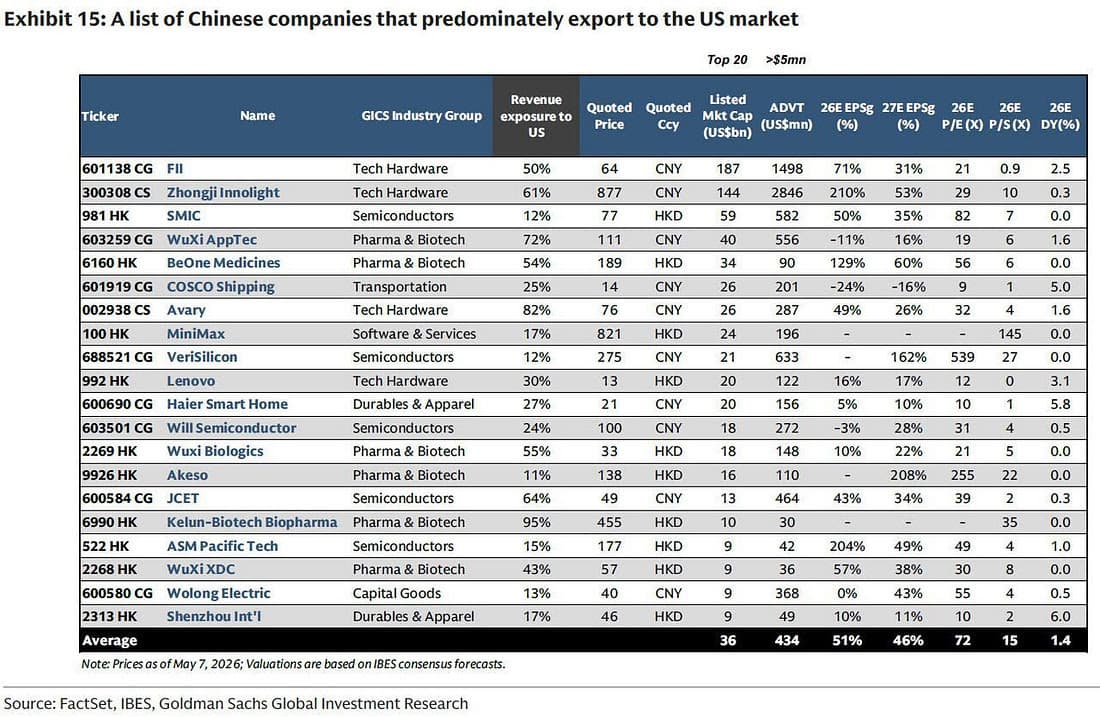

- How to position for the event in Chinese equities? Goldman sees a positive tactical upside case anchored by supportive empirical trading patterns, low investor expectations, and a compelling risk/reward profile for Chinese equity. They highlight Chinese exporters to the US, and a list of most-shorted HK-listed names for potential short-term alpha but would reiterate the bank’s strategically positive views on several structural themes, notably AI and the 15th Five-Year Plan.

Let’s look at each of these in more detail:

1. What’s going to happen? As previously signalled by President Donald Trump, he is set to travel to Beijing for meetings with President Xi Jinping on May 13-15, with Chinese state media Xinhua officially confirming the state visit early Monday local time. The announcement follows a steady increase in bilateral contacts and government-level communications in recent weeks, indicating that extensive groundwork for the summit has already been laid. The trip will mark only the second in-person meeting between the two leaders since President Trump returned to office in 2024, and could become the first in a series of four face-to-face engagements this year, with a potential reciprocal visit by President Xi to the United States, the APEC Summit in Shenzhen in November, and the G20 Summit in Miami in December all emerging as possible venues for further high-level talks.

2. How did Chinese equities trade around previous Trump/Xi interactions? Since 2017, Presidents Donald Trump and Xi Jinping have held six in-person meetings and 12 bilateral phone calls. Across those 18 interactions, offshore Chinese equities generally traded in a relatively tight range heading into the events, delivering average returns of roughly +1% over one month and flat performance over three months. Market performance historically improved after the engagements; however, Chinese equities gained an average of 2% over the following month and 4% over the subsequent three months, typically led by cyclicals and Growth sectors, while Internet shares and traditional Defensives tended to lag. China also outperformed US equities in the near term following the meetings, with an average excess return of around 4% over three months and a historical success rate of roughly 67%. The pattern suggests investors have generally viewed high-level US-China engagement as a stabilizing force for markets, helping reduce geopolitical overhangs and often acting as a tactical catalyst for renewed risk appetite in Chinese equities.

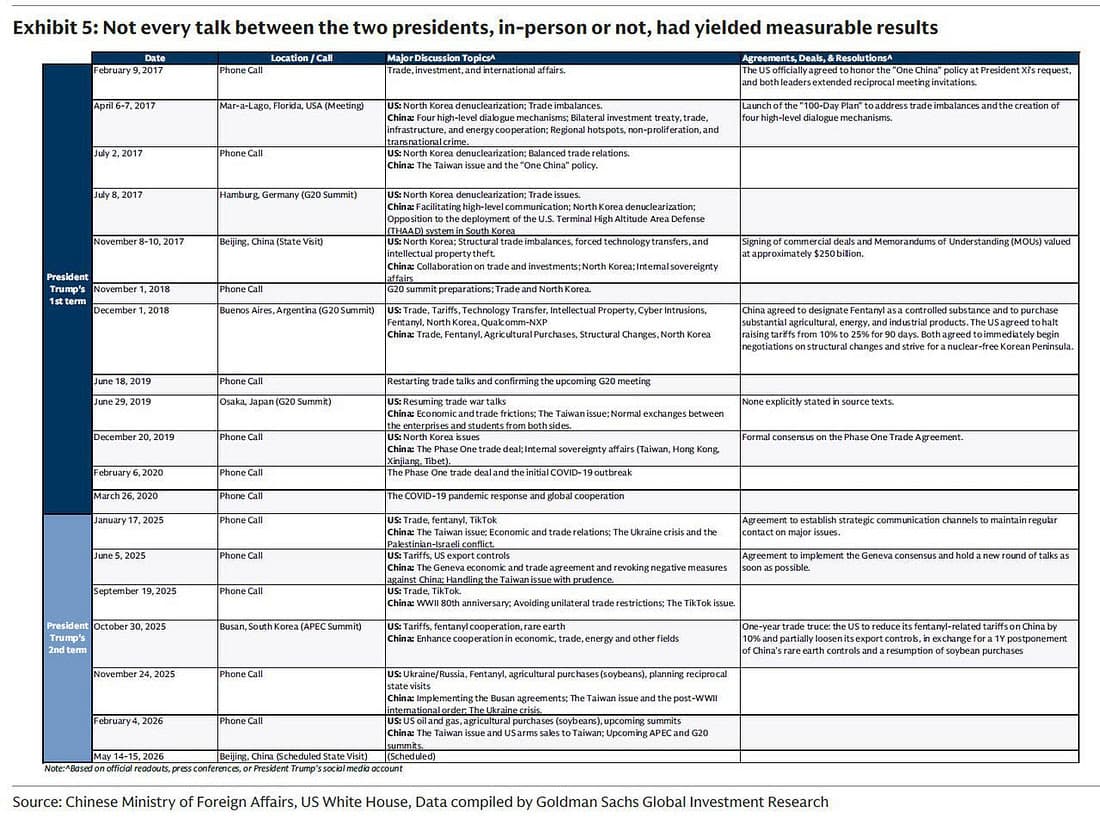

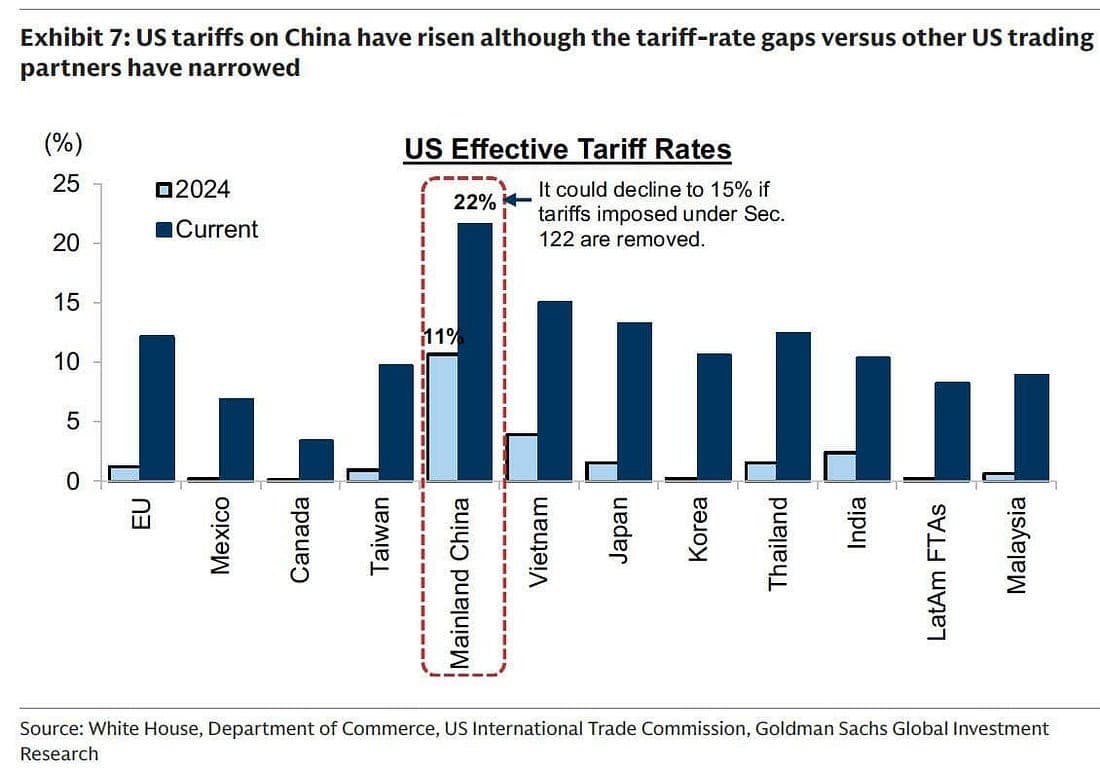

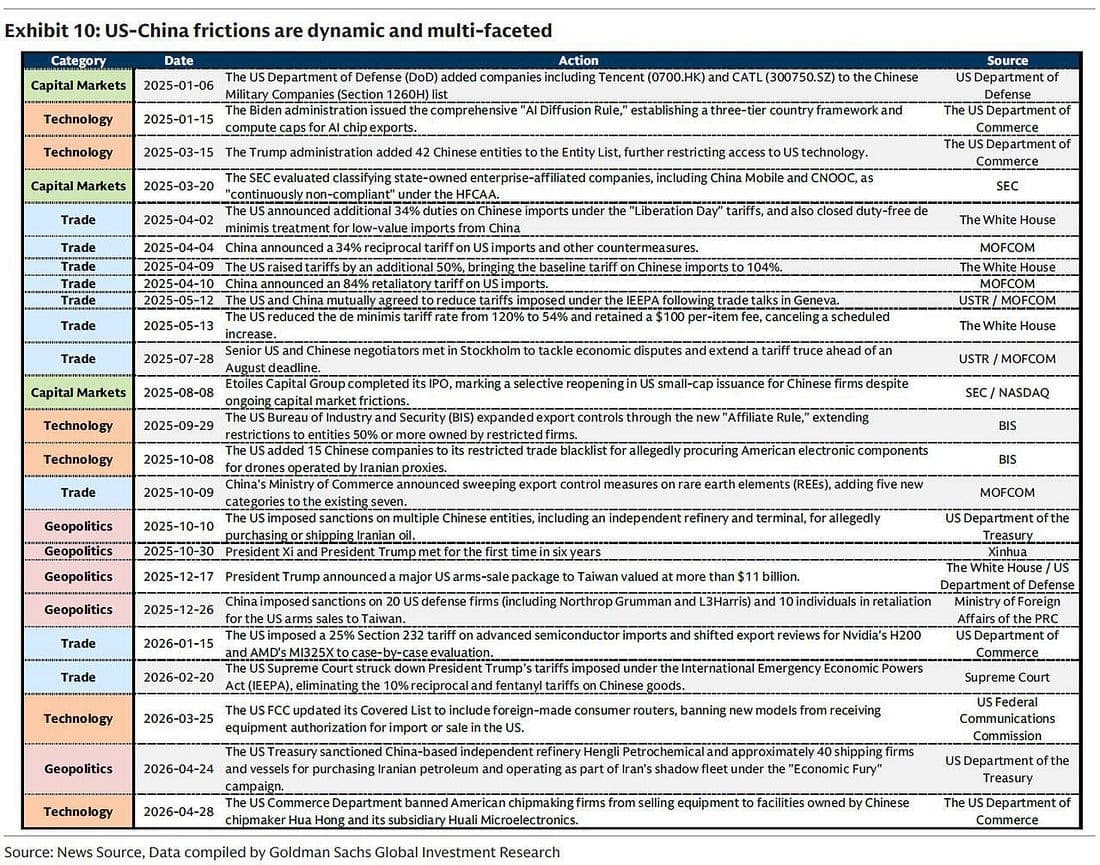

3. What were the deliverables in the prior meetings? It remains difficult to draw firm conclusions from past Trump-Xi interactions, given that each meeting unfolded against very different global macro conditions, geopolitical backdrops, and shifting strategic priorities on both sides. Still, several consistent themes have emerged since US China tensions intensified in 2018. First, not every engagement produced tangible or market-moving outcomes, particularly the various bilateral phone calls, which often served more as signalling exercises than breakthrough moments. Second, most agreements reached in recent years have centred around trade in goods and investment commitments, with China typically positioned as the primary purchaser. Third, effective US tariff rates on Chinese imports have steadily climbed across both Trump administrations, rising from roughly 11% at the end of 2024 to around 22% currently. Fourth, Washington’s technology restrictions have continued to broaden in both scope and intensity, alongside a growing list of Chinese firms facing export controls and investment restrictions. Finally, Taiwan has remained a near-constant feature of discussions, according to official Chinese readouts, underscoring that strategic security tensions continue to sit alongside efforts to stabilize the economic relationship.

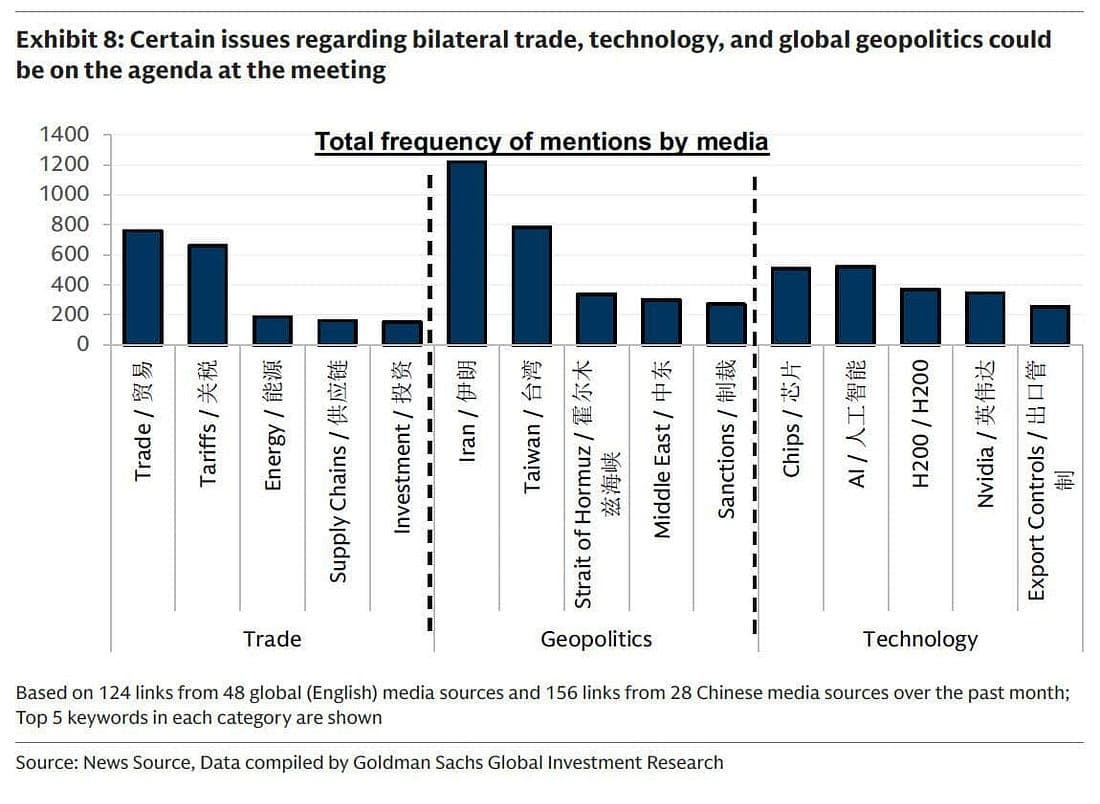

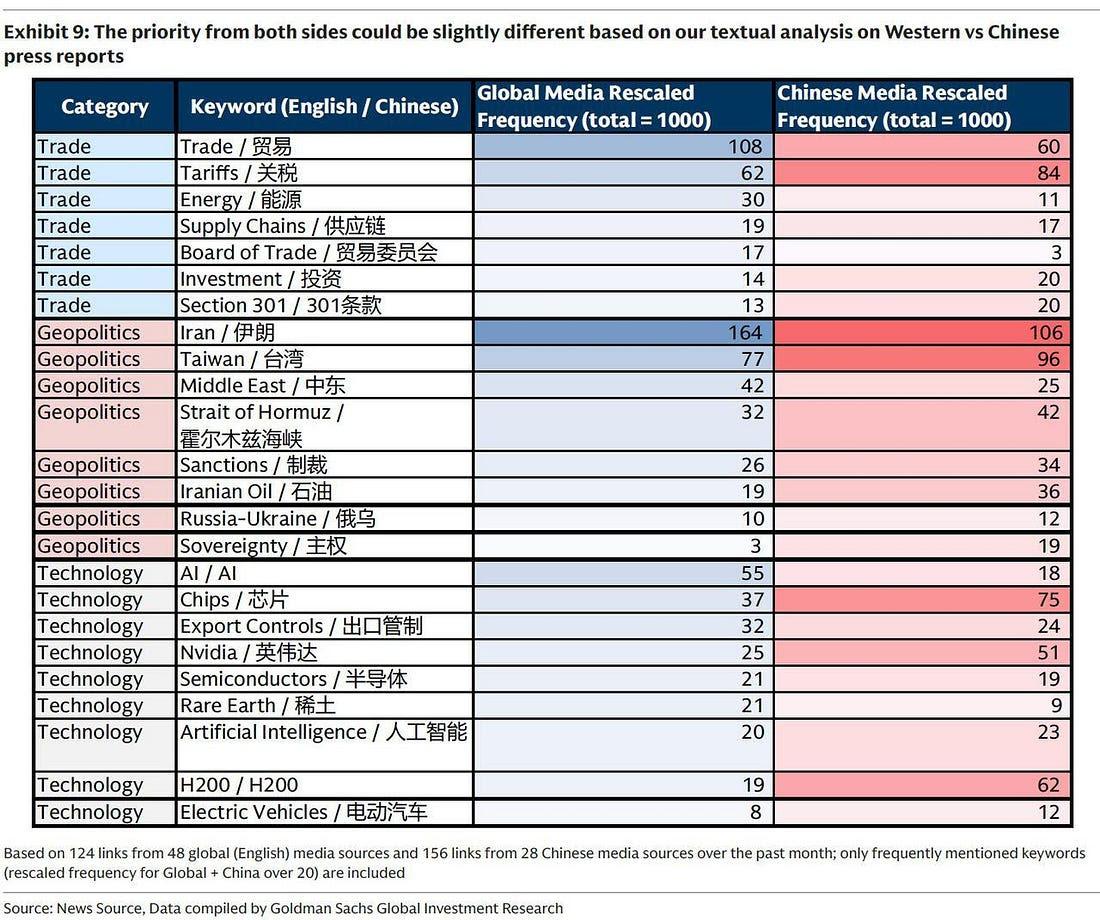

4. What could be discussed at the meeting? Goldman Sachs’ textual analysis, which tracks keyword frequency across more than 280 online news articles from major Western media outlets and Chinese state affiliated publications over the past month, suggests the upcoming Trump Xi meeting is likely to center around three primary pillars: trade, technology, and geopolitics. On the trade front, discussions are expected to focus heavily on tariffs, trade imbalances, energy flows, rare earth supply chains, purchase agreements, and foreign direct investment. Technology issues are also emerging as a central battleground, particularly around advanced semiconductors, artificial intelligence, technology transfers, and broader national security concerns tied to strategic industries. Geopolitical discussions are likely to include the evolving conflicts in the Middle East alongside the increasingly sensitive issue of Taiwan. Goldman’s analysis further suggests differing priorities between the two sides in their coverage of English- and Chinese-language media. From Washington’s perspective, the agenda appears more concentrated on trade and broader geopolitical positioning, while Beijing’s emphasis is skewing more heavily toward technology restrictions, industrial competitiveness, and Taiwan-related concerns.

5. What’s GS expectation going into the meeting? In Goldman’s base-case scenario, the bank’s economists expect China to increase purchases of US agricultural products, capital goods, energy supplies, and manufactured exports in exchange for some easing of technology restrictions and potentially modest reductions in tariffs on Chinese goods. However, consistent with Goldman’s recent discussions with industry experts and the broader consensus view among investors, the bank sees little chance of a sweeping “grand bargain” emerging from the upcoming Trump-Xi meeting. The expectation instead is for a more incremental and transactional framework, reflecting the deep structural tensions that continue to divide both sides on strategically critical issues ranging from technology dominance to national security and Taiwan. Goldman also notes that with several additional opportunities for the two leaders to meet later this year, both Washington and Beijing may prefer to keep negotiations flexible rather than force a comprehensive agreement at this stage.

6. What’s market expectation going into the meeting? Goldman frames its view on this question through the lens of:

- Market pricing: Goldman’s proprietary GSSRUSCN indicator, which attempts to quantify how deeply US China tensions are embedded into Chinese equity valuations, suggests investors remain relatively relaxed about the geopolitical risk backdrop for now, with the gauge currently sitting below mid cycle stress levels. In practical terms, this implies that bilateral tensions are not presently acting as a dominant driver of China equity performance, as markets appear more focused on domestic growth dynamics, policy support measures, earnings expectations, and broader global liquidity conditions than on the immediate risk of a renewed escalation in US China relations.

- Investor positioning: A range of objective positioning indicators also suggests investors are approaching the Trump Xi meeting with caution rather than aggressively chasing a bullish China re-rating scenario. Goldman notes that hedge fund gross exposure to Chinese equities has been rising faster than net exposure according to Prime Brokerage data, implying increased trading activity and tactical positioning rather than strong directional conviction. Mutual fund allocations to Chinese equities remain roughly 300 basis points underweight in aggregate, although positioning within emerging-market and broader Asia mandates has begun to improve modestly. Meanwhile, Hong Kong short-selling turnover has been gradually rising relative to overall cash market turnover, put-call skew has widened moderately year to date, and Southbound flows from mainland investors have remained broadly stable. Taken together, Goldman interprets these indicators as evidence that investors are not yet meaningfully positioned for a major upside surprise or decisive breakthrough from the upcoming summit.

- Factor performance: Chinese exporters with heavy exposure to the US market have consistently lagged the broader Chinese AI ecosystem and domestic technology self-sufficiency themes year to date, highlighting investors’ growing preference for structural and idiosyncratic growth stories over traditional macro or event-driven trades tied to US-China relations. The divergence suggests capital has increasingly gravitated toward sectors viewed as aligned with Beijing’s long-term strategic priorities, such as artificial intelligence, advanced manufacturing, semiconductors, and domestic innovation, while export-oriented names remain more vulnerable to tariffs, external demand uncertainty, and the broader geopolitical overhang surrounding bilateral trade relations.

7. How to position for the event in Chinese equities? While Goldman does not expect the upcoming Trump Xi meeting to fundamentally reset US China relations, the bank believes the event could still create a constructive tactical backdrop for Chinese equities. That view rests on three pillars: historically positive market performance following prior Trump Xi meetings, relatively conservative investor positioning heading into the summit, and what Goldman continues to see as an attractive risk reward setup for both China A shares and Hong Kong listed H shares within a regional allocation framework. In effect, the bank argues that current conditions offer investors a relatively inexpensive upside call option on China equities, with return asymmetry skewed positively on a tactical horizon.

Should global risk appetite improve after the meeting, Goldman expects offshore Chinese equities to outperform onshore A shares in the near term due to their higher sensitivity to geopolitical developments and global liquidity conditions, alongside cheaper valuations and relative underperformance versus mainland markets year to date. However, the bank cautions that any more durable rally in H shares would ultimately require a meaningful improvement in earnings growth and analyst upgrades, something Goldman believes is more likely to emerge later this year.

From a thematic perspective, Goldman sees potential near term upside in Chinese exporters exposed to the US economy as well as heavily shorted Hong Kong listed names, both of which could benefit from positioning squeezes and improving sentiment. For longer duration investors, the bank continues to emphasize structural themes tied to China’s AI ecosystem, the priorities embedded within the upcoming 15th Five Year Plan, improving shareholder return policies, and the expanding global footprint of Chinese corporations.

Author

Stephen Innes

SPI Asset Management

With more than 25 years of experience, Stephen has a deep-seated knowledge of G10 and Asian currency markets as well as precious metal and oil markets.