G10 FX Week Ahead: With a little help from my friends

While monetary and fiscal policy have moved in tandem in the US, coordinated fiscal measures (coronabonds) have still not found enough 'friends' within the EU. Meanwhile, the USD funding concerns may ease further this week, fuelling more USD weakness. JPY, EUR and CHF should reap the most benefit, while the rebound in pro-cyclical FX looks vulnerable.

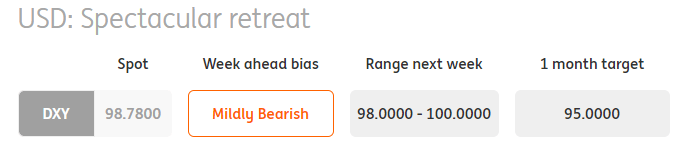

USD: Spectacular retreat

The dollar’s remarkable turnaround last week owed a lot to: i) the Fed’s commitment to unlimited asset purchases and ii) some modest signs of improvement in USD funding markets. Over the last three weeks the Fed’s balance sheet has grown by a trillion dollars and by the end of this current rescue operation it could be $9-10trn in total. The Fed typically over-delivers at times like these and, as we have noted before, would expect a weaker dollar to play its role in this reflationary exercise. We would expect this flood of liquidity to start to take some of the volatility out of FX markets, but it will take some time. Notably the Fed’s commercial paper buying programme may not start for a week or two and the still elevated levels of 3m $ Libor warn that dislocations take time to fix.

Now that the $2trn fiscal stimulus bill has been passed, investors are left to assess the size of the draw-down in activity that needs fixing. Sharp falls in ISM business confidence readings this week are fully discounted and on Friday we will see the March jobs report. That should show sizable job losses and the market will focus on the household unemployment rate. The length of current lockdowns is a new variable for the market to monitor. Overall, we do now have greater confidence that the dollar has peaked against G3 currencies and should be trending lower into the summer.

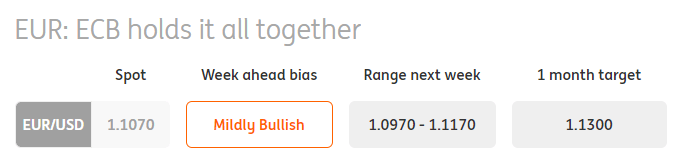

EUR: ECB holds it all together

One-month EUR/USD implied volatility remains high at 10%, largely because realised volatility remains at 15%. Volatility should start to settle, however, as policymakers work their way through the list of market distortions. As above, measures are underway to address the USD funding squeeze, (we’ve already seen the EUR basis narrow substantially), but it may take a couple more weeks before conditions normalise. So far the EUR has managed to take advantage of the turn in the dollar – largely down to aggressive ECB measures. Its early support of EZ peripheral debt with the Pandemic Emergency Purchase Programme is so far preventing the economic shock from turning into a new European sovereign debt crisis.

This week the European macro focus is on economic confidence figures and then the March CPI. Inflation should be dragged lower by oil prices, which are still in sharp decline. Presumably, there will also be more focus on the possible use of the ESM (allowing ECB OMT purchases) and the scope for a coronabond. It still seems, however, that northern Europe frowns on such collective issuance. Expect further modest EUR/USD gains this week, but perhaps with less volatility.

JPY: GPIF news is old news

Dollar funding demand from Japanese banks ahead of the 31 March fiscal year end looks set to dissipate and is helping to cement this turn lower in USD/JPY. Expect much press attention this week to be given to the new Japanese fiscal year and the investment intentions of the Government Pension Investment Fund (GPIF). It is widely expected to announce a 10% increase in weights to foreign bonds, which ultimately may be worth a JPY15-20trn outflow. In a recent article, however, we made the point that the GPIF was unlikely to be pouring money into foreign debt markets when i) the foreign debt yield advantage over JGBs was crumbling and ii) USD/JPY was above 110 and volatile. We see this week’s GPIF story more as a case of buy (USD/JPY) on the rumour and sell the fact.

Late last week we also saw USD/JPY re-connecting with its typical stock market correlations. That makes sense because Japan’s large (and potentially larger on low oil prices) current account surplus gives the JPY good insulation at a time of stifled portfolio flows. Volatility should slowly edge lower, but so should USD/JPY as the Fed’s flood of dollars starts to make its way slowly through the system.

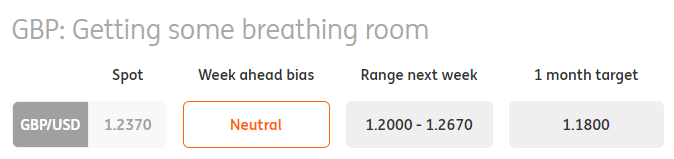

GBP: Getting some breathing room

As the rebound in risk assets is likely to pause so should sterling's gains. Still, the GBP position now looks better as the declining USD funding concerns makes the currency less to stand out on the negative side. Here, the worst current account position in the G10 FX space and its external funding needs made sterling vulnerable during the dollar funding squeeze sell-off.

Our financial fair value model suggests that GBP is now back close to its short-term fair value levels. This points to a limited need for further correction in the spot. GBP/USD direction will also be in large part driven by the EUR/USD move. On the domestic data front, it is a fairly quiet week. No new fiscal measures from the government are expected either.

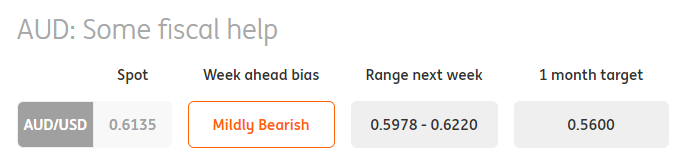

AUD: Some fiscal help

A 5% recovery in AUD/USD last week has largely been a function of the USD giving up recent gains as funding worries eased. In fact, the Reserve Bank of Australia has ramped up its bond-buying activity last week and has so far purchased AUD24bn since announcing quantitative easing (QE). Given the explicit aim to control the front-end of the curve, the Bank has concentrated its purchase on short-term bonds, which has contributed to a further steepening of the curve. It will remain to be seen whether an excessive steepening may prompt the RBA to buy longer-term bonds, which however remain highly dependent on the UST, given the relatively small Australian bond market.

This week, we think that the balance of risks for the pro-cyclical currencies is skewed to the downside as markets probably held an excessively sanguine stance on risk sentiment this week. As AUD was amongst the key outperformers this week, we see room for some reversal, also helped by the RBA bond buying, which may increase in size over the next few days. However, the third leg of the fiscal stimulus package deployed by the Australian government (bringing total stimulus to AUD 230bn, or about 16% of GDP), may partly cushion the losses and AUD may outperform its cyclical peers this week.

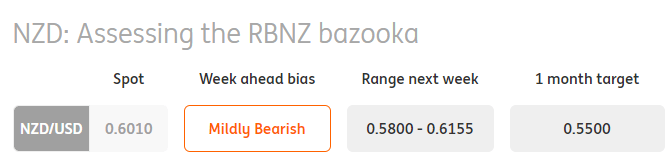

NZD: Assessing the RBNZ bazooka

The Reserve Bank of New Zealand announced its own bazooka last Monday and will purchase up to NZD30bn of government bonds across various maturities for the next 12 months. We analysed the implications for the New Zealand dollar in What the Kiwi bazooka means for NZD. Our feeling is that what is surely a substantial QE package has not shown its marks on NZD as the USD funding story drove most of the moves in global FX.

Now that the dust has settled, we suspect NZD faces a sizeable risk of a downward correction due to the highly unsupportive rate environment. We expect most of NZD weakness to be channelled against low-yielders, in particular JPY. Looking at AUD/NZD, we struggle to see the pair consistently trading at parity as the notion that led it to briefly touch 1.00 earlier in March was the RBNZ lagging the RBA in unorthodox monetary policy. After the RBNZ bazooka, this is clearly not the case anymore.

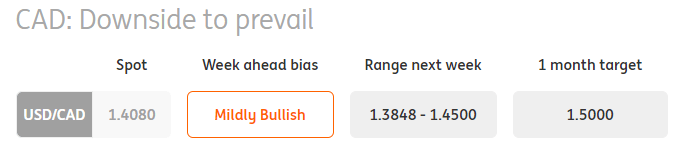

CAD: Downside to prevail

Early last week, we called for 1.50 in USD/CAD as the combination of low oil prices and our expectation for Bank of Canada cuts and QE warranted another leg lower in the loonie. The major correction in the USD, however, pushed the pair back from 1.45 to the 1.40 area, despite the BoC delivering on its aggressive easing package (50bp cut and QE).

Sticking to our 1.50 call would at this point imply a substantial recovery in the USD along with CAD weakness, and this may not be the case as USD funding fears seem to have abated. However, this has not made us change our mind on how fundamentals keep pointing at CAD weakness. As highlighted by our commodities team, oil is still likely to face downside pressure, while the BoC’s QE (for now, a minimum of CAD5bn a per week) may be ramped up (similar to the what the Fed did) in the next weeks. For now, we expect a move back towards the 1.45 area in USD/CAD, but we expect more weakness of the loonie in the crosses, especially versus low yielders.

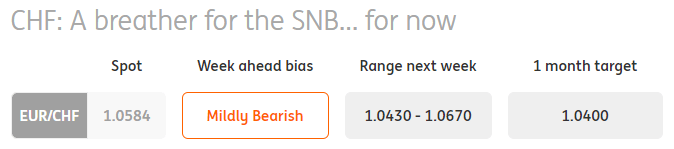

CHF: A breather for the SNB... for now

The rebound in equities dragged down safe-havens including the Swiss franc, and allowed the Swiss National Bank to temporarily ease its FX interventions to curb CHF appreciation. EUR/CHF is back to the 1.06 area, but the question now is, for how long?

As liquidity and USD funding fears have abated, markets may now start to look to the longer term. With a global recession – the length and depth of which are still highly uncertain – about to be fully priced in, the risk is of another flight-to-safety, to the benefit of the franc. Incidentally, the disagreement within the EU around the measures to offset the impact of the virus are now sparking speculation about the future of the Union and the eurozone itself. CHF is the quintessential hedge to such scenarios, which means the SNB’s headaches may be far from over.

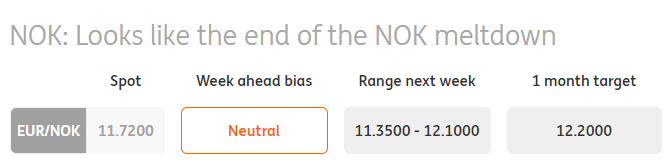

NOK: Looks like the end of the NOK meltdown

With the USD funding issues easing, Norway's krone should be less vulnerable (the low liquid NOK has been the key G10 FX victim in the recent search for the USD cash environment). This is not to say that EUR/NOK cannot re-test the 12.00 level again (this is still on the cards if investors' concerns about the Covid-19 impact on global economy rise further), but we now expect the abrupt currency volatility to decline from the ultra-elevated levels (ie, no longer the around 5% daily moves in USD/NOK observed in prior weeks).

As the dollar funding issues ease, the profound NOK undervaluation may now (and finally) start to play a larger role and may be thus limiting the scale of NOK downside. Equally, the persistently depressed oil prices suggest that the scope for a meaningful NOK rebound may be limited as well. In the current markets, domestic Norwegian economic data won’t matter for NOK.

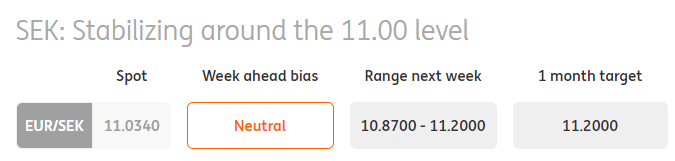

SEK: Stabilizing around the 11.00 level

EUR/SEK is stabilising around the 11.00 level. Sweden's krona has lagged the NOK gains in the last week’s risk rebound, but this is understandable given the sharp NOK sell-off during the past weeks as well as the prior SEK outperformance vs its G10 cyclical peers. For the week ahead, we expect EUR/SEK to stabilise around the 11.00 level, with the pair’s volatility declining (in line with the trend in the wider G10 FX world).

So far, the Riksbank has been a relative outlier during the current crisis. Indeed, no rates cuts (like BoC), no QE (like RBNZ) and no threat of FX interventions (like NB) from the Riksbank underline the relative stance of SEK – the currency being the outperformer in the G10 cyclical space during the Covid-19 crisis. No easing was done by the Riskbank and not much is expected at this point.

Read the original analysis: G10 FX Week Ahead: With a little help from my friends

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.