Forex markets consolidating ahead of ECB monetary policy

Market Overview

Forex markets are consolidating ahead of the main risk event of the week as the ECB gears up for its latest monetary policy announcement. The market is very long on the euro, and subsequently there is an expectation that Mario Draghi will lay some ground work for ECB tapering later in the year. There will be no changes to interest rates (we still likely to be at least a year out from that), however with growth improvements and the strength of soft data such as the PMIs, there is likely to be an upbeat ECB President. However, with the strong run higher of the euro in recent weeks and extended positioning , there is a risk of profit taking if the market deems that Draghi does not at least set the market up for a September tapering of asset purchases. The ECB is not the only bank to report today though. Overnight, we had the Bank of Japan announcing no change to its monetary policy. There is a juggling act of ever slipping inflation forecasts but improving growth prospects. Subsequently although growth forecasts have been upwardly revised the BoJ now does not expect to hit its 2% target until “around 2019” which hardly instills confidence in that forecast either.

Wall Street closed positively again with earnings once more helping the market higher, with the S&P 500 +0.5% at 2474. Asian markets were broadly positive overnight and European markets are in a similar vein. In forex there is a consolidation across most of the majors, although the Aussie has just ticked lower in the wake of stronger employment data which showed very strong improvement in full time jobs. After the strength of the bull run, some profit taking on the Aussie would not be a huge surprise at some stage soon anyway. Commodities are all but flat with a very mild dip on gold and silver, whilst oil is holding on to yesterday’s gains after another larger than expected EIA drawdown.

The main event of the day is the ECB meeting, however sterling and FTSE 100 traders will be focusing initially on UK Retail Sales which are announced at 0930BST. Retail Sales are expected to pick up by +0.5% ex-fuel after last month’s dreadful -1.6% decline, a number that would pull the year on year reading back to +2.5% (from +0.9% last month). The ECB monetary policy decision is at 1245BST and despite the talk about tapering, could actually be a bit of a damp squib. Rates will not be changed from the 0.0% main refinancing rate and -0.4% on the deposit rate. However there will be more interest in the Draghi press conference at 1330BST in which the ECB President will be pushed on the discussion of tapering. It will likely be too early this month, but that will not stop the journalists asking him questions. Quite how straight he answers them could determine whether the euro holds on to recent gains or not. US weekly jobless claims are at 1330BST and are expected to once more stay around recent levels at 245,000.

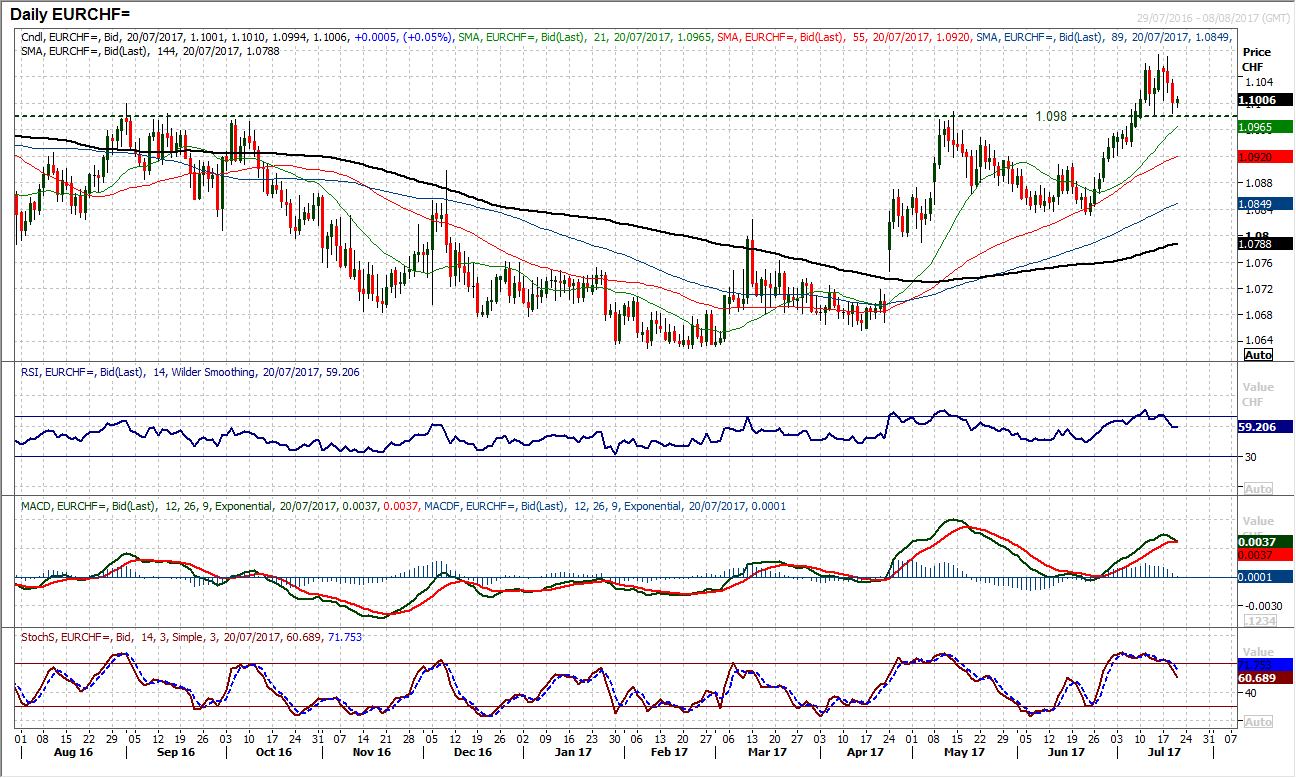

Chart of the Day – EUR/CHF

As the ECB prepares to announce monetary policy there has been an interesting rolling over on Euro/Swissy which could point to waning momentum in the euro rally. After three days of progressively more corrective candles, the market is putting increasing pressure on the breakout support around 1.0980 which had been the key May highs subsequently turned supportive. This 1.0980 pivot also tracks back to August to October highs, so is of historic importance. However this has now become a neckline of a potential top pattern which would imply around 80/90 pips of correction if breached. This would imply a corrective near term target of 1.0890/1.0900. The deterioration in the momentum indicators with a sell signal on the Stochastics crossing back below 80 for the first time in three weeks, whilst the RSI is also below 60 for the first time in three weeks. Hourly momentum also reflects this deterioration in the pair in the past day or so and the pressure on 1.0980 is mounting. This is a key level to watch for the ECB meeting and press conference.

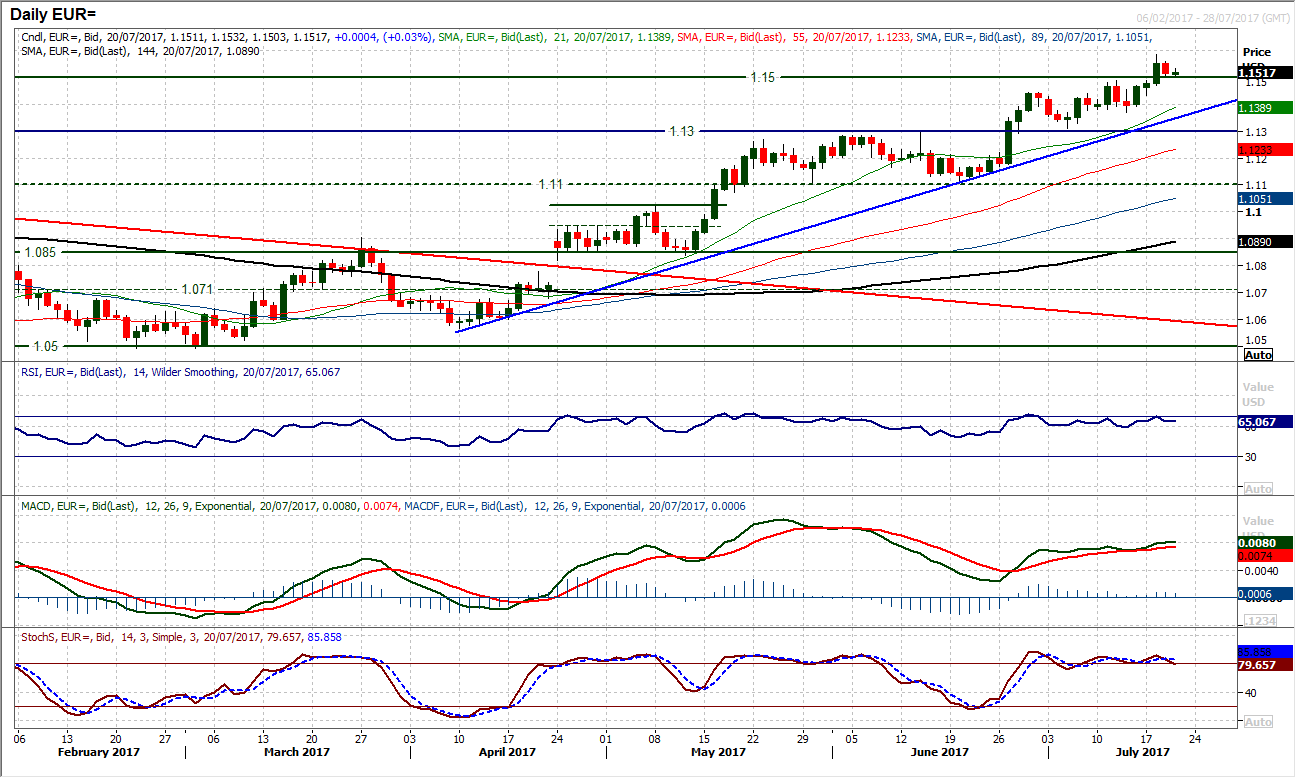

EUR/USD

After a mildly corrective candle yesterday, euro traders are consolidating in the run to the ECB meeting announcement and press conference this afternoon. The trend has been continually strong over recent weeks with a sequence of higher lows and strong momentum. Technically very strong, the outlook continues to suggest buying into weakness. Yesterday’s high of $1.1583 comes just below the $1.1614 May 2016 key high. However, if the euro has run ahead too far, whilst the ECB gives off a less hawkish than expected message this afternoon, then some profit taking could easily set in. The previous breakouts are supportive with $1.1445/$1.1490 the latest levels to watch initially, with $1.1270 being a higher reaction low and $1.1300 being key. The uptrend is supportive at $1.1345 today.

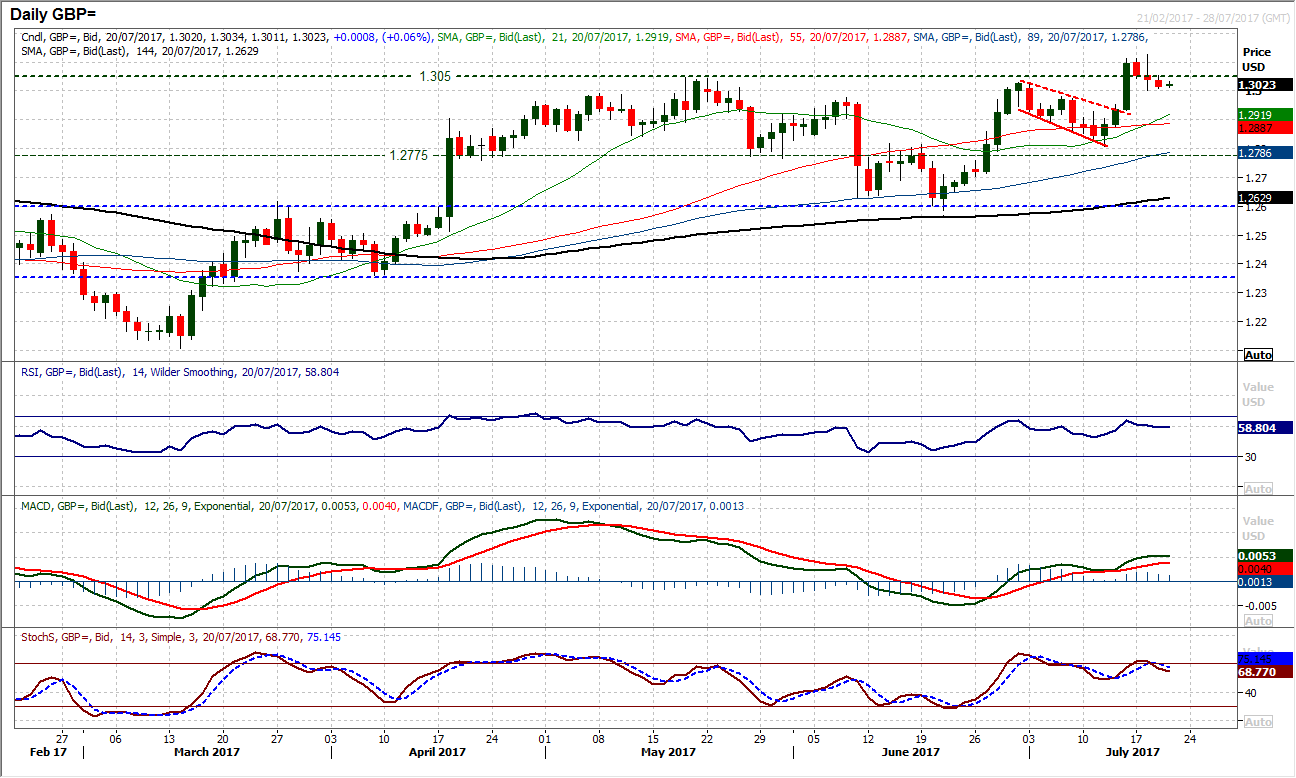

GBP/USD

Cable continues to hold on to the psychological support around $1.3000. However there is still a corrective drift that threatens to turn into something more substantial. A close back below $1.3000 would give the bears something to go on today. For now though there is a minor negative reaction to the Stochastics but essentially the $1.3000/$1.3050 support band is holding, however, equally the $1.3050 level was also a barrier yesterday.. Yesterday’s mild negative candle also now means three in a row but the market seems to be in consolidation mode today. There are two fundamental factors that traders will be watching, the UK Retail Sales and then the ECB. Both are key tier one data that will impact on Sterling/Dollar. A close below $1.3000 and the old reaction high at $1.2982 would increase the corrective momentum, with the key support at $1.2808 from the July low. The hourly chart shows the market just settling down for the key risk events of the week. Initial resistance is around $1.3050 with $1.3125 now key.

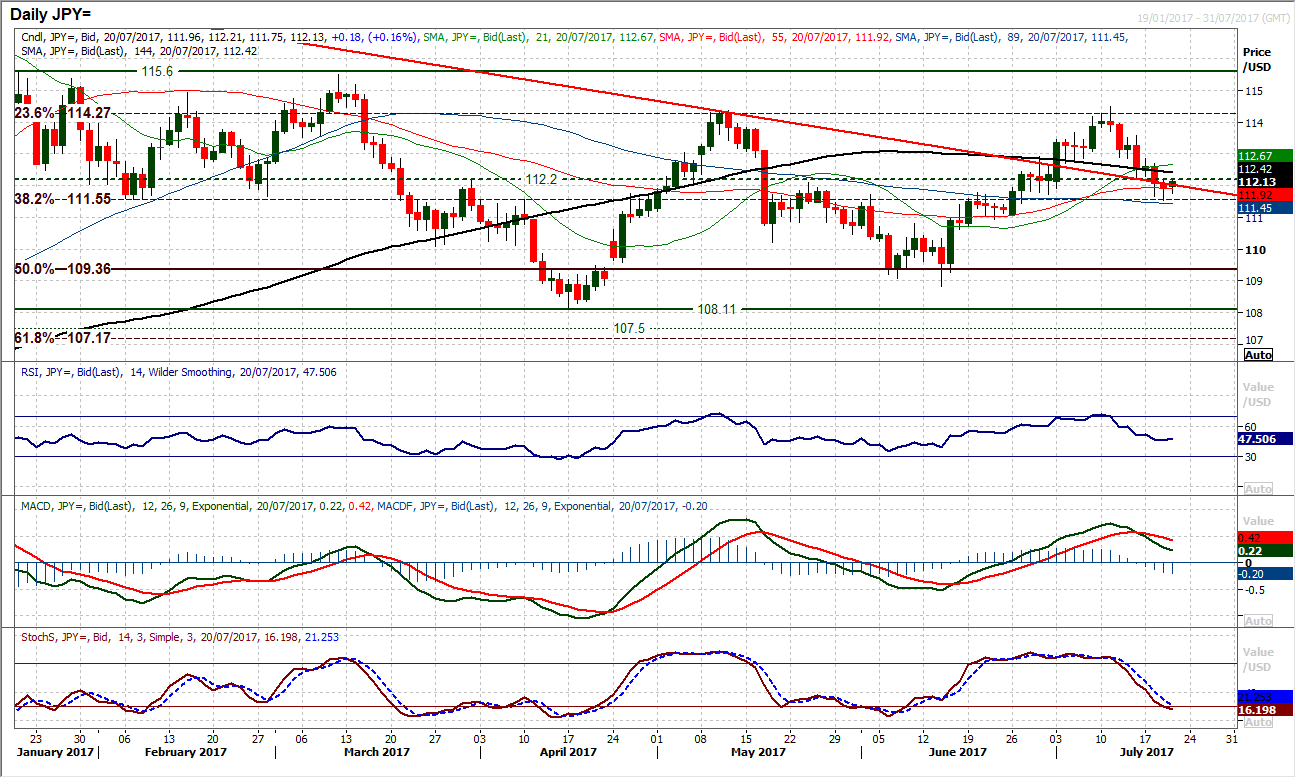

USD/JPY

The nascent selling pressure on Dollar/Yen has just started to slow a touch in the wake of the Bank of Japan monetary policy. The intriguing factor is that the decline once more retreated to find a turning point (or at least consolidation) at the 38.2% Fibonacci retracement of 100.07/118.65 at 111.55. The market has since bounced slightly, but is this the beginning of a recovery? The indicators would suggest the market is in consolidation mode. Not only is the BoJ policy going to impact, but also the ECB and its knock-on impact on the dollar today. The hourly chart simply suggests a consolidation within the downtrend, with the hourly RSI, MACD and Stochastics indicators all back around levels where the bears have resumed control recently. The seven day downtrend has been breached, but there has been no breach of a key lower high yet. The resistance at 112.40 and especially 112.90 remain intact. A closing breach of 111.55 would re-open the downside.

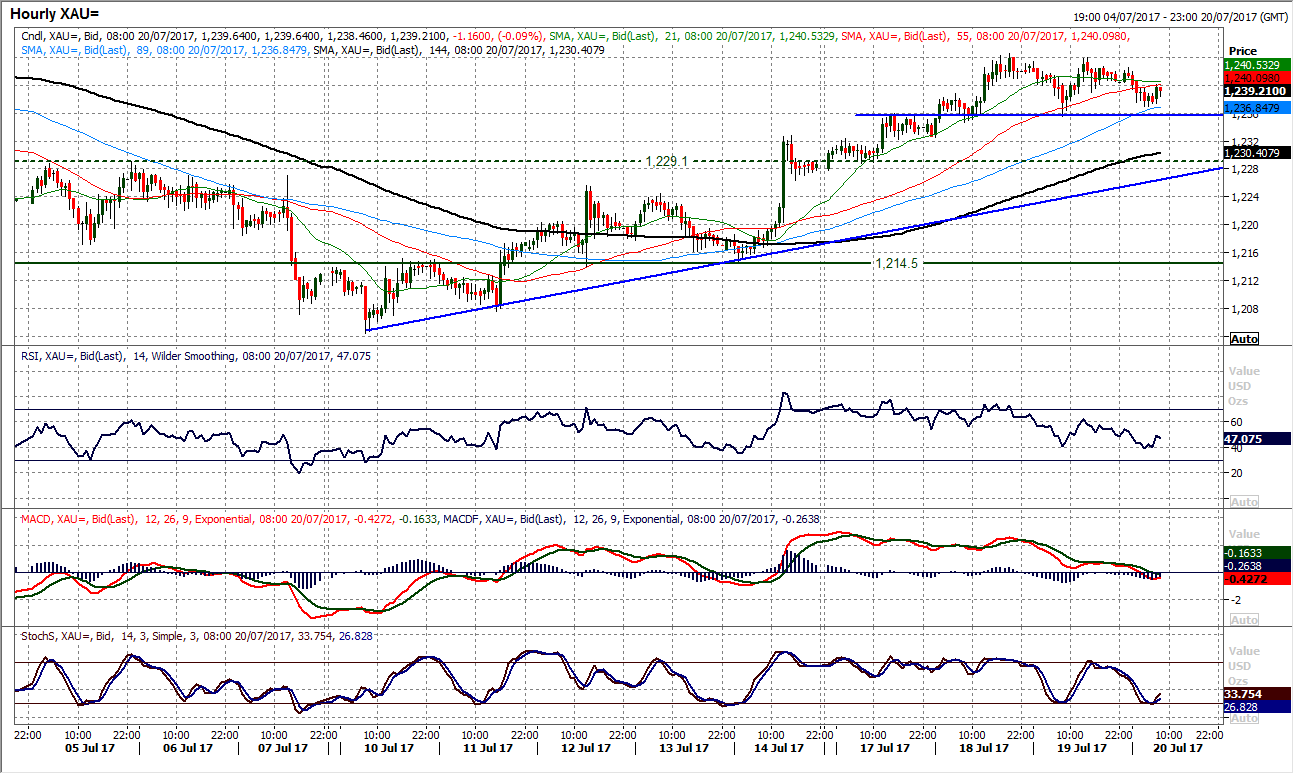

Gold

The impetus in the rally has just been lost again as the run above $1240 has just consolidated. There have been two consecutive closes above $1240 but yesterday’s mild negative candle has been followed by an early slip again. Daily momentum indicators show the importance of the bulls hanging on in there as the RSI has only unwound to 50 and the MACD lines are rising, but still well below neutral. The hourly chart shows that the breakout support around $1235 has become a potential neckline of a small top (of around $9) but the key support remains $1229. Hourly momentum reflects this mild loss of impetus and a more neutral configuration with the hourly RSI failing around 60 and MACD lines back to neutral. The uptrend of the recovery comes in around $1226 today so a correction would not be a disaster for the bulls. However equally, the failure at the resistance of $1244.50 would be a disappointment now.

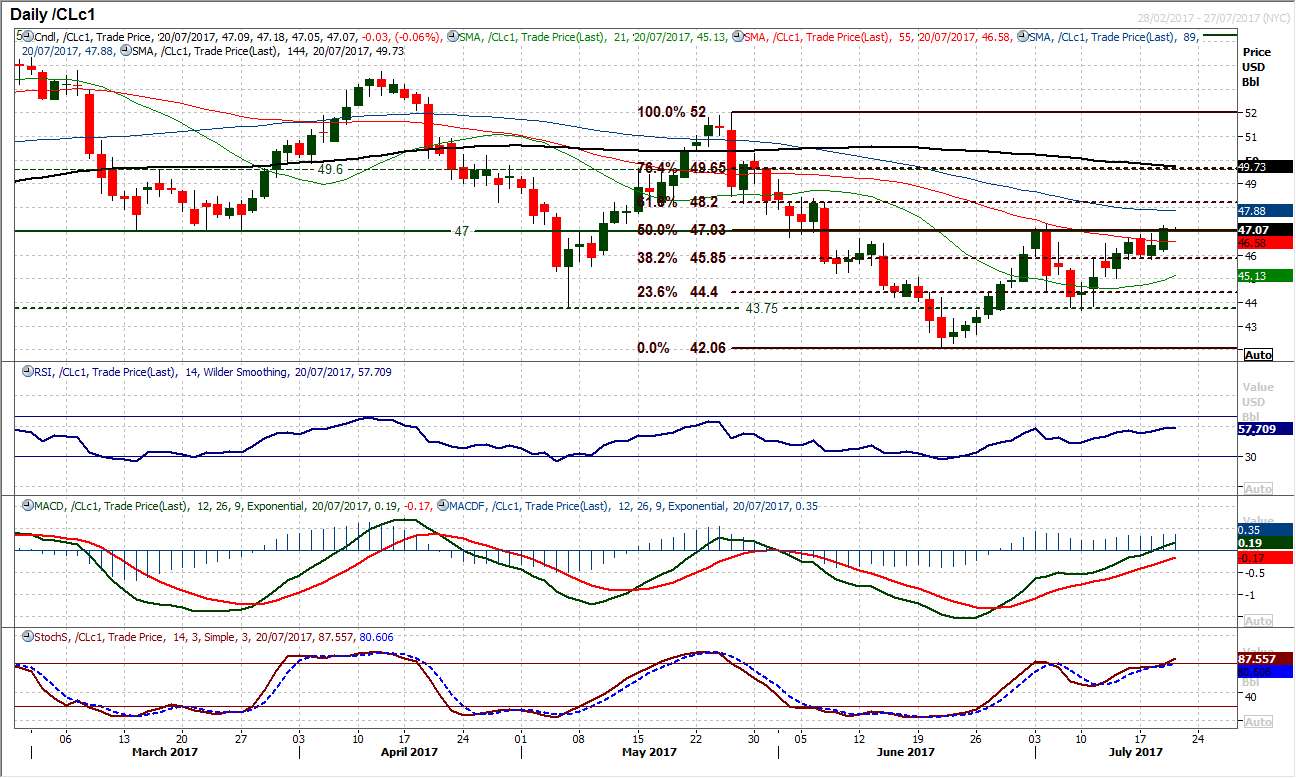

WTI Oil

The bigger than expected drawdowns on crude, distillates and gasoline stocks have helped to push WTI higher through the $47.00 key medium term pivot resistance. This comes with the support of the recent lows at $45.80 bolstered in addition to the 38.2% Fibonacci retracement of $52.00/$42.05 at $45.85. A second positive candle in a row also maintains the continuation of the improving momentum configuration with the RSI pushing higher towards 60, the MACD lines accelerating higher and the Stochastics also strengthening. This positive momentum is also reflected across the hourly time horizon and suggests that corrections are a chance to buy. A second day (and decisive) closing break above $47.00 would open the upside, as for now the market is still holding back a touch. However the bulls are now more confident, with $48.20 as the next Fib retracement.

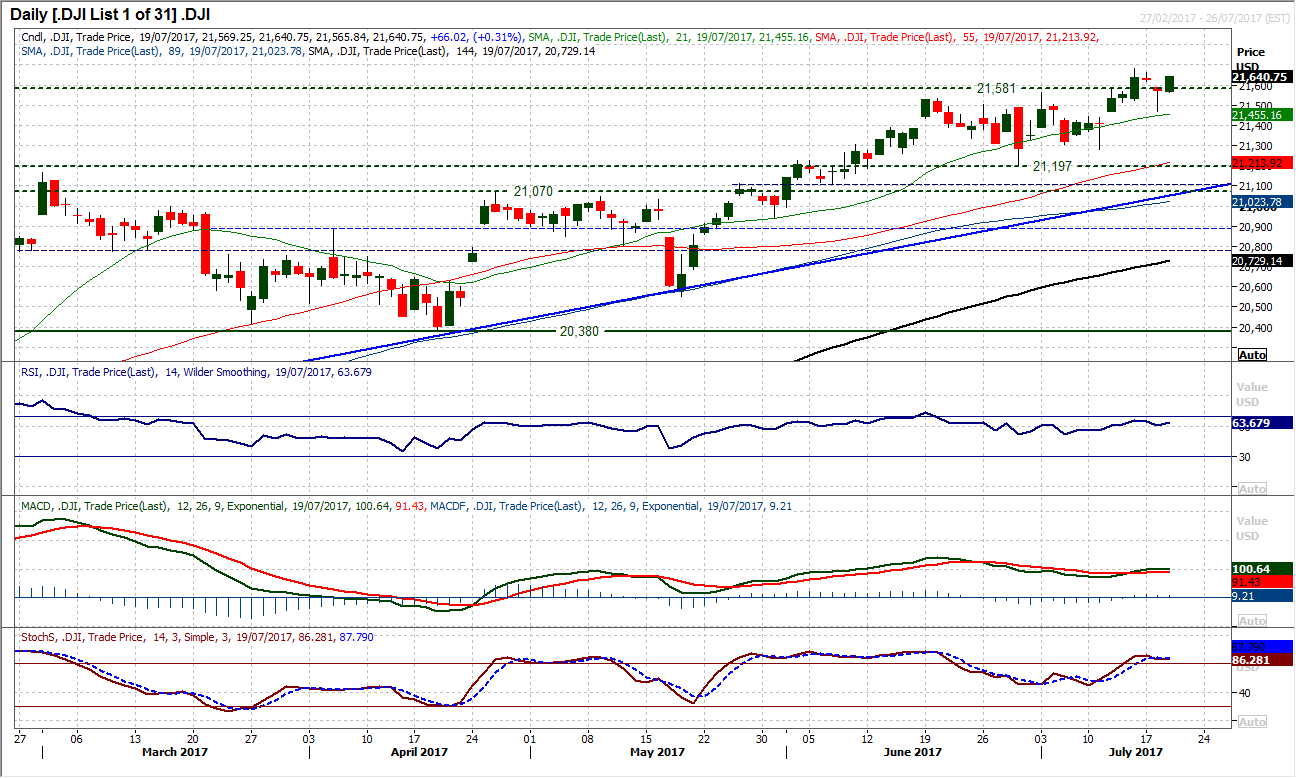

Dow Jones Industrial Average

The appetite for the bulls to still support the Dow into weakness continues as the strong momentum indicators suggest corrections remain a chance to buy. Tuesday’s low of 21,471 takes on an increasingly important level of support, but the bulls, helped by the development of a decent start to US earnings season, are eying all-time highs again. Resistance is therefore at 21,681, whilst the hourly chart shows once more that 35/40 is a strong buying opportunity for the hourly RSI, whilst the MACD lines turning up from neutral has also renewed upside potential.

Author

Richard Perry

Independent Analyst