Fuse has been lit

S&P 500 didn‘t surprise, and delivered the dead cat bounce that I was looking for at the onset of Friday:

(…) We‘re in for a dead cat bounce attempt today – even if import prices don‘t point to yet another source of quickening domestic inflation, the quickening export prices pace reveals that U.S. inflation is being also directly (not just via exchange rates) exported.

The point is how far it can carry the stock buyers, and whether the turn in bonds can be classified as risk-on. It has the potential to turn into risk-on retracement of the S&P 500 downswing as Nasdaq can kick in (tech largely missed Friday‘s retreat in yields, still digesting Mester and Bullard talk of 5.50%). Yes, it‘s all a play of yields and yields differentials when it comes to the much touted emergning markets story at the beginning of 2023 – Fed stepping up to the tightening plate as inflation data confirmed my calls of sticky and returning inflation, is a game changer for the greenback too (relief rally goes on, and the world reserve currency wouldn‘t be as weak in 2023 as the hype would have you believe).

More tightening deals with the „no landing“ thesis (i.e. that recession has been avoided and the economy would just continue expanding as the job market is still largely unscathed) that markets were carried away with earlier in the week – it works to tighten financial conditions, pressure real estate a lot more, increase the cost of capital (hitting tech hard – this has to still play out, e.g. around NVDA earnings), and decrease disposable income, which would sooner or later show up in retail sales, but for now is masked by still good consumer debt serviceability.

All in all, the Fed is pausing later rather than sooner – and that‘s what markets started discounting only on the PPI data arrival. Coupled with positive data from Europe and continued focus on tightening around the world, the pressure on stock prices and valuations vis-a-vis what‘s risk-free, grows already premarket on PMI data. Fed funds rate is still far from observing the Taylor rule, and I doubt the Fed can get rates there, let alone to 6%+ before short-term bond yields top out in summer.

This alone has powerful consequences for growth stocks, which are set to face a major rotation out of later this year. For now, they are cushioned by yields trying to retreat on approaching recession, but with the Fed staying the hawkish course (this force is to win out, careful bond bulls), tech would undeniably suffer. These stocks can run only so far when the focus isn‘t on immediate profitability and without the risk-free Treasuries return so appealing (T-bills are at 5% now, making it an interesting 2023 proposition for those unwilling to go long equities on a long-term basis).

Let‘s bring up Friday‘s analysis:

(…) While inflation returning is bullish real assets, the USD upswing and rising rates (now practically comparable to the S&P 500 earnings yield – redefining what‘s risk-free and overpriced) serve as a powerful drag on especially precious metals (no local bottom there – as per prior Thursday‘s premium analysis, the short-term tune has changed, and it would take many weeks to see one), and copper amid all the supply deficits pointing to inflation‘s resurgence, won‘t save the day.

A lot of deleveraging ahead still as the overly loose financial conditions get tightened – both by the Fed and commercial banks. Don‘t forget the Treasury general account and repo facilities when assessing conditions. What‘s the terminal Fed funds rate, is being redefined from 5.50% upwards, and the yields differential to the rest of the world, is responsible for the USD upswing. Hear that sucking sound of liquidity (to still) disappear!

Buy the dippers will try again, and would struggle at 4,095 – 4,105 area – doubtful they can get there today. Market breadth and volatility are rather silently supporting the topping process as having been well underway already, and one that wouldn‘t be developing in a one way fashion. 4,040s would take time to break, and require continued leading weakness in the riskiest of bonds, the junk ones. We‘re getting there, and getting today‘s options expiry volatility out of the way, would be very constructive for the bears.

All those earnings to disappoint, layoffs to spread, and recession arrival quickened by more hikes and balance sheet shrinking, will power the coming very significant stocks decline. And precious metals refusing to keep declining more, would a sign we‘re getting ready to rally, not just in real assets but including in stocks.

Of course, that‘s a long-term perspective – one measured in months rather than weeks.

Keep enjoying the lively Twitter feed serving you all already in, which comes on top of getting the key daily analytics right into your mailbox. Plenty gets addressed there (or on Telegram if you prefer), but the analyses (whether short or long format, depending on market action) over email are the bedrock. So, make sure you‘re signed up for the free newsletter and that you have my Twitter profile open with notifications on so as not to miss a thing, and to benefit from extra intraday calls.

Let‘s move right into the charts – today‘s analysis is exceptionally open freely in full to see what subscribers get.

S&P 500 and Nasdaq outlook

4,095 – 4,105 is the daily target for the bulls to overcome, but I see them struggling and without real initiative. I doubt they can make it as far as 4,150 area during this week at all. The ingredients for a bond market rally aren’t there, and rotation into cyclicals won’t be strong enough to fuel a series of 1%+ daily reversal indefinitely. Bears though need to be patient in grinding lower – the 4,040s area would take some work to break, but it’ll give in. The conditions for a powerful decline to 4,010s and couple of hundreds of points below, are in place, the fuse has been lit.

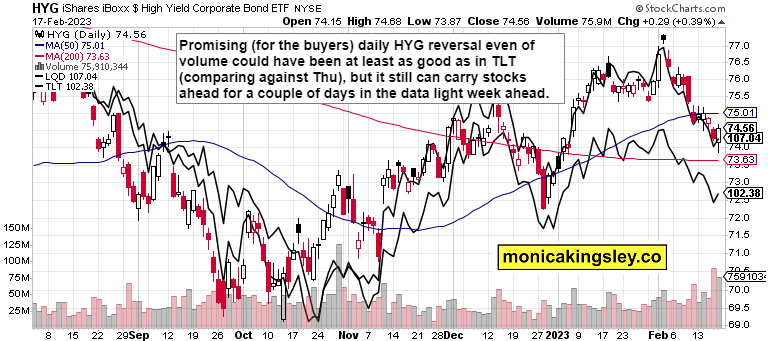

Credit markets

Bonds are to temporarily support the rebound attempt in stocks, but their underperfomance for at least two last weeks (if you don’t look at longer time series) is out in the open, visible to the naked eye, just as much as VIX waking up.

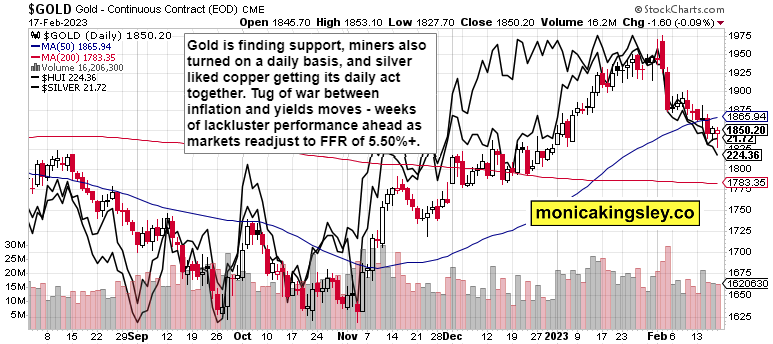

Gold, Silver and miners

Gold and silver are trying to stabilize, and would welcome some bond market strength. The recent downswing has been amplified by the dollar waking up, and its more range bound action medium-term (once the new hawkishness gets absorbed), would bring relief to the metals, as these would rise on inflation and recession themes. Best case scenario is consolidation in time rather than price for the metals here, with silver defending the 200- day moving average.

Crude oil

Oil is to recover not only thanks to China moves, and together with services inflation, and the job market remaining more resilient than during prior recessions, would fuel the inflation woes, forcing the Fed to tighten really above 5.50% in the end. The sectoral fundamentals are bullish, and recession isn‘t knocking on the door in the least yet (that would happen late Q2 2023). Of course, copper would lead oil higher.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.