FOMC preview: What to expect and how will it impact the US Dollar?

-

The FOMC meeting today is highly anticipated due to uncertainty surrounding future US monetary policy.

-

Markets expect a 25 bps rate cut today and a slower pace of easing in 2025 due to President-elect Trump's policies.

-

The Fed's reverse repo rate may be adjusted, potentially impacting the US Dollar's strength.

The FOMC meeting today is key as interest rate meetings tend to be from the US. However, today's meeting is even more intriguing given all the noise and uncertainty moving forward.

The Fed is shifting its policies from being very restrictive to more balanced. Recent data has shown some stickiness in inflation and with President-elect Trump aiming to boost US economic growth, the Fed is likely to take a careful and slow approach to easing policies in 2025. This for now is where the focus will lie.

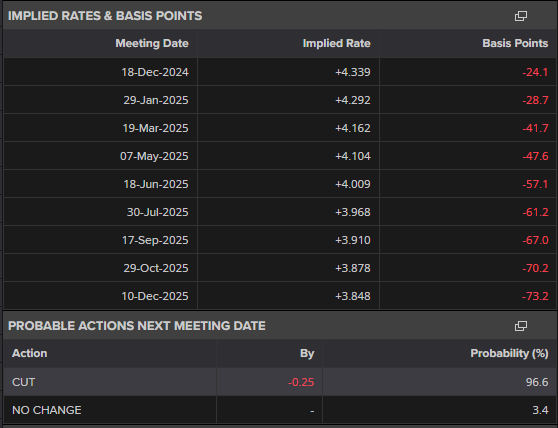

Heading into the meeting, markets are expecting around 73 bps of rate cuts through December 2025. This would include the proposed 25 bps cut today, meaning just 50 bps cuts in 2025.

Source: LSEG (click to enlarge)

What to expect from the FOMC Meeting?

The main driver of late when it comes to US monetary policy decisions has been the US Labor market. The labor market is slowing down, with fewer new jobs, a drop in full-time employment, and a small rise in unemployment. These changes give the Fed a reason to move toward a more balanced policy approach.

Inflation which had been the main focus for the first 6-8 months of the year did take a backseat over the past few months. However recent data suggests that this may rear its ugly head once more in 2025.

Focus heading into the meeting will focus on updates to the Feds economic projections. In particular, the number of rate cuts we may expect in 2025. The consensus heading into the meeting is that President-elect Trump's plans for stricter immigration controls, new tariffs, and cutting taxes for individuals and businesses are expected to lead the Fed to take a more cautious and slower approach to easing policies in 2025.

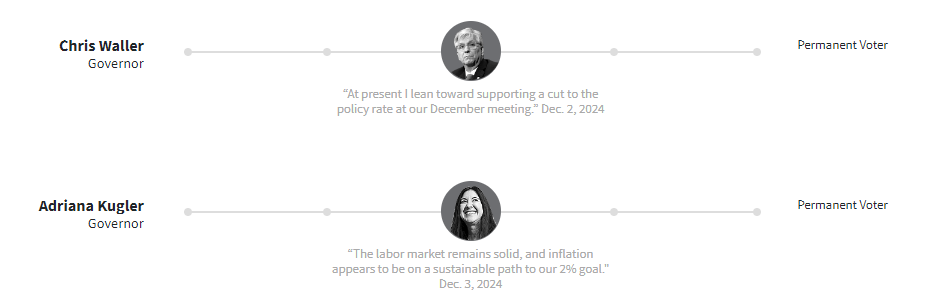

I do think that this is on point however, the rhetoric of the Fed will be important. Heading into the meeting we have heard a host of comments from Fed Policymakers who have supported more gradual easing in 2025.

Fed policymaker comments in the lead up to December 18 meeting

Source: LSEG (click to enlarge)

The comments from policymakers definitely show a willingness for a slower rate cut path moving forward. In theory this should lead to some US Dollar strength as well as a rise in US Yields.

Having said that, I do expect a pause in January as the meeting will arrive just 9 or so days after President Elect Trump takes office. The March meeting should provide some time to gauge the effects of proposed Trump policy and might give markets a clearer picture for 2025.

Feds Reverse repo rate

The minutes from the last FOMC meeting made reference to a possible technical adjustment to the Fed’s reverse repo rate and this may be something to watch as well. The proposal is to lower the reverse repo rate by 5 basis points (bp), bringing it down to match the floor at 4.25%. At the same time, the Fed would also lower its whole interest rate range by 25 bp.

This means the new floor would drop to 4.25%, the ceiling would fall to 4.5%, and the reverse repo rate would shift to align with the new floor.

The other important rate, the interest on reserves (which is what the Fed pays banks for holding their extra money), would also go down by 25 bp, staying 15 bp above the floor as it is now.

One big takeaway here is that lowering the reverse repo rate would make the facility less appealing for banks to use. Eventually, as banks reduce their use of this facility, their reserves (money they hold at the Fed) could shrink.

Is such a move a positive or negative for the US Dollar?

In theory, if the reverse repo rate is lowered, as the Fed is considering, it reduces the interest banks and financial institutions earn when parking their cash with the Fed. This could make US interest rates slightly less attractive. With lower interest returns, some foreign investors might look for better opportunities in other countries with higher rates. If this happens, it could put mild downward pressure on the US Dollar's strength.Something else to consider heading into the meeting, could such a move cancel out any US Dollar strength that may be gained should the Fed point to a slower rate cut path in 2025? Time will tell.

US Dollar Index

From a technical standpoint, the dollar is at crossroads as it is back around the multi-month key level at 107.00.

I do expect the US Dollar to maintain its dominance heading into 2025 especially if the Fed meet markets expectations regarding slower cuts in 2025.

This should keep the rate differential in play which has benefited the US Dollar since October.

As the Dollar has defied its seasonal trend by strengthening thus far in December, it would take a surprise later in the day to change the narrative. I do expect this narrative to persist until President trump takes office and begins enacting his policies.

US Dollar Index (DXY) daily chart, December 18, 2024

Source: TradingView.com (click to enlarge)

Support

- 106.50

- 106.00

- 105.63

Resistance

- 107.50

- 108.00

- 109.00

Author

Zain Vawda

MarketPulse

Zain is a seasoned financial markets analyst and educator with expertise in retail forex, economics, and market analysis.