Gold Price Forecast: Faces risk of double top breakdown

- Gold defended $1,300 this week, but the relief could be short-lived.

- The payrolls figure missed estimates, but the June Fed rate hike is still on the table.

- The dollar index seems to have found acceptance above the long-term descending trendline.

- The US 10-yr treasury yield remains on the hunt for a big break above 3 percent.

Gold defended the psychological support of $1,300 (also the double top neckline) this week, but the fundamental factors and the inter-market analysis suggest the bears could soon take out the key support.

The non-farm payrolls released today showed the US economy added 164K jobs in April vs 192K expected. So, the headline number did miss estimates, still, the dollar remained bid, possibly because the headline number when viewed against the backdrop of sliding jobless rate (fell to 3.9 percent in March), indicates falling slack in the labor market.

Moreover, The 150,000 two-month NFP average remains comfortably above the roughly 120,000 increase needed to meet working-age population growth, according to Reuters report. Further, the unemployment rate (includes discouraged workers and those holding part-time positions) fell to 7.8 percent - the lowest level since July 2001.

So, the NFP report won't prevent a June rate hike. Meanwhile, the average weekly earnings (wage growth) rose 2.6 percent year-on-year, narrowly missing the estimate of 2.7 percent. The stagnant wage growth, though a cause of concern, is unlikely to kill June rate hike bets.

Markets still expect the Fed to hike rates in June and deliver another rate hike in the second half of this year. So, gold will likely remain on the back foot in the near-term.

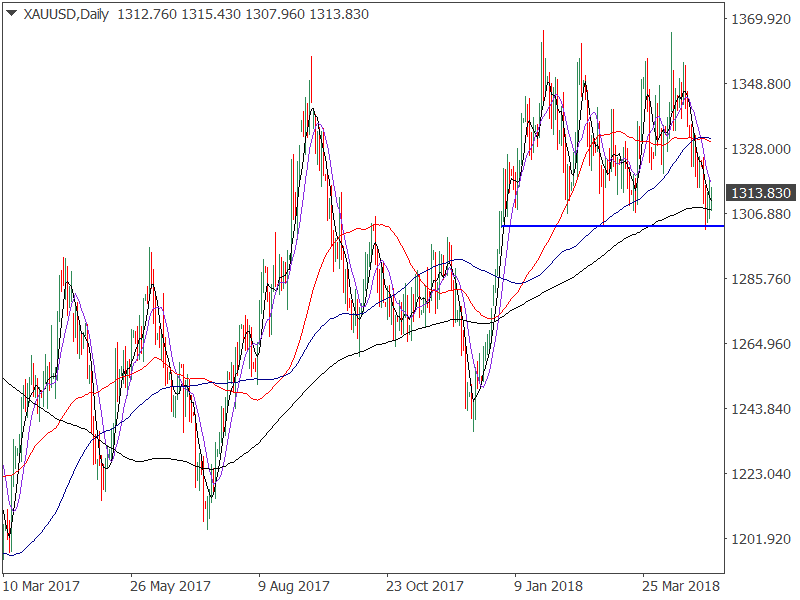

Gold Daily chart

The repeated bull failure favors double top breakdown. The 5-day moving average (MA) and the 10-day MA are trending southwards, indicating a bearish setup.

The related markets aren't helping the matters either. For instance, the dollar index has cut through the long-term descending trendline, signaling a bearish-to-bullish trend change, as seen in the chart below.

Dollar index daily chart

-636610589544104361.png)

The trendline sloping downwards from January 2017 high and March 2017 high has been breached. The bullish breakout, coupled with the talk of the June Fed rate hike will likely yield a rally to 94.22 (Dec. 12 high) over the next few weeks.

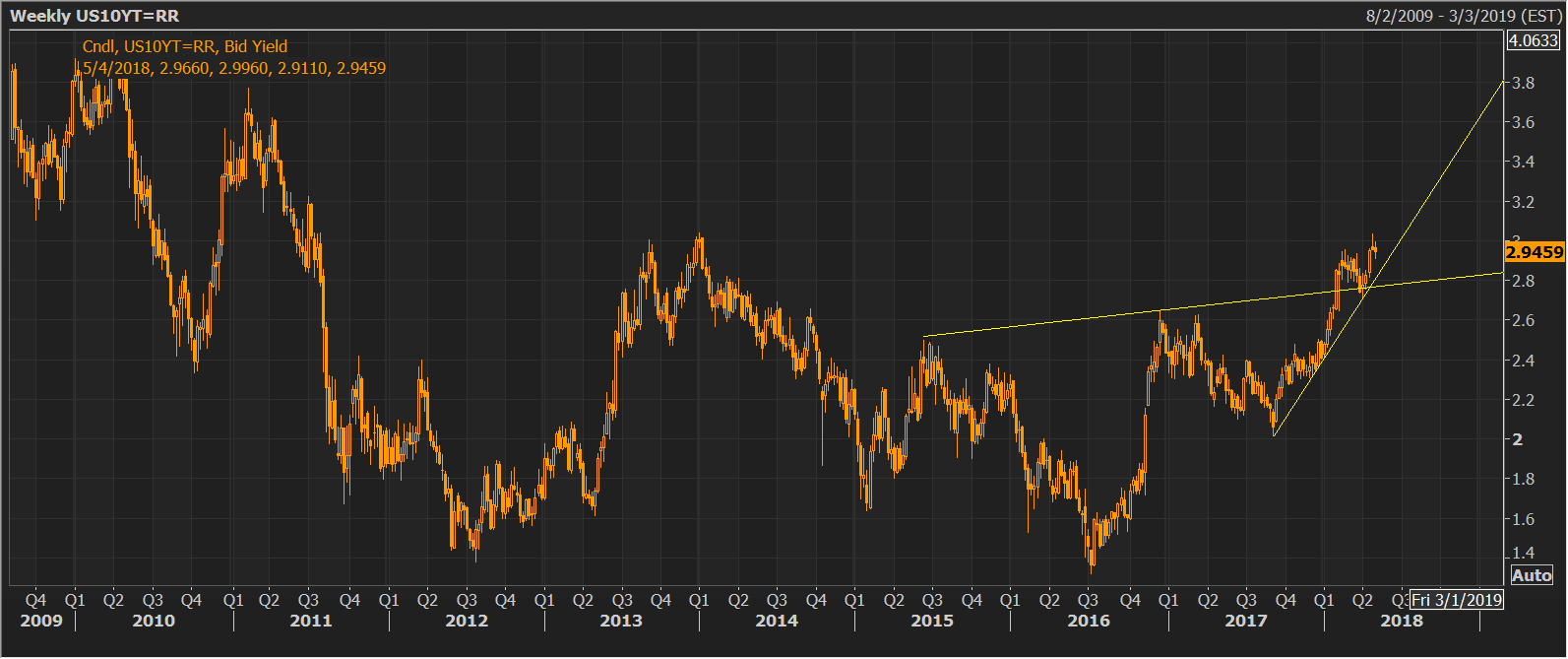

US 10-year Treasury yield weekly chart

Meanwhile, the 10-year treasury yield seems to have found acceptance above the inverse head-and-shoulders neckline and it is only a matter of time before it breaks above 3 percent in a convincing manner.

The rising yields and rising US dollar is gold-negative and vice versa. Thus, the probability that metal will drop below the $1,300 confirming a double top breakdown is high. A close below $1,300 would open the doors to $1,240 (double top breakdown target).

However, the 50-week MA, 100-week MA and the 200-week MA are aligned in favor of the bulls. So, the downside post-double top breakdown could be capped around $1,270.

On the higher side, a move above the 10-week MA would signal bearish invalidation, while a bull revival is seen only above $1,380.

Author

Omkar Godbole

FXStreet Contributor

Omkar Godbole, editor and analyst, joined FXStreet after four years as a research analyst at several Indian brokerage companies.