FOMC Minutes and RBA decision next week

As the week draws to a close we open a window at what next week has in store for the markets. On Monday we note the release of the UK’s Halifax house prices rate for June, Sweden’s preliminary CPI rate for June and the Eurozone’s sentix index figure for July. On Tuesday we note the RBA’s interest rate decision and Canada’s Ivey PMI figure for June. On Wednesday, we note China’s PPI and CPI rates for June and the RBNZ’s interest rate decision. On Thursday we note Japan’s corporate goods price rate for June, Sweden’s GDP rate for May, Norway’s Core CPI rate for June, the Czech Republic’s final CPI rate for June and the US weekly initial jobless claims figure. On Friday we note Germany’s final HICP rate for June, the UK’s GDP rates for May and manufacturing output rate for May, France’s final HICP rate for June and lastly Canada’s employment data also for the month of June. Lastly on a monetary level we would like to note the release of the FOMC’s last meeting minutes on Wednesday.

USD – FOMC minutes due out

On a monetary level, we note that the Fed’s last meeting minutes are due out next Wednesday. The FOMC’s minutes may showcase greater insight into the Fed’s deliberations and what considerations they took when deciding on their decision to keep interest rates steady. As such, should the minutes showcase that the bank may be preparing to cut rates in the near future it may be perceived as dovish. However, should the bank’s meeting minutes showcase a willingness from policymakers to remain on hold for a prolonged period of time, it may be perceived as hawkish which could in turn aid the dollar.

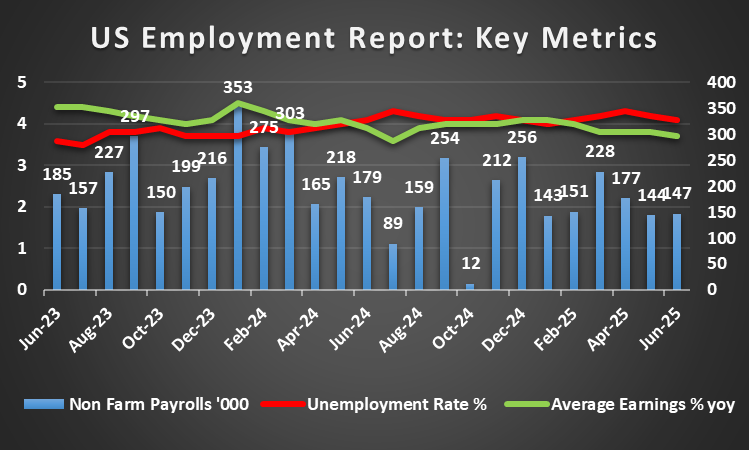

On a macroeconomic level, we note a light economic calendar for the US in the upcoming week and thus the dollar may cede some of its control. However the US Employment data was released yesterday and surprised market participants as it showcased a reduction in the unemployment rate whereas economists had expected an uptick. Overall the employment data tended to provide support for the dollar following its release.

On a fundamental level, we highlight and stress that the tariff deadline is next week on the 9th of July, where the tariff reprieve is set to expire. Thus, with trade deals still being discussed, it may lead to heightened volatility in the markets as some uncertainty still persists.

“The Fed’s minutes will be interesting considering Powell’s dovish comments this week. In turn, we would not be surprised to see a more dovish rhetoric emerging from Fed policymakers in the meeting minutes. Moreover, we wouldn’t be surprised to see some nations failing to reach an agreement with the US prior to the 9th of July tariff deadline, which could increase volatility in the US equity markets.”

GBP – GDP rates in sight

We make a start by noting on a monetary level that BoE member Alan Taylor stated on Bloomberg this Wednesday, that he is “starting to see cracks” in the labour market and that a soft landing is at “risk”. Moreover, the policymaker stated this week that in his view “we needed to be on a lower rate path, needing five cuts in 2025 rather than the market-implied quarterly pace of four”. The policymakers comments are dovish in nature and thus may have weighed on the pound.

On a macroeconomic level, we note that the UK’s GDP rates for May are set to be released next Friday. The GDP rates may increase interest in the sterling especially considering the comments made by BoE Taylor which we referenced above. Overall, should the GDP rates showcase an expansion of the UK economy it may aid the pound and vice versa.

On a fundamental level, we note the recent political drama in the UK, which saw UK government bonds rallying after PM Starmer reassured the markets that Reeves would remain on as Chancellor of the Exchequer after the PM failed to give the chancellor his full backing after being asked about her future. Nonetheless the issue appears to have been resolved as of today.

“The UK’s GDP rates are one to watch for next week for obvious reasons. We are also interested as to whether other policymakers will echo the remarks of BoE Taylor in the coming week. Should they decide to do so it could weigh on the pound.”

JPY – BOJ to resume its rate hiking path?

On a monetary level, we note BOJ Governor Ueda’s comments earlier on this week where he stated that underlying inflation was still “somewhat below” the bank’s 2% inflation target. Moreover, BOJ member Takata who spoke earlier on today stated that “I believe that the bank is currently only pausing its policy interest rate hike cycle and should continue to make a gear shift after a certain · period of ‘wait and see” which may imply that the bank could be preparing to continue on it’s rate hiking cycle which in turn could possibly aid the JPY.

On a macroeconomic level, we note no major financial releases for Yen traders in the upcoming week hence we expect fundamentals to lead the JPY

On a fundamental level we note that President Trump noted earlier on this week that a trade deal with Japan before the 9th of July deadline may not occur and thus should they fail to reach a trade agreement prior to the deadline next week, it could weigh on the Japanese Equities markets.

“We expect to see volatility in the Japanese Equities markets in the coming week as a trade deal between the US and Japan currently seems unlikely to be reached prior to the deadline. Furthermore, we would like to see comments from BOJ policymakers as to whether the majority appear inclined to resume the banks rate hiking path”

EUR – Zone’s Sentix index

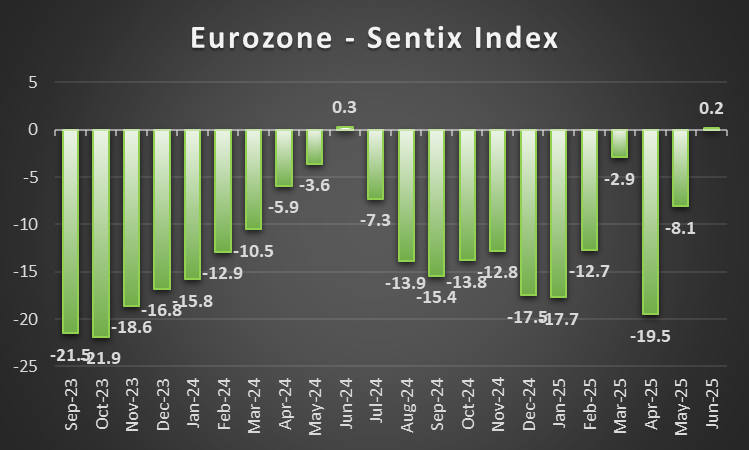

On a macro level we note that Germany’s preliminary HICP rates for June came in lower than expected at 2% on a year on year level versus 2.2% and 0.1% versus 0.3% on a month-on-month basis. In turn the lower than expected inflation print tends to showcase easing inflationary pressures in one of the largest economies in the Eurozone. Thus the lower than expected inflation print for Germany may have weighed on the common currency during the week. For next week, interest surrounding the Eurozone’s Sentix index may increase, where an improvement in the figure may see the EUR potentially moving higher and vice versa.

On a monetary level, we note the comments made by ECB President Lagarde earlier on this week, who stated that ““structural shifts” make the world more volatile and that it respond to “large, sustained deviations of inflation from target in either direction” with a forceful response. In turn the comments made by the ECB President may be perceived as slightly hawkish in nature which may have aided the EUR.

On a fundamental level we note that Trump’s July 9th deadline is quickly approaching and with no time to spare some media outlets have been reporting that the EU is close on agreeing to a framework for a trade deal with the US which would avert a 50% tariff on all exports starting next week. In turn, the recent media announcements could potentially aid the European Equities markets.

“We are concerned that the EU and the US are still attempting to hammer out a trade deal before the July 9th deadline. In our view a full trade deal may be unlikely to occur prior to the deadline and thus the best alternative may be a working framework which could push back the imposition of the 50% tariff on European goods. Otherwise, we may see heavy volatility in the European Equities markets.”

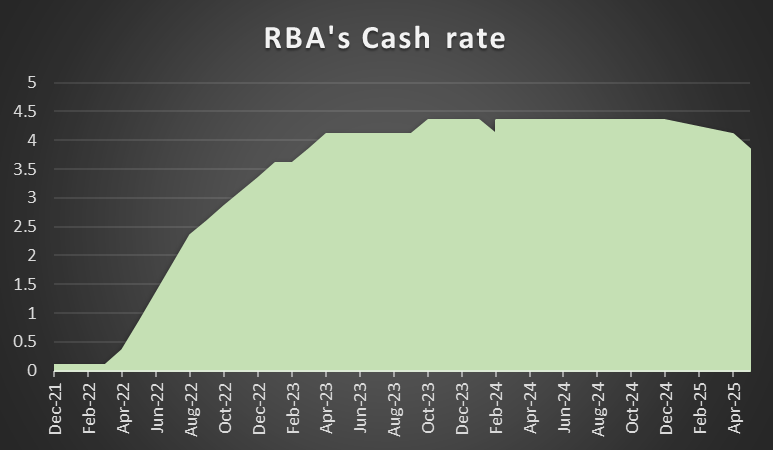

AUD – RBA decision next week

On a macro level, we note the release of Australia’s Judo Bank manufacturing PMI figure for June this Tuesday. The figure came in lower than expected at 50.6 versus 51.0 which may have weighed on the Aussie. Yet when looking at the figure, it still remains in expansion territory and thus is still a positive in the grander scheme of things. However, of some concern was Australia’s trade data for May which was released on Thursday which showcased a deterioration in the nation’s trade surplus which may have weighed on the AUD.

On a monetary level, we note the market’s expectations for RBA to deliver three more rate cuts by the end of the year. Hence the RBA’s interest rate decision next week is sure to garner significant attention from Aussie traders. In particular, the majority of market participants are currently anticipating the bank to cut rates in their meeting next with, with AUD OIS currently implying an 84.6% probability for such a scenario to materialize. In turn should the bank’s accompanying statement be perceived as dovish in nature, i.e implying that they may continue cutting rates down the road as is currently expected it could weigh on the Aussie. On the other hand, should they imply that they may deviate from such a path, it may be perceived as hawkish in nature which could aid the AUD.

On a fundamental level, we highlight China’s NBS manufacturing PMI figure for June which was released earlier on this week and came in higher than expected. Therefore considering the close economic ties between China and Australia an improvement in China’s manufacturing sector may imply an increase in demand for raw materials from Australia and could thus aid the Aussie should China’s economic situation continue to improve.

“The RBA’s decision will be an interesting event next week. Given the markets expectations of 3 rate cuts by the end of the year which include next week’s decision, any deviation from such a path could lead to heightened volatility in the Aussie. Moreover, policymakers may be concerned with the ongoing trade negotiations that China has engaged in with the US and the EU and their possible impacts.”

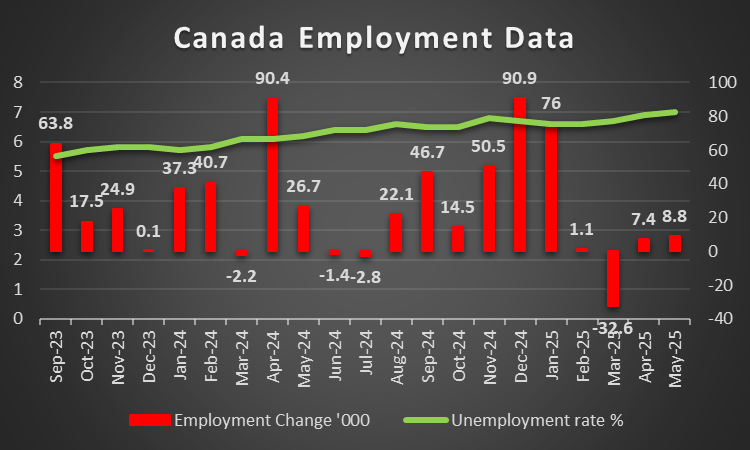

CAD – Employment data due out next week

On a macroeconomic level, we had a rather easy going week for Loonie traders, once again. However, interest may pick up next week with the release of Canada’s employment data for June on Friday. Should the Canadian employment data showcase a resilient labour market, it could potentially aid the Loonie. Whereas should the data showcase a loosening labour market it may have the opposite effect.

Furthermore we would also like to note the release of Canada’s Ivey PMI figure for June on Tuesday. Should the figure showcase an improvement from its prior figure of 53.8 it could potentially aid the Canadian dollar. Whereas should the figure showcase a deterioriation it could have the opposite effect and thus could weigh on the Loonie.

On a fundamental level, some reports have emerged that OPEC may be moving their meeting to July 5th which is tomorrow. Therefore given Canada’s status as an oil exporting nation any changes to oil prices could also influence the Loonie in the coming week.

“We expect Loonie to possibly experience volatility next week given the nation’s employment data , Ivey PMI and the OPEC meeting which is allegedly set to take place tomorrow.”

General Comment

As a closing comment we note that the risk which may arise from Trump’s July 9th tariff deadline may lead to heightened volatility in the US Equities markets. Moreover, with Trump’s “One Big Beautifull Bill” having passed both the Senate and the House, economists may be looking to gauge its full impact on the US economy. In turn should concerns over the state of the US economy arise it may aid gold prices as well.

Author

Phaedros Pantelides

IronFX

Mr Pantelides has graduated from the University of Reading with a degree in BSc Business Economics, where he discovered his passion for trading and analyzing global geopolitics.