GBP/USD Weekly Forecast: Focus remains on stagflation and the BoE

- GBP/USD managed to surpass the 1.3500 barrier, closing the week with gains.

- Investors are expected to keep their focus on the UK fiscal position.

- The BoE is anticipated to maintain its policy rate unchanged this month.

In quite turbulent past few days for the Pound Sterling, GBP/USD eventually managed to close the week with decent gains above the key 1.3500 figure, reversing at the same time two weekly retracements in a row.

While the cautious stance from the Bank of England (BoE) continues to lend some cushion to the currency, speculation that a potential stagflationary scenario could be brewing raised extra concerns among market participants and seems to keep occasional bullish attempts contained.

Adding to worries at home, the health of the United Kingdom's (UK) fiscal position emerges as a headwind to have in mind for investors, at least until Chancellor Rachel Reeves unveils the Autumn Budget in late November.

Fiscal policy and gilt yields keep the Sterling under pressure

After testing the 1.3600 region in August, GBP/USD quickly lost momentum as selling pressure came roaring back. Much of that weakness has been tied to concerns over the UK’s fiscal outlook, which are building as the Autumn Budget draws nearer.

Those fiscal worries spilt over into the UK's money market, triggering a heavy sell-off in gilts. Long-dated yields have climbed to levels not seen since 1998, while the 10-year benchmark touched highs last visited in 2008. That backdrop continues to weigh on the pound.

Inflation and the BoE: The quid’s safety net?

Helping to steady the currency somewhat, the Bank of England’s (BoE) decision to trim its policy rate to 4.00% was a close call, and importantly, it signalled that a steeper easing cycle may not be on the table just yet.

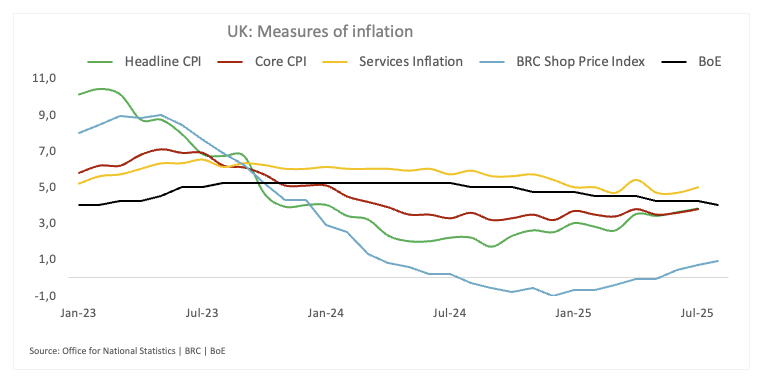

The BoE is stuck in a tug-of-war. On one side, the UK labour market has been cooling, hit by Chancellor Rachel Reeves’ employer tax hike and the spillover from US President Trump’s trade war. On the other, inflation is proving sticky. The Bank raised its forecast for a September peak to 4% from 3.7%, warning that higher food prices could filter into wage demands and lock in longer-term cost pressures.

Adding to the challenge, the BoE has pushed back its timeline for returning inflation to target. Price growth is now expected to reach 2% only by Q2 2027.

July’s data underlined the problem: headline CPI rose 3.8% YoY, with core running at the same pace, while services inflation ticked up to 5.0%. Those numbers leave the BoE little room for comfort and help explain why markets have scaled back bets on cuts this year.

The September 18 gathering looks like a hold, and markets are only pricing in around 26 basis points of easing by March 2026.

BoE-speak leans toward a cautious stance

Governor Andrew Bailey told lawmakers that markets had broadly understood his message about rates moving lower, but admitted there was now more uncertainty about the pace of cuts. He also played down fears that US tariffs were having a major impact on UK inflation.

Deputy Governor Clare Lombardelli and MPC member Megan Greene struck a more hawkish tone, warning that rising expectations were troubling and that policy was not yet tight enough to squeeze inflation meaningfully. By contrast, Alan Taylor argued for a steadier pace of four to five cuts a year, saying wage deals looked consistent with inflation easing back to target and that household expectations had only nudged up modestly.

The split inside the central bank captures the push and pull driving GBP/USD. Bailey’s caution keeps the doves in check, while Taylor’s call for steady cuts leaves the easing story alive. The Sterling, as a result, is stuck navigating between hopes of looser policy and the reality of inflation that refuses to back down.

What’s next for GBP?

It’s a relatively light week for UK data. The BRC Retail Sales Monitor lands on September 9, followed by a busier September 12 with the RICS House Price Balance, GDP figures, trade numbers, industrial and manufacturing production, construction output, and the NIESR Monthly GDP Tracker.

What are techs saying?

From a technical perspective, GBP/USD faces its next resistance at the August top of 1.3594 (August 14). A break above that would open the way toward the weekly peak at 1.3588 (July 24), before testing the 2025 ceiling at 1.3788 (July 1).

On the downside, first support comes at the September base of 1.3332 (September 3), followed by the August valley at 1.3141 (August 1) and the May floor at 1.3139 (May 12). A move beneath that zone would put the 1.3000 psychological level into play.

As long as the pair holds above its 200-day SMA at 1.3062, the broader outlook remains constructive.

Momentum signals remain mixed: The Relative Strength Index (RSI) near 55 suggests scope for short-term gains, but the Average Directional Index (ADX) around 14 shows the trend lacks colour for now.

All in all

The UK economy is holding up a bit better than many feared, but the bigger picture is still clouded by fiscal uncertainty, sticky inflation, and a cooling jobs market. That said, the BoE is expected to keep its prudent stance in place for now, with Chancellor Reeves and the fiscal backdrop remaining firmly at the centre of the debate. Against that backdrop, Cable may find support, but any bull run is likely to remain choppy amid data surprises at home and the policy path from the Federal Reserve (Fed) abroad.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.