FOMC Minutes June 18-19 Meeting Preview: July and beyond

- Fed Funds maintained at 2.25%-2.50% by 8-1

- James Bullard of the St. Louis Fed voted to cut 0.25%

- Hints to future policy in the minutes paramount

The Federal Reserve will release the edited minutes of the June 18-19 Federal Open Market Committee (FOMC) meeting on Wednesday July 10 at 2:00 pm EDT, 18:00 GMT

FOMC Policy

The June FOMC statement dropped the description of Fed rate policy as patient that had first appeared in January after the December fed funds 0.25% increase and remained until May. That excision combined with Chairman’s Powell’s comment that the bank could reduce rates if it thought necessary convinced the markets that the FOMC would cut by at least a quarter point at the next, July 31 meeting.

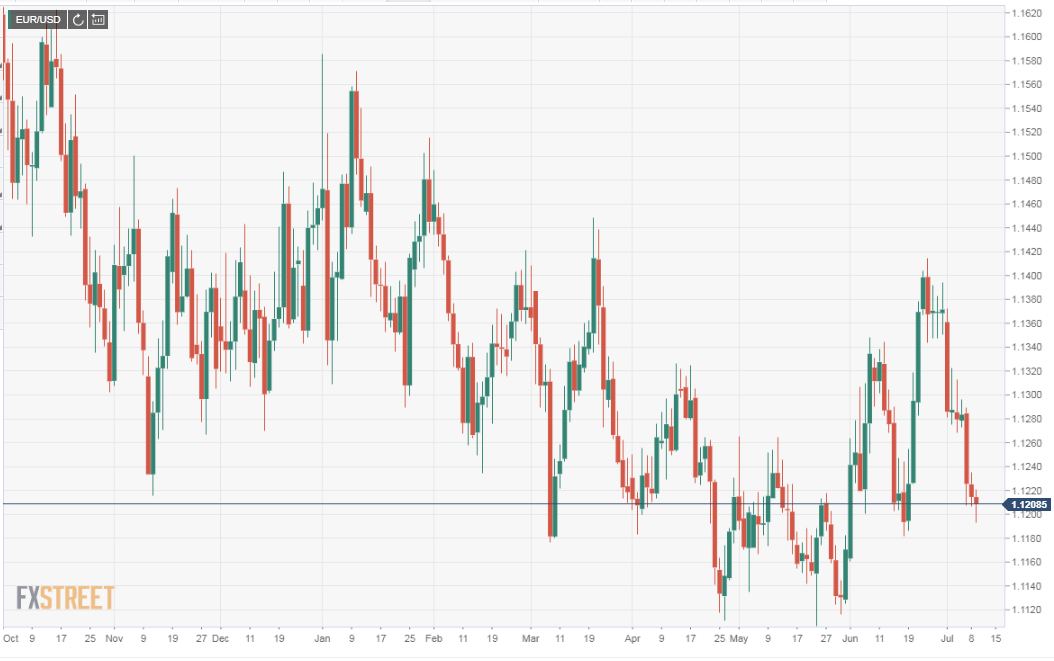

Nothing has changed in the market anticipation of a rate reduction. Equities have set and retreated from records highs. The dollar gain over the past two week, almost 2% against the euro, has been largely due to ECB comments that it too could cut rates.

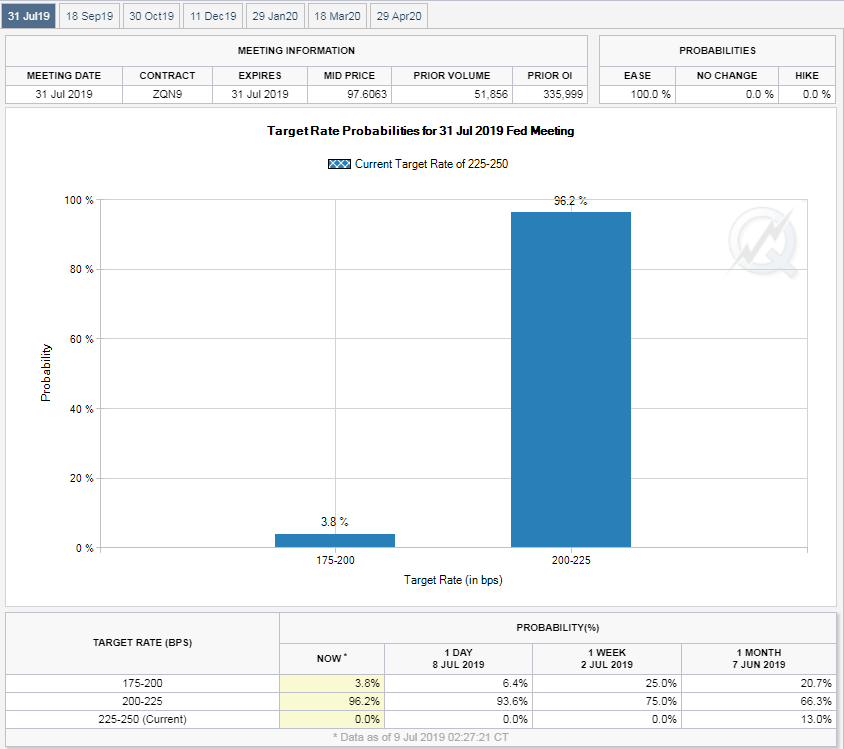

Fed funds futures are almost unanimous in conviction that the governors will elect a rate cut with a 96.2% chance of a 25 basis point reduction and 3.8% for a 50 point decrease.

CME Group

The June non-farm payrolls added 224,000 workers, far more than the 160,000 forecast and the unemployment rate of 3.7% was a five decade low.

This unexpected labor strength helped to mitigate concerns that two recent NFP reports below 100,000, February and May, combined with ADP’s 27,000 May and 102,000 June payrolls indicated that job creation was slowing in line with weakening GDP.

The economy expanded at a 3.1% annual rate in the first quarter but the Atlanta Fed GDPNow current forecast for the second quarter is just 1.3% and has been below 2% for most of the past two months.

Before the July 5th NFP report the futures had listed a 74.5% chance of a 0.25% cut at month end and a 25.6% change of a 0.5% decrease. The NFP result and the change in the futures helped boost the dollar.

FOMC Minutes and Policy

The Fed’s June policy shift is not primarily based on US economic performance, though the 56,000 February and 72,000 May payrolls elicited concern.

While the three month moving average for payrolls of 171,000 in June was considerably less than the 245,000 average in January it does not appear to be the result of a general slowing of hiring but of the unusual juxtaposition of two weak months. One month below trend is a common occurrence but not two.

-636982981545718077.PNG)

Reuters

Other labor market indicators, initial jobless claims, annual wages and the unemployment rate remain healthy.

Fed governors were and we may presume are still worried about the impact of slowing global economic growth on the US economy and the drag on both from the US-China trade and tariff dispute. The IMF has reduced its global growth estimate from 3.7% last year to 3.5% in January and 3.3% in April which would be the weakest since 2009.

The market confidence that the Fed will take out that 0.25% insurance policy on the 31st is warranted. It would be uncharacteristic for the governors to have set up the rate cut and then with it fully priced in all markets change their minds.

It is the evolution of Fed policy after the July meeting that is the unsolved question. The June fed funds rate projection at year end of 2.4% would be satisfied by a cut on the 31st as would the central tendency of 1.9% -2.4%.

It is unlikely that the governors have any secure conviction for the direction of the US economy in the second half, too much, particularly China being unsettled. But any clue as to their thinking will be eagerly seized by markets looking for a post-summer direction.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.