GBP/USD Weekly Forecast: Pound Sterling bulls regain control ahead of next week's key events

- GBP/USD bulls retained control as the US Dollar dominance continued to fade.

- GBP/USD’s fate hinges on the US Federal Reserve decision and United States jobs’ data.

- Bullish RSI keeps GBP/USD buyers hopeful but 1.2580 needs to be cleared first.

Pound Sterling buyers managed to retain control as the GBP/USD pair rallied on Friday following a choppy trading within a 150 pip range earlier in the week. The United States Dollar (USD) resumed its sell-off, as investors weighed US earnings, the health of the economy and the US Federal Reserve (Fed) interest rates’ outlook. Attention now turns toward the Fed policy announcements in the week filled with top-tier economic data from the United States, including the all-important Nonfarm Payrolls (NFP).

GBP/USD: What happened last week?

The US Dollar sellers returned in a data-busy week, with risk sentiment mainly driven by corporate earnings reports from the United States. That said, choppy trading in the US Dollar extended for the second week in a row, leaving GBP/USD in a defined range. US banking sector concerns re-emerged in the first half of the week and sapped investors’ confidence, motivating US Dollar bulls to jump back into the game.

The troubled US bank, First Republic Bank’s shares slumped about 50% after the bank said it lost customer deposits of $102 billion in the first quarter. Meanwhile, tensions escalated over the approaching US debt ceiling deadline after the House Rules Committee unexpectedly went into recess, delaying a Republican bill authorizing a $1.5 trillion increase to the US debt ceiling. Against this backdrop, recession fears crept back and lifted the safe-haven appeal of the US Dollar.

However, flight-to-safety driven flows into the US government bonds smashed the US Treasury bond yields across the curve, curbing the rebound in the US Dollar. Markets pared their bets on a 25 basis points (bps) Federal Reserve rate hike next week to around 70% amid renewed fears over a US economic recession. Markets ignored upbeat Durable Goods Order data from the United States. US durable goods orders rose 3.2% in March, beating estimates of a 0.8% increase, and improving on February's 1.2% drop. GBP/USD tested levels sub-1.2400 amid risk aversion and renewed US Dollar strength.

The tide soon turned in favor of US Dollar bears, as optimism returned alongside upbeat tech earnings from Meta Platforms and Amazon, allowing GBP/USD to retake the 1.2500 threshold. Nevertheless, Cable’s upside petered out toward the latter part of the week, as the US Dollar regained its footing after the details of the US GDP report for the first quarter. Despite the headline US Q1 GDP number missing estimates of 2.0% QoQ by a wide margin at 1.1%, resilient personal consumption, inventories accumulation and a higher inflation component grabbed investors’ attention and ramped up odds of a 25 basis points (bps) Fed rate hike next week to 86%.

The US Dollar held onto its recovery mode, making it an uphill task for GBP/USD bulls on the final trading day of the week. Investors trading with caution heading into the monthly close and ahead of the Fed’s preferred gauge, US Core PCE Price Index.

Ahead of the weekend, the US Bureau of Economic Analysis reported that inflation in the US, as measured by the Personal Consumption Expenditures (PCE) Price Index, fell to 4.2% on a yearly basis in March from 5.1% in February. The annual Core PCE Price Index, the Federal Reserve's preferred gauge of inflation, edged lower to 4.6% from 4.7% in the same period. Although these data failed to trigger a noticeable market reaction, the rebound seen in Wall Street's main indexes following a negative opening limited the USD's gains and allowed GBP/USD to advance to its highest level since early June 2022 beyond 1.2550.

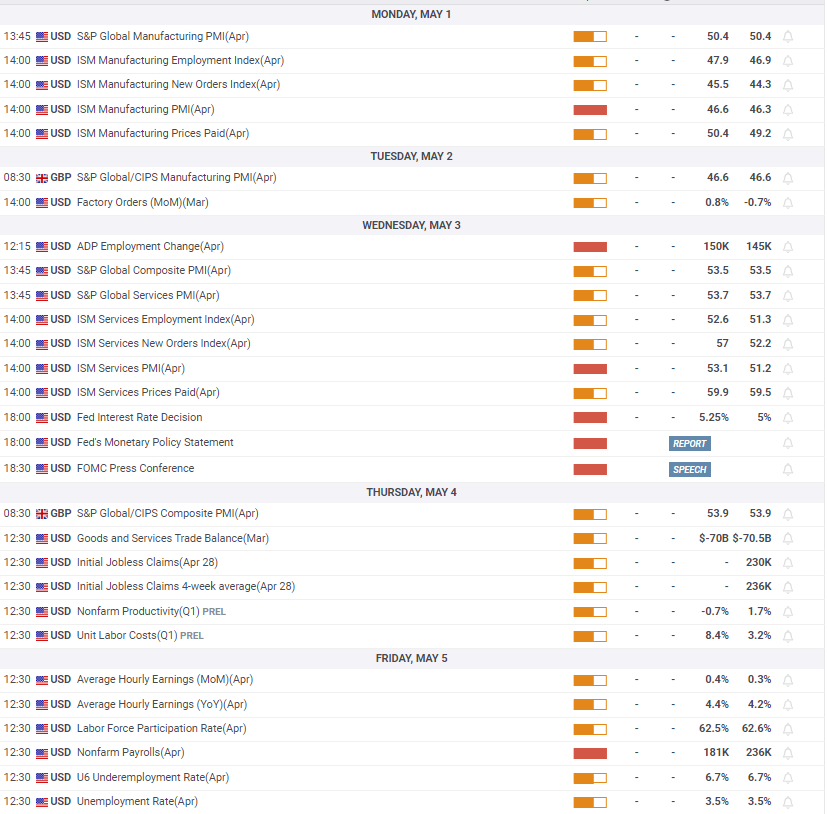

In focus: United States Federal Reserve verdict and Nonfarm Payrolls

With the United States banking sector fears back in play, the Federal Reserve interest rate decision in the week ahead will be eagerly anticipated for the world’s most powerful central bank’s future policy course.

Ahead of that, a fresh batch of top-tier economic data from the United States will be reported, starting with the ISM Manufacturing PMI and its sub-component Manufacturing Prices Paid Index due for release on Monday. The start of the week will witness thin liquidity conditions, as most of the major European markets are closed while the United Kingdom observes Labor Day.

Tuesday will feature the final print of the UK Manufacturing PMI, followed by the JOLTS Job Openings and Factory Orders data from the US docket.

Moving on, the US ADP Employment Change data and ISM Services PMI will grab the market’s attention on Wednesday ahead of the highly-anticipated Federal Reserve policy announcements. Fed Chair Jerome Powell’s press conference will hold the key, as investors will scrutinize his words on the US banking sector troubles, recession risks and future policy. The Fed event is likely to trigger extreme volatility around the US Dollar and eventually around the GBP/USD pair.

Thursday’s Chinese Caixin Manufacturing PMI and the UK final Services PMI could be overlooked by Pound Sterling traders, as they would be assessing the implications of the Fed outcome on the pair. Later on Thursday, the European Central Bank (ECB) interest rates decision could stir markets again, having a EUR/GBP cross-driven rub-off effect on Cable.

From the United States economic calendar, the Fed’s closely watched quarterly Prelim Unit Labor Costs data will be published on Thursday, alongside the weekly Jobless Claims data.

Friday will see an eventful end to a busy week, as the United States Nonfarm Payrolls report will stand out amidst the releases of China’s Trade Balance report and the Caixin Services PMI. Following the Federal Reserve decision, the US labor market report will help reprice the Fed interest rates outlook for the June and July policy announcements.

The focus will also remain on the US banking sector strain and the return of Federal Reserve speakers after the policy decision. Investors will also resort to repositioning ahead of next week’s crucial United States Consumer Price Index (CPI) data and the Bank of England monetary policy decision.

GBP/USD: Technical outlook

Following the previous week’s breakdown from a three-week-long rising wedge, GBP/USD continued to struggle alongside the wedge support-turned-resistance that aligned between the 1.2500-1.2530 range all through the week.

The downside, however, remained cushioned by the upward-sloping 21-Day Moving Average (DMA) near 1.2440. Looking ahead, the bullish potential in the GBP/USD pair appears intact so long as it holds above the 21 DMA support.

The 14-day Relative Strength Index (RSI) is holding comfortably above the 50 level, adding credence to the positive bias. Pound Sterling bulls, however, need acceptance above the wedge resistance at 1.2580. Further up, the May 2022 high at 1.2616 could challenge bullish commitments before the pair could target 1.2700 psychological level next.

On the flip side, if the 21 DMA support gives way, then GBP/USD sellers could target the critical support near 1.2350. Failure to defend the latter will open floors toward the April 3 low of 1.2275. The bullish 50 DMA at 1.2248 could come to buyers’ rescue. Immediate support then awaits at the 100 DMA of 1.2211.

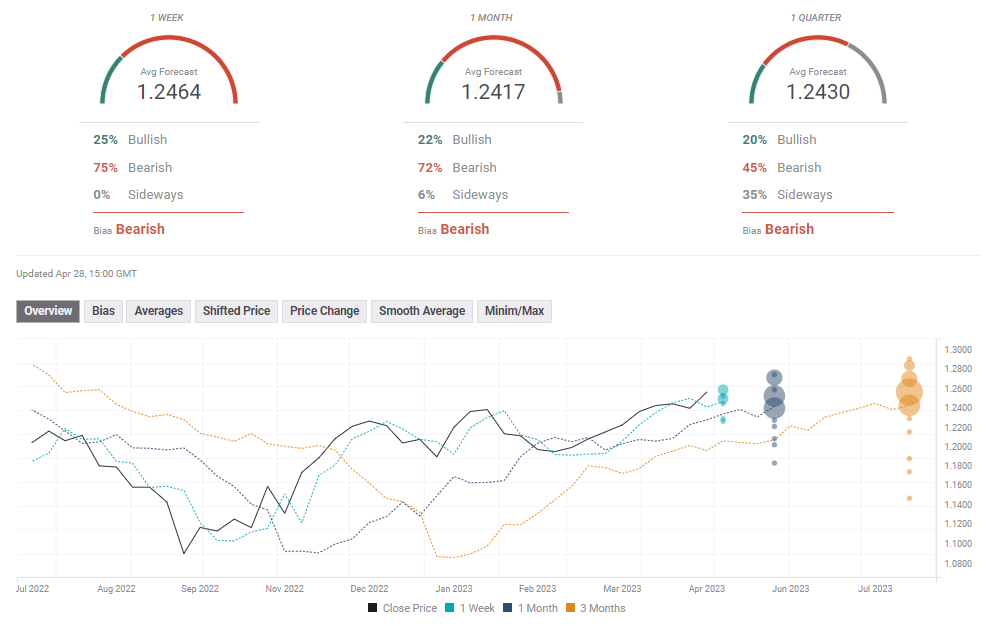

GBP/USD: Forecast poll

Despite Friday's action, FXStreet Forecast Poll remains overwhelmingly bearish in the short term with the one-week average target aligning at 1.2464. The one-month view also points to a bearish bias.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Dhwani Mehta

FXStreet

Residing in Mumbai (India), Dhwani is a Senior Analyst and Manager of the Asian session at FXStreet. She has over 10 years of experience in analyzing and covering the global financial markets, with specialization in Forex and commodities markets.