Four out of G10

Central banks

In most cases, the G10 central bank stories for December are starting to converge on a single outcome. Here is the state of play:

Fed

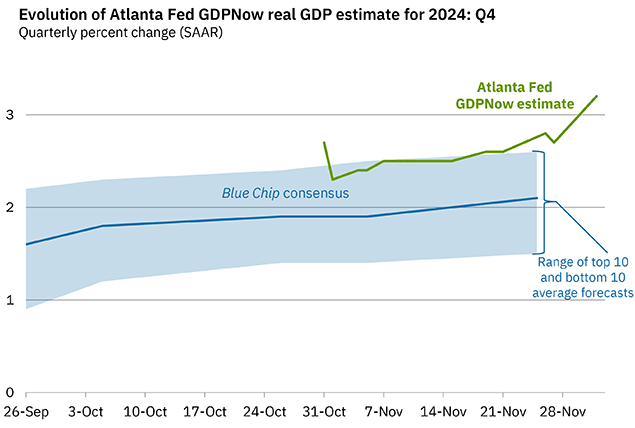

My interpretation of Waller’s speech this week is that his prior probability for a December cut was around 75% before the data. JOLTS should make it a bit lower, but NFP and CPI will be the deciders. 74% feels a bit high to me with Atlanta Fed GDPNow making new highs, ISMs perky, JOLTS higher, inflation no longer falling, and so on. We are in a solid economy with upside inflation risk from tariffs and downside growth risks from government restructuring.

Policy uncertainty is high enough to offer an excuse for any Fed voter who prefers to pass in December, so buoyant NFP and CPI and the cut odds are going to collapse from 75 to 10 pretty fast. Prefer to be paid the December meeting given risk/reward and risk of strong data.

ECB

December meeting priced for 27bps, and that looks right. Here are the important ECB comments over the past week or so. Given how little of a chance of 50 is priced, and the near-absolute certainty of 25… Risk/reward is pretty good to receive the meeting. It’s a cheap option on a change of heart where the doves become more vocal and the hawks shrug and say OK.

ECB'S VUJCIC: Small steps on rates better amid uncertainty

ECB'S Holzmann sees likelihood for a moderate rate cut in Dec.

KAZAKS: Data-dependent, gradual ECB approach still appropriate

KAZAKS: Likely to discuss bigger Dec. cut but uncertainty high

GUINDOS: Nobody in ECB council knows what will happen in Dec.

ECB'S STOURNARAS: Tariffs could warrant aggressive rate cuts

ECB'S VILLEROY: Should remain open on size of December cut

ECB has significant room to remove restrictive policy: Villeroy

ECB’S schnabel sees only limited room for further rate cuts

SCHNABEL: ECB can gradually move rates to neutral, not lower

BoJ

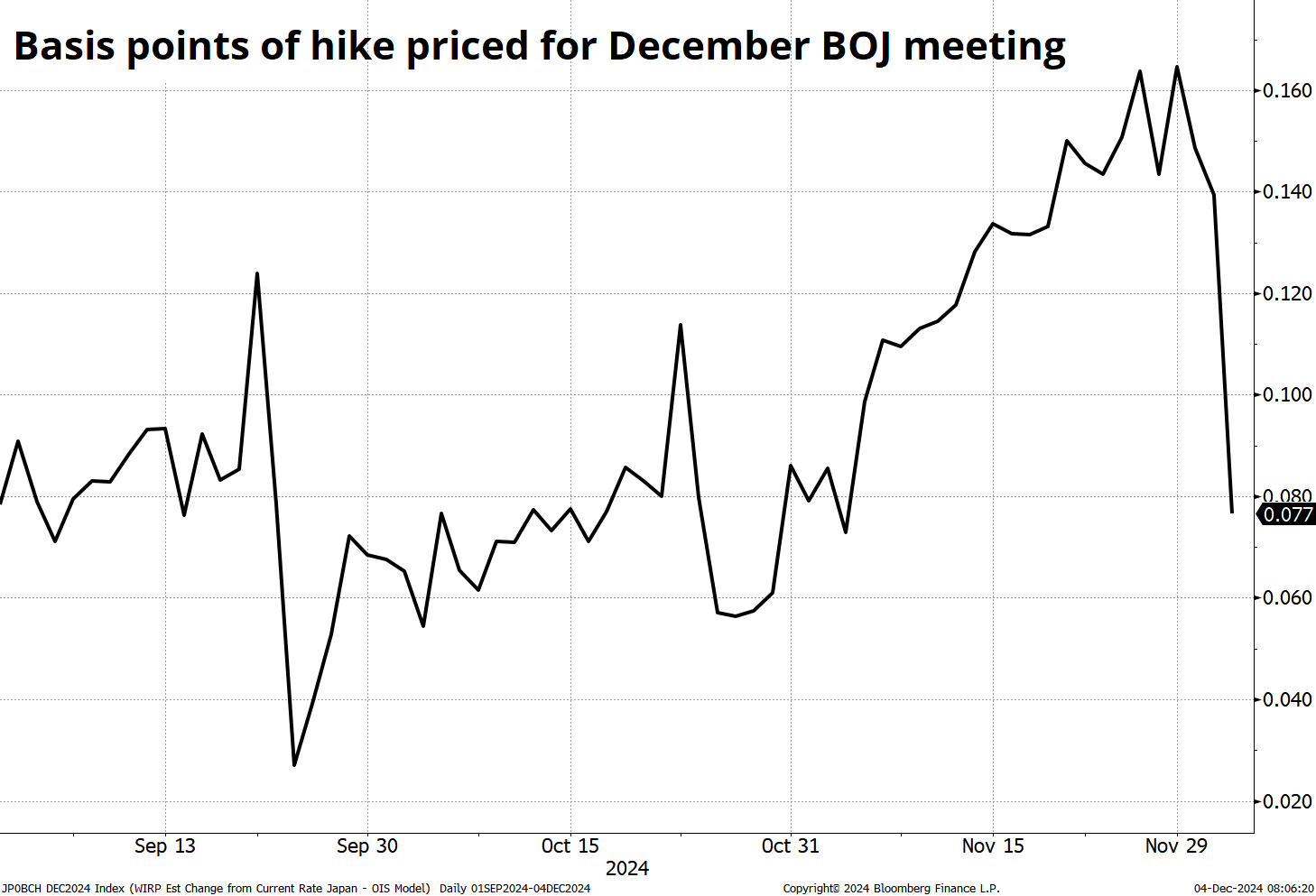

December rate hike odds have reversed significantly on the back of a JIJI article (since retracted), an MNI article, and some political noise. We went from pricing 15bps to now just 7bps and this has triggered a major short squeeze in cross/JPY and USDJPY. This looks like an overreaction at first because the Nikkei is back near the highs (reduced financial instability risk from a hike), the JPY is neither here nor there at 152, and the politics of hiking rates in December vs. January are not particularly different.

But the hike was probably overpriced given the recent drop in USDJPY and now it’s probably about right. Cash Earnings data tomorrow night at 6:30 p.m. matters as the BOJ seems ready to hike given inflation and wages, and a strong report there could still push them over the line.

151.70/00 is the USDJPY sell zone as there are multiple layers of resistance up there, including the 200-day MA at 151.99.

SNB

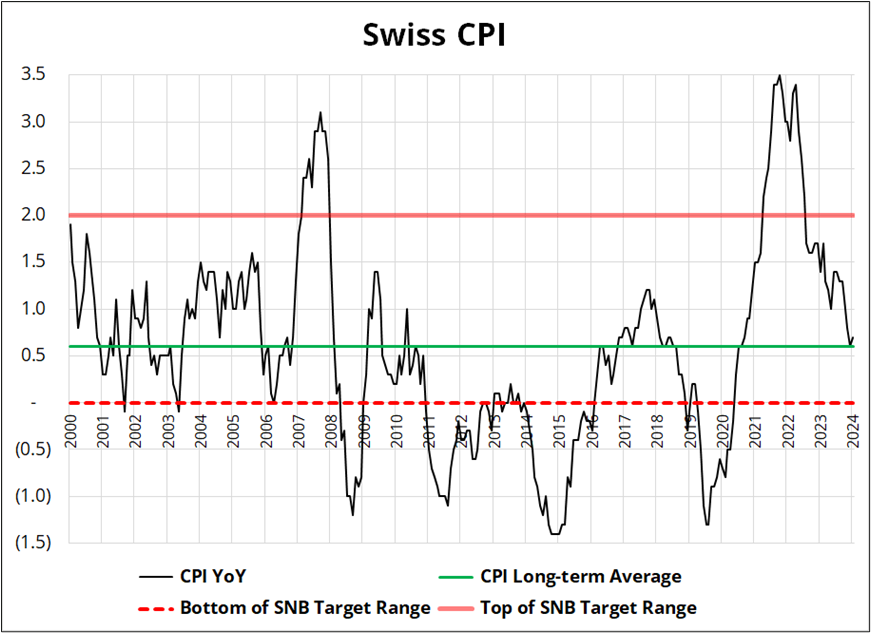

The SNB is the most interesting meeting, as it’s priced exactly 50/50 for 50. As an outsider, inflation looks alarmingly low in Switzerland, but for Switzerland, YoY inflation of 0.7% is actually not that odd. The current SNB target rate is 1.0% and the implied rate for September 2025 is one bp below zero (i.e., -0.01%). Schlegel has consistently been saying that negative rates could come back, and they don’t seem particularly panicked about that fact, but that’s an obvious statement as they will never remove that optionality. Board member Petra Tschudin sounded pretty chill in a November 21 interview, saying: “Inflation is now comfortably in the range of 0% to 2% where we want to see it.” Here is the inflation situation in the Swiss Confederation:

It’s very important to note when dealing with Swiss Inflation data that it is not seasonally adjusted. Therefore, we can be almost certain that inflation is about to bounce as we approach the seasonal nadir for Swiss prices.

Swiss inflation is at its 25-year average and it’s likely to bounce in the new year. I don’t think the SNB will go 50bps in December, unless the ECB does it first. The ECB meeting is on the 12th of December and so the SNB made a scheduling mistake. They should really put their meetings after the ECB meetings given the importance of the exchange rate to their policy and the importance of ECB meetings to the exchange rate. Anyway, I think the SNB cuts 25, not 50.

This view runs counter to my current USDCHF long, but I will be out of the USDCHF well before the SNB meeting.

It’s actually O Canada (sir)

Extracting meaning from Donald Trump’s Truth Social post yesterday feels a bit like decoding a Q drop. He says: “Oh Canada!” while looking past a Canadian flag and out over the Swiss Alps. What does it mean?! Why are we here!??!?

Trump appears to be schoolyard bullying Canada with particular vim right now for some reason, and it makes me wonder if he has something more nefarious up his sleeve… Like, maybe tariffs on Canadian crude oil? He can attach some sort of random reasoning based on fentanyl or whatever and achieve two goals at once: Target a large trade deficit “offender” and benefit US oil producers by making Canadian producers dramatically less competitive overnight.

Just a theory. With its reliance on US exports, its creaking housing market, and an enormous consumer debt pile, the vulnerabilities for my homeland are starting to stack up.

3-month 1.45s in USDCAD are cheap and I think they are positive expected value. USDCAD is up 560 pips in the past 8 weeks. Another 500 pips, quick, is easily doable if Canada gets tariffed.

Author

Brent Donnelly

Spectra Markets

Brent Donnelly is the President of Spectra Markets. He has been trading currencies since 1995 and writing about macro since 2004. Brent is the author of “Alpha Trader” (2021) and “The Art of Currency Trading” (Wiley, 2019).