GBP/USD Forecast: Bulls seem non-committed after dovish BoE

- A combination of factors assisted GBP/USD to gain strong positive traction on Monday.

- The optimism over the reopening of the UK economy extended some support to the sterling.

- Mixed signals on US inflation kept the USD bulls on the defensive and remained supportive.

The GBP/USD pair kicked off the new week on a positive note and touched an intraday high level of 1.3939 during the early European session. The British pound was supported by the optimism that the UK remains on track to end COVID-19 measures in July. The UK Prime Minister Boris Johnson has said the remaining restrictions will be lifted on 19 July but has also promised a data review to see if this can happen two weeks earlier on 5 July. This, along with a subdued US dollar demand, provided a goodish intraday lift to the major.

The USD remained on the defensive amid mixed signals on the US inflation and was further pressured by a fresh leg down in the US Treasury bond yields. The Fed Chair Jerome Powell, during his testimony before the House Select Subcommittee last week, said that inflation is rising due to pent-up demand and supply bottlenecks and that the price pressures should ease on their own. That said, Friday's Core PCE Price Index showed a notable acceleration and shot to 3.4% YoY in May, marking the largest gain since April 1992.

Investors, however, remain concerned that the Fed would tighten its monetary policy if inflationary pressures continue to intensify. Apart from this, the Bank of England's dovish stance might hold investors from placing any aggressive bullish bets and keep a lid on any further gains for the major, at least for the time being. There isn't any major market-moving economic data due for release on Monday, either from the UK or the US. This further makes it prudent to wait for some strong follow-through buying before confirming that the pair has bottomed out in the near term and positioning for any further appreciating move.

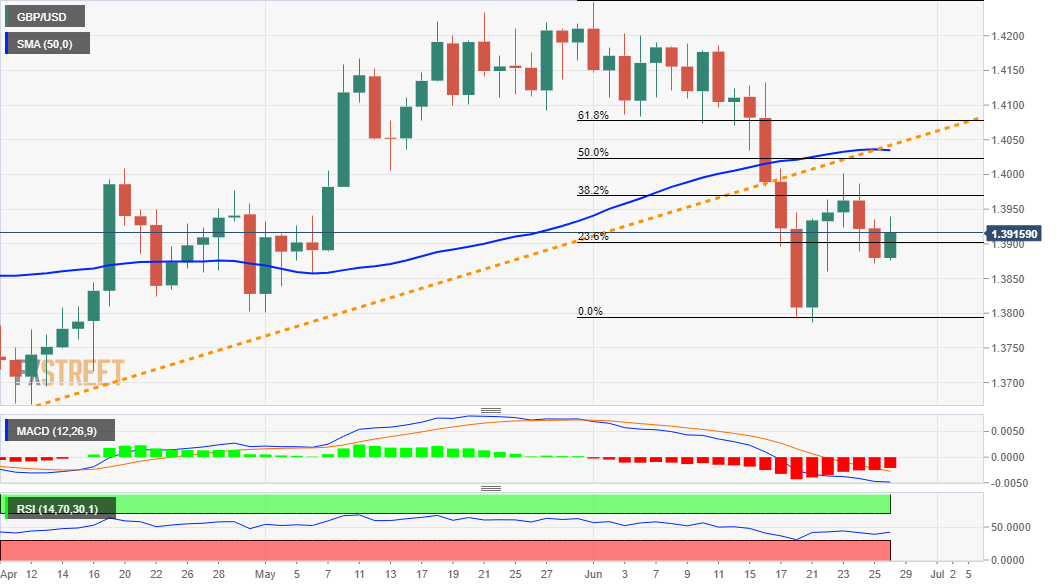

Short-term technical outlook

From a technical perspective, last week's solid rebound from sub-1.3800 levels stalled near the 50% Fibonacci level of the recent corrective slide from multi-year tops. The mentioned hurdle around the key 1.4000 psychological mark is closely followed by the 50-day SMA and a short-term ascending trend-line support breakpoint, around the 1.4030 region. A sustained strength beyond will negate any near-term negative bias and push the pair beyond the 61.8% Fibo. level, around the 1.4070 region, allowing bulls to aim back to reclaim the 1.4100 mark.

On the flip side, the 1.3870 region now seems to have emerged as immediate support. A convincing break below will be seen as a fresh trigger for bearish traders and turn the pair vulnerable to resume its recent corrective fall from the vicinity of mid-1.4200s, or the highest level since April 2018 touched earlier this month. The next relevant support is pegged near the 1.3800 mark ahead of monthly swing lows, around the 1.3785 region. Some follow-through selling now seems to pave the way for a slide towards the 1.3700 mark en-route the 1.3670-65 support zone.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Haresh Menghani

FXStreet

Haresh Menghani is a detail-oriented professional with 10+ years of extensive experience in analysing the global financial markets.