Forget resilience, consumers defiant in February splurge

Summary

Nominal consumer spending shot up by the most in a year in February. Consumers are primarily deploying their outlays in the service sector and that is problematic because it is disrupting progress in bringing down service price inflation.

Amid spending surge, where's the incentive to lower prices?

The days are getting longer and so is the wait for the Fed to lower interest rates. That is partly because consumer outlays have not been slowed by higher borrowing costs as evidenced by the 0.8% increase in nominal spending in February. That is the biggest jump in spending in over a year and a half. Even after adjusting for inflation, real consumer spending rose 0.4%.

Consumers had cut back on goods in January, but this category posted a 0.1% gain in February. Where consumers are really splurging is on outlays in the service sector where real spending jumped 0.6%. That is the biggest monthly jump in real services outlays since the wild summer of 2021 when consumers were still flush with pandemic-era savings and residual stimulus was still very much in play. Every category within services reported an increase in real spending. This is problematic for policymakers because as long as consumer keep splashing out in the service sector, the businesses that provide these services have no incentive to ease up on pricing.

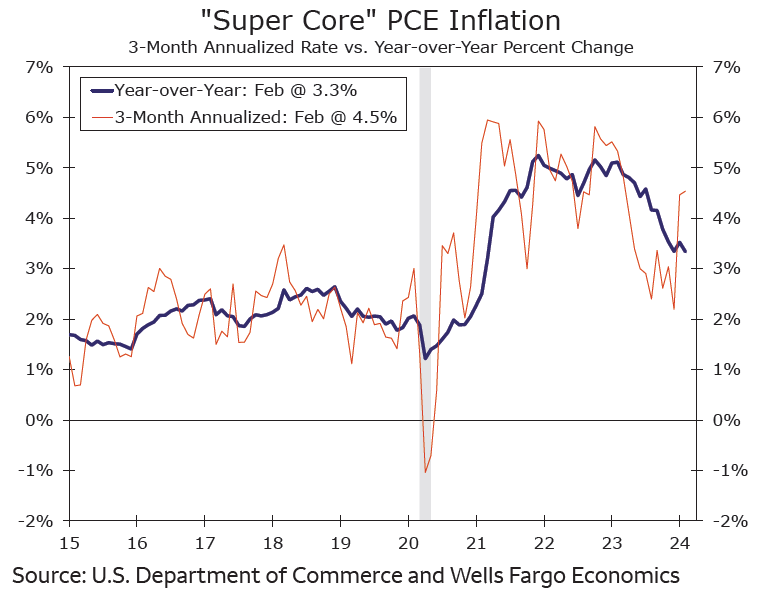

The inflation rate for services less housing, or super-core inflation came in at 3.3% year-over-year, but the three-month annualized rate of 4.5% points to a problematic rise in service sector pricing (chart). While financial markets may take some comfort in the annual rate of the core PCE deflator coming in at 2.8% with a slightly smaller-than-expected monthly rise of 0.3% in February, service prices are no longer cooling as they were a few months ago.

Author

Wells Fargo Research Team

Wells Fargo