Forecasting the upcoming week: Central bank rate calls back in the spotlight

Following another print in US NFP jobs data, markets will pivot to face rate calls from several central banks next week and fresh inflation updates from both the US and China.

The US Dollar Index (DXY) spent most of the week on the low end, but made a late recovery on Friday to end the week near the 106.00 handle. Weekly candlestick watchers will note the Dollar Index is churning near the top end of a chopping range that has plagued the Greenback since bottoming out in mid-2023 near the 100.00 key price level, and trend traders could be gearing up for another leg lower. The US data docket starts off quiet next week but then kicks off a dense release schedule in the midweek with Consumer Price Index (CPI) inflation due on Wednesday, followed by Producer Price Index (PPI) inflation and weekly Initial Jobless claims on Thursday.

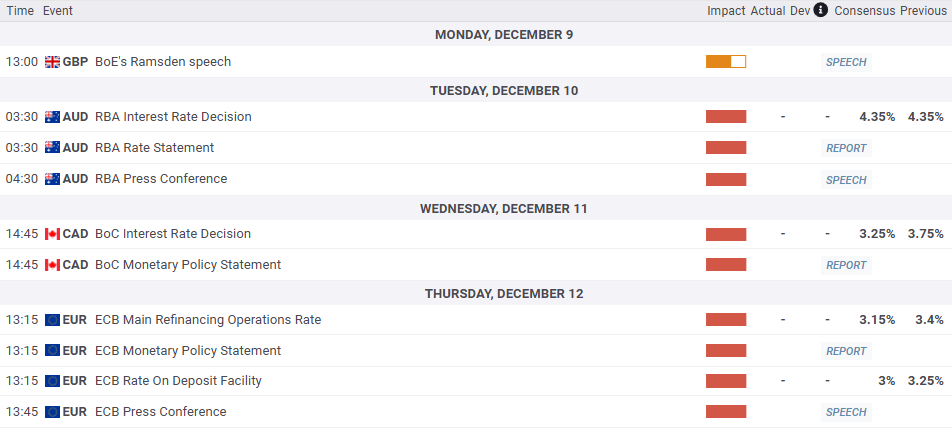

EUR/USD ended the week slightly down in typical mirror-image fashion to the US Dollar Index. Fiber spent much of the week rattling near the 1.0600 handle before turning south on Friday to end the week in the middle of a near-term churning point around 1.0550. EUR traders will be on the lookout next week for the latest rate call from the European Central Bank (ECB) on Thursday, which is widely anticipated to deliver another 25 bps rate trim despite a recent uptick in inflation figures.

GBP/USD ended the trading week close to where it started just north of 1.2700. Cable kicked off the week with a fresh plunge into the low end of the 1.2600 region, battling into a three-week high near 1.2800 before settling lower on Friday and washing the week’s action. UK data is limited on the calendar for next week, leaving Pound Sterling traders to wait for Friday’s mid-tier releases of Industrial and Manufacturing Production output, as well as a monthly update on UK Gross Domestic Product (GDP) growth figures for October.

USD/JPY remains bolted to 150.00, unable to make meaningful headway in either direction. The Dollar-Yen pair halted the previous week’s sharp backslide, but bidding momentum was too thin to pare away recent losses. USD/JPY remains down nearly 4.5% from early November’s peak at 156.75. Japan will kick off the economic data docket early next week with a fresh batch of GDP growth figures for the third quarter. Japan’s Tankan Large Manufacturing Index of business activity expectations for the fourth quarter will print early next Friday.

AUD/USD chalked in another losing week, closing below the 0.6400 handle for the first time in nearly 13 months. The trend remains firmly bearish as the pair continues to backslide from late September’s peaks north of 0.6900. The Reserve Bank of Australia (RBA) will be delivering its latest rate call early Tuesday next week, and markets are broadly anticipating another rate hold from the Australian central bank. Next Thursday brings Australian labor data, where the Unemployment Rate for November is expected to tick up to 4.2% from the previous 4.1%.

USD/CAD closed above 1.4150 for the first time in over four years on Friday, posting the pair’s highest daily close in 55 months as the Loonie continues to roll over against the Greenback. If the pair continues to trend higher through December, USD/CAD will be on pace to close higher on a monthly basis for a fourth consecutive calendar month. Next week, Canadian data remains limited on the economic calendar as always, however the Bank of Canada (BoC) will be delivering its latest rate call on Wednesday, where the Canadian central bank is widely expected to accelerate its rate cutting cycle once again and trim its main reference rate by 50 bps, from 3.75% to 3.25%.

Key events on the radar next week

Estimated central bank appearances and rate calls

Central banks FAQs

Central Banks have a key mandate which is making sure that there is price stability in a country or region. Economies are constantly facing inflation or deflation when prices for certain goods and services are fluctuating. Constant rising prices for the same goods means inflation, constant lowered prices for the same goods means deflation. It is the task of the central bank to keep the demand in line by tweaking its policy rate. For the biggest central banks like the US Federal Reserve (Fed), the European Central Bank (ECB) or the Bank of England (BoE), the mandate is to keep inflation close to 2%.

A central bank has one important tool at its disposal to get inflation higher or lower, and that is by tweaking its benchmark policy rate, commonly known as interest rate. On pre-communicated moments, the central bank will issue a statement with its policy rate and provide additional reasoning on why it is either remaining or changing (cutting or hiking) it. Local banks will adjust their savings and lending rates accordingly, which in turn will make it either harder or easier for people to earn on their savings or for companies to take out loans and make investments in their businesses. When the central bank hikes interest rates substantially, this is called monetary tightening. When it is cutting its benchmark rate, it is called monetary easing.

A central bank is often politically independent. Members of the central bank policy board are passing through a series of panels and hearings before being appointed to a policy board seat. Each member in that board often has a certain conviction on how the central bank should control inflation and the subsequent monetary policy. Members that want a very loose monetary policy, with low rates and cheap lending, to boost the economy substantially while being content to see inflation slightly above 2%, are called ‘doves’. Members that rather want to see higher rates to reward savings and want to keep a lit on inflation at all time are called ‘hawks’ and will not rest until inflation is at or just below 2%.

Normally, there is a chairman or president who leads each meeting, needs to create a consensus between the hawks or doves and has his or her final say when it would come down to a vote split to avoid a 50-50 tie on whether the current policy should be adjusted. The chairman will deliver speeches which often can be followed live, where the current monetary stance and outlook is being communicated. A central bank will try to push forward its monetary policy without triggering violent swings in rates, equities, or its currency. All members of the central bank will channel their stance toward the markets in advance of a policy meeting event. A few days before a policy meeting takes place until the new policy has been communicated, members are forbidden to talk publicly. This is called the blackout period.

Author

Joshua Gibson

FXStreet

Joshua joins the FXStreet team as an Economics and Finance double major from Vancouver Island University with twelve years' experience as an independent trader focusing on technical analysis.