GBP/USD Weekly Forecast: The worst seems far from over, focus shifts to US inflation, UK GDP

- GBP/USD witnessed a fresh downside leg during Fed/BOE week.

- Cableslumped to 22-month lows as the BOE fanned UK recession fears.

- A bear flag on the daily chart points to more pain, with eyes on US inflation, UK GDP.

The Fed-BOE contrast remained in play, despite the less aggressive Fed stance, as the dire UK economic outlook widened the economic divergence alongside the monetary. GBP/USD was fairly resilient throughout the week before crashing to fresh 22-month lows below the 1.2300 mark. The pair has recorded the third straight weekly loss, as attention turns towards the US inflation and the UK quarterly GDP.

GBP/USD: Nothing stopped bears

After the previous week’s selling spiral to 1.2411, the lowest level since July 2020, GBP/USD entered a phase of downside consolidation in the first half of the week. The early May bank holiday in the UK and risk-averse market conditions prompted the US dollar bulls to take control. Contraction in the Chinese business activity due to the ongoing covid lockdowns in the country dented the market mood.

GBP bulls, however, managed to find some comfort from pre-Fed meeting dollar repositioning, while the greenback pulled back on disappointing US ISM and S&P Global Manufacturing PMIs. Cable buyers bought into the dip below 1.2500, as risk sentiment improved and weighed negatively on the safe-haven buck. Meanwhile, the pound cheered the Reuters report that markets now price in a 30% probability of a larger than expected, 50 bps hike from the BOE on Thursday, especially after Tuesday’s Reserve Bank of Australia's (RBA) 25 bps hawkish hike.

The GBP/USD rebound only strengthened after the dollar correction gathered steam alongside a fall in the US Treasury yields following the Fed’s less aggressive tightening stance on Wednesday. The world’s most powerful central bank turned out to be less hawkish than expected, pouring cold water on expectations of a 75 bps rate lift-off in June. The Fed decided to hike the key Fed Funds rate by the expected 0.50% while commencing the balance sheet reduction process at a rate of $47.5 billion per month from June 1st with an intention to raise it to $95 billion in three months.

The currency pair failed to resist bearish pressure once again above 1.2600 and witnessed a massive sell-off on Thursday, as the BOE projected a recession for the UK economy in the final quarter of 2022 after unanimously hiking the key rates by 25 bps to 1%. The ‘Old Lady’ raised inflation forecasts, citing that inflation is peaking at around 10% in the Q3 vs. the previous 7.5% in April. Global growth fears intensified, which triggered a fresh flight to safety mode and revived the dollar’s haven demand. Cable hit 22-month lows at 1.2325, shedding 300 pips on ‘Super Thursday’.

There was no reprieve for cable on Friday, as it renewed 22-month lows below 1.2300 during the European trading hours. The dollar preserved its strength ahead of the weekend as the US jobs report confirmed tight labor market conditions and didn't allow the pair to stage a meaningful rebound. The US Bureau of Labor Statistics reported that Nonfarm Payrolls rose by 428,000 in April, surpassing the market expectation of 391,000. Additionally, the Labor Force Participation Rate edged lower to 62.2% from 62.4% in March and the annual wage inflation stayed little changed at 5.5%.

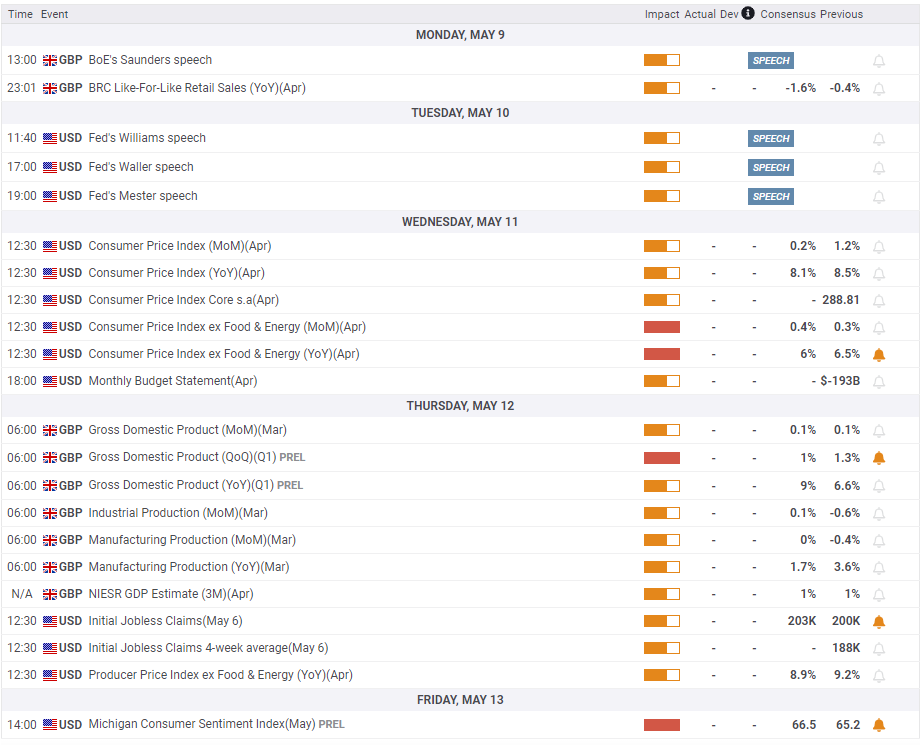

Week ahead: US Inflation and UK GDP take center stage

Following a dramatic week, dominated by central bank events, markets now brace for the US inflation and UK GDP releases, which will stand out in an otherwise relatively light week. Meanwhile, cable will continue dancing to the dynamics of the dollar and the Fed-BOE divergence.

The week starts with the speech by the BOE policy-maker Micheal Saunders on Monday. Note that Saunders joined other hawks Catherine Mann and Jonathan Haskel to vote for a 50 bps hike at the BOE policy meeting last Thursday.

Tuesday is data-empty, as it offers no first-tier economic releases from both sides of the Atlantic –although Fedspeak could gather attention.

The all-important US Consumer Price Index (CPI) for April drops in on Wednesday, which could offer fresh hints on the Fed’s policy guidance.

On Thursday, the UK Q1 Preliminary GDP data will be published alongside the monthly figure and the Manufacturing Production data. This could have a significant impact on the pound, given the BOE’s warning of stagflation. Later in the day, the US will publish the Producer Price Index (PPI) for April.

Friday will be relatively quiet, with the only US Preliminary Michigan Consumer Sentiment due on the cards. Fed policymaker Loretta Mester will also make an appearance.

GBP/USD: Technical outlook

The bear flag formation seen on the daily chart suggests that the pair is likely to target new lows in the near term. The flag pole covers approximately 500 pips, suggesting that the next bearish target aligns at around 1.2100, taking 1.2600 as the starting point of the current downtrend.

It's worth noting, however, that the Relative Strength Index (RSI) indicator on the same chart stays below 30, pointing to oversold conditions. In case the pair stages a correction, 1.2400 (psychological level, bottom of the bear flag pole) aligns as the first resistance before 1.2500 (psychological level).

On the downside, 1.2200 (psychological level) and 1.2170 (static level from May 2020) could act as interim supports ahead of 1.2100.

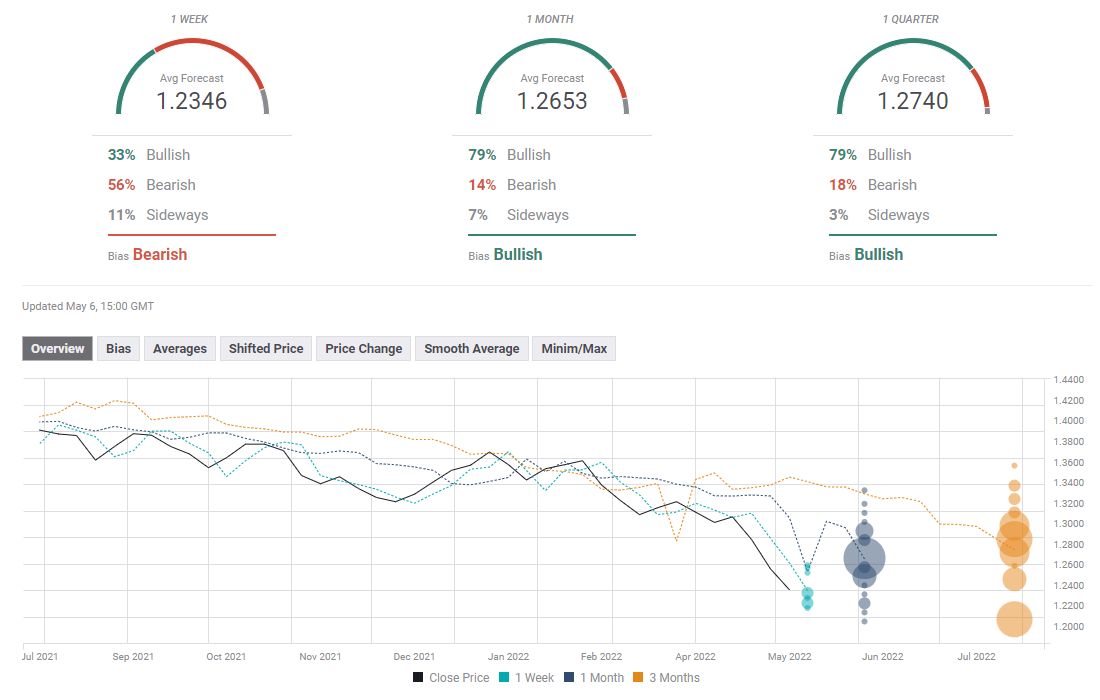

GBP/USD: Sentiment poll

The FXStreet Forecast Poll shows that the majority of polled experts see the pair pushing lower next week. The one-month and the one-quarter outlooks, however, remain overwhelmingly bullish.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Dhwani Mehta

FXStreet

Residing in Mumbai (India), Dhwani is a Senior Analyst and Manager of the Asian session at FXStreet. She has over 10 years of experience in analyzing and covering the global financial markets, with specialization in Forex and commodities markets.