GBP/USD Weekly Forecast: No reprieve amid Ukraine crisis, focus shifts to Fed and BOE

- Russia-Ukraine war pounds the pound, dragging GBP/USD towards 1.3000.

- Central banks’ decisions are unlikely to offer any relief to cable in the near term.

- GBP/USD remains a ‘sell the bounce’ trade amid looming Ukraine risks.

It was a brutal week for markets, as the tensions between the West and Russia intensified over the latter’s invasion of Ukraine. Risk-off trades dominated almost throughout the week, as investors dumped the higher-yielding currencies such as the pound while seeking safety in the US dollar and gold. Stagflation risks from the Ukraine crisis will continue to spook markets heading into a busy week. Top-tier economic releases from both sides of the Atlantic will be closely followed alongside the US Federal Reserve (Fed) and Bank of England (BOE) monetary policy announcements.

GBP/USD downed to multi-month lows amid Russia-Ukraine saga

Reacting to the weekend’s developments surrounding the Russia-Ukraine war, GBP/USD lost over one big figure on Monday, breaking out of the previous week’s downside consolidative mode. The US dollar capitalized on the safe-haven demand, as Russia’s President Vladimir Putin refused to ease its aggression on Ukraine.

Meanwhile, hostilities continued, as Russia was reported to have accumulated resources to seek complete control of Kyiv. The West continued to pressure Russia by threatening to increase economic warfare. Cable found little relief from the third round of peace talks between Moscow and Kyiv, which resulted in opening up of a humanitarian corridor instead of reaching a diplomatic solution to end the conflict.

Reports that the European Union (EU) would hold a massive bond sale to fund increased energy and defense spending also failed to lift the pound, as the pair accelerated its declines, breaching the 1.3100 level on Tuesday.

The relentless surge in oil prices added to risk-sensitive GBP’s misery, especially after it announced on Tuesday that it will phase out its Russian oil imports by the end of 2022. Comments from Bank of England (BOE) Monetary Policy Committee Member Silvana Tenreyro also weighed negatively, as he warned that rising oil prices could dampen economic activity.

A sudden turnaround in the market midweek, helped the major stage a rebound to just below 1.3200, as investors turned hopeful ahead of Thursday’s peace talks between the Russian Foreign Minister Sergey Lavrov and his Ukrainian counterpart Dmytro Kuleba in Turkey. It was seen as more of a correction across the market, as traders geared up for the peace talks and the critical ECB decision plus US inflation report. The ECB turned surprisingly hawkish while the US inflation rate stood at its highest level in 40 years, which dented sentiment once again while fuelling a fresh upswing in the dollar. Re-igniting risk-aversion was also the failed talks between Moscow and Kiev, which left with no progress on a ceasefire and sent risk trades into a tailspin heading into the week. The month of January’s solid improvement in the UK economy also did little to deter GBP bears, as the spot closed in on the 1.3000 threshold.

GBP/USD: Week ahead

The negative tone in global markets is likely to extend into a busy week, dominated by the Fed and BOE monetary policy announcements while war updates will continue to remain the main market driver.

The high-volatility economic news from the UK and US will also play second fiddle to the Russia-Ukraine conflict. The UK releases its monthly Employment data on Tuesday, with the ILO Unemployment Rate foreseen at 4% in January vs. 4.1% previous. On the same day, the Producer Price Index (PPI) will drop in from the US.

On Wednesday, US Retail Sales data for February will be reported, which will likely show a sharp drop in consumer spending. The FOMC decision, however, will hog the limelight, as the world’s most powerful central bank is set to hike interest rates for the first time since the pandemic began. A 25 bps rate hike is well priced-in amid Ukrainian uncertainty, although Powell’s outlook on the economy, inflation and future rate hikes will also have a major impact on the USD valuations, as well as on market sentiment in general.

The BOE will be the next central bank in focus. It is expected to lift policy rates amid soaring inflation. A more hawkish outlook from the BOE cannot be ruled out after the ECB signaled faster tapering at its March 10 policy decision, despite Ukrainian uncertainty.

Friday is data-sparse, with only US Existing Home sales data on the cards, wrapping up an eventful week. The developments around the war will likely supersede central bank impact on the major.

GBP/USD: Technical outlook

In a significant bearish development, GBP/USD closed below the 200-week MA for the first time since October 2020. Additionally, the Relative Strength Index (RSI) indicator on the weekly chart is still above 30, suggesting that there is more room on the downside before the pair turns technically oversold.

On the downside, interim support is located at 1.3050 (static level) before the pair can target 1.3000 (psychological level). A daily close below the latter could open the door for additional losses toward 1.2920 (static level).

The 200-week MA forms the first resistance at 1.3120 ahead of 1.3200 (psychological level) and 1.3240 (static level).

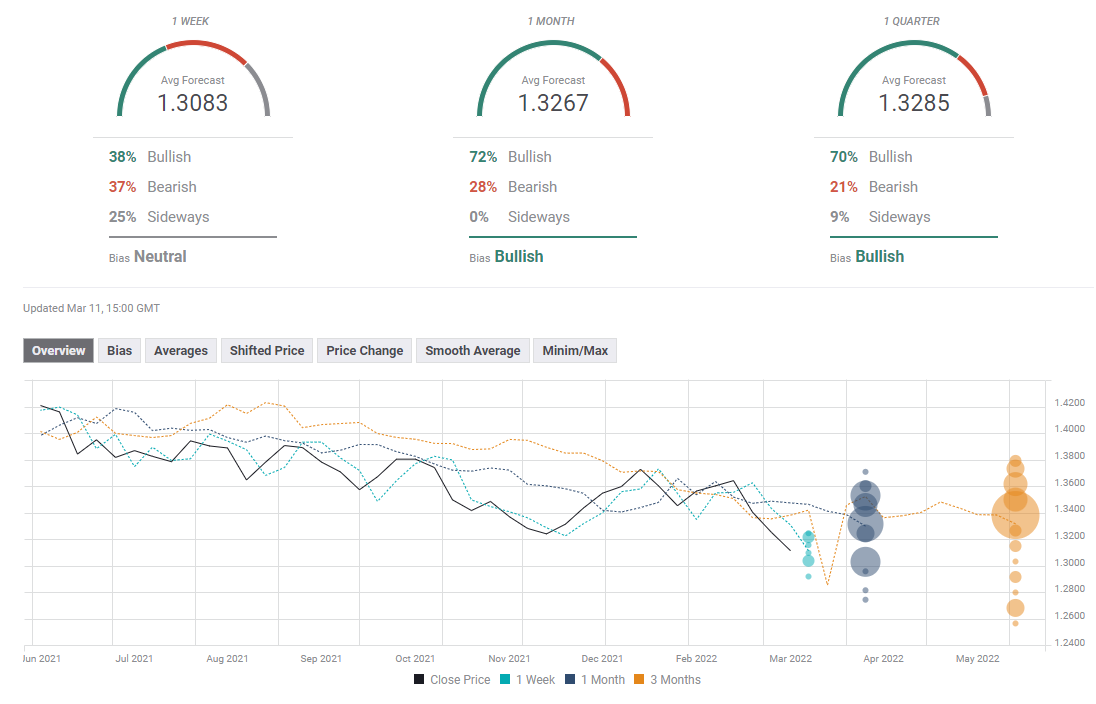

GBP/USD: Sentiment poll

The FXStreet Forecast poll paints a mixed picture for GBP/USD in the near term and the varying views of experts are reflected upon the one-week average target, which sits slightly below 1.3100. The one-month and the one-quarter outlooks remain overwhelmingly bullish.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Dhwani Mehta

FXStreet

Residing in Mumbai (India), Dhwani is a Senior Analyst and Manager of the Asian session at FXStreet. She has over 10 years of experience in analyzing and covering the global financial markets, with specialization in Forex and commodities markets.