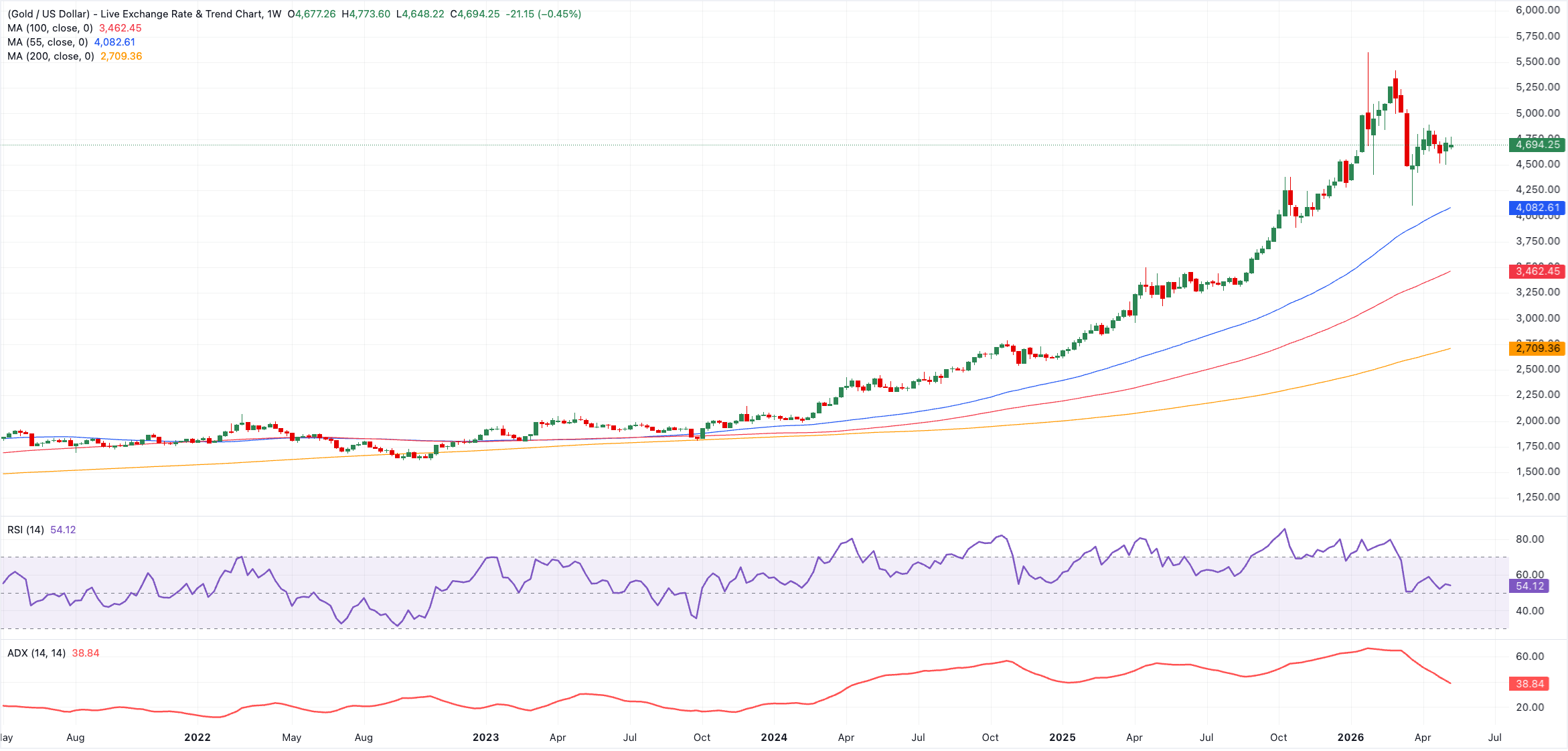

Gold at a crossroads: What would it take to reach $5,000 again?

Gold has gone strangely quiet, leaving traders wondering whether this is a temporary pause or something bigger is on the horizon.

After the spectacular rally seen earlier this year, bullion has spent the last several weeks drifting in the $4,400-$4,900 band per troy ounce, unable to fully regain the momentum that drove the explosive move higher in the first quarter.

That pause is intriguing.

Because if you look closely, the broader macro backdrop for Gold has not really disappeared. In many ways, it still looks supportive. The Federal Reserve (Fed) remains trapped between slowing growth and sticky inflation; geopolitical tensions continue simmering in the background; central banks are still buying Gold aggressively; and concerns over the long-term credibility of global debt dynamics are quietly becoming more mainstream.

And yet, Gold has stalled.

The market feels as though it is waiting for something bigger, another catalyst strong enough to justify a fresh run toward the psychological $5,000 level and potentially beyond.

In reality, Gold probably does not need just one catalyst. It likely needs a combination of macro stress, policy uncertainty and a renewed loss of confidence in the system itself.

The Fed still holds the key

At the centre of the Gold story remains the Fed.

Yes, Gold has managed to perform surprisingly well despite elevated US interest rates, but historically, the biggest and most aggressive rallies in bullion tend to happen when markets begin anticipating a meaningful shift in monetary policy.

Not simply rate cuts, but rate cuts arriving at a moment when inflation still refuses to fully disappear.

That distinction matters enormously.

The ideal backdrop for Gold would probably involve weaker US growth, softer labour market conditions and a Fed gradually moving toward easing policy, while inflation remains sticky enough to keep real yields under pressure.

That is the kind of environment where investors begin questioning the purchasing power of fiat currencies again and the so-called debasement trade kicks in.

And if markets start believing the Fed is falling behind the curve, or cutting rates into an economy still dealing with inflation problems, Gold could very quickly regain momentum.

Because ultimately, bullion tends to thrive when confidence in monetary stability starts deteriorating.

Geopolitics could still ignite another surge

Another major driver would be a renewed geopolitical shock.

Gold’s biggest rallies over recent years have almost always coincided with periods when markets suddenly realised that geopolitical risk was no longer just background noise.

The Middle East remains the obvious focal point.

Any escalation involving Iran, the Strait of Hormuz or regional Oil infrastructure would almost certainly trigger another rush into safe-haven assets. The same applies to any deterioration in US-China relations, Taiwan tensions or a broader geopolitical fragmentation story.

Importantly, Gold does not necessarily require a full-blown global crisis. It simply needs markets to begin repricing instability again.

And if geopolitical tensions simultaneously push Oil prices higher, the effect becomes even more powerful. Rising energy prices tend to feed directly into inflation expectations, creating exactly the kind of uncomfortable macro backdrop that historically benefits bullion.

The bigger story may actually be debt

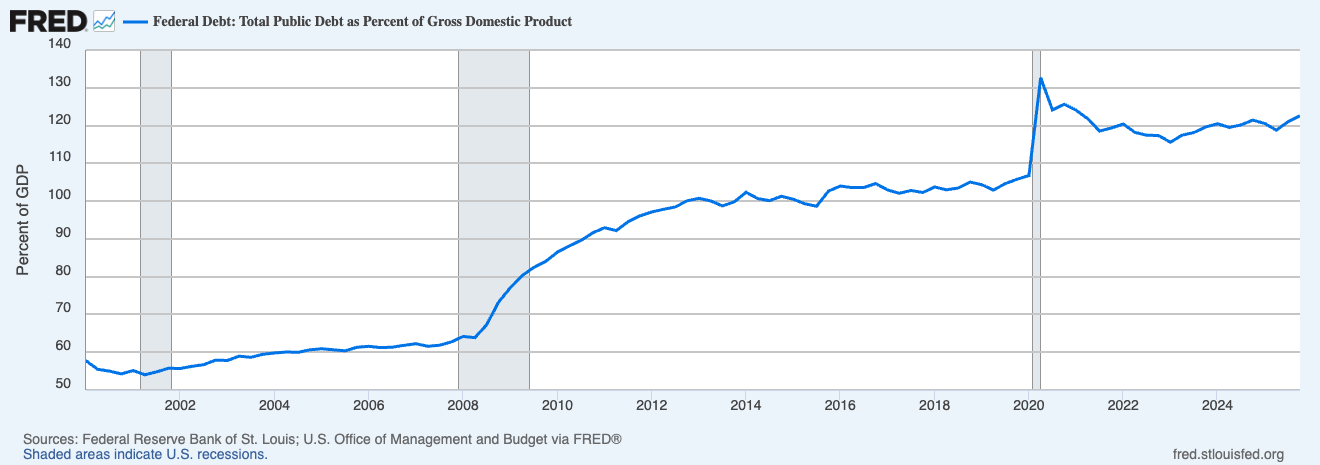

Perhaps the most important long-term catalyst, however, is not war, inflation or even the Fed. It may be debt.

For years, markets largely ignored the steady deterioration in the US fiscal backdrop, but that is becoming harder to do.

Deficits remain enormous, Treasury issuance continues climbing, and interest payments on government debt are consuming a growing share of public spending. At the same time, investors are increasingly starting to ask uncomfortable questions about whether the current trajectory is sustainable over the long run.

And this is where the Gold story becomes much deeper than a traditional safe-haven trade.

Because increasingly, investors are no longer buying bullion simply as protection against volatility. They are buying it as protection against a potential loss of confidence in the broader monetary system itself.

That shift matters.

The old Gold narrative was largely:

- Buy Gold when markets panic.

The emerging narrative increasingly feels more like:

- Buy Gold when trust in fiscal and monetary credibility begins to weaken.

That is a far more structural theme.

Central banks are quietly changing the market

One of the most underestimated aspects of the current rally has been the scale of central bank demand.

Countries such as China and India have continued accumulating Gold reserves at an aggressive pace, partly as a diversification strategy away from the US Dollar system.

The weaponisation of sanctions in recent years has accelerated that process.

Many countries now appear increasingly uncomfortable with excessive reliance on US Dollar-denominated reserves, particularly in a world becoming more geopolitically fragmented.

That steady sovereign demand has changed the underlying structure of the Gold market.

Instead of relying purely on speculative inflows, the precious metal now has a much stronger layer of structural buying underneath it. And that makes deep corrections harder to sustain.

Momentum could eventually do the rest

Then comes the final ingredient: momentum.

If Gold eventually breaks decisively above $5,000, the psychology of the market could shift rapidly.

A large number of investors still feel they missed the first major rally. Once psychologically important levels begin breaking, commodity markets often become highly reflexive. Systematic funds, macro traders, exchange-traded fund (ETF) inflows and retail investors all begin chasing the same move simultaneously.

At that point, Gold can stop behaving like a slow-moving defensive asset and start trading more like a momentum-driven macro trade.

That is when overshoots become possible.

To sum up

For now, the yellow metal still feels torn between conviction and hesitation.

The structural bullish story remains alive, but the market is still searching for the next catalyst powerful enough to reignite the move.

And perhaps that is the real story here.

Gold may no longer be trading purely on fear. Increasingly, it may be trading on confidence, or the lack of it, in the global financial system itself.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.