Five Fundamentals for the week: Fed overtowers pivotal week for Gold, stocks and the US Dollar

- The Fed's first rate cut stands out as economic uncertainty mounts.

- US Retail Sales and Jobless Claims are of high interest.

- Rate decisions by central banks in the UK and Japan are also pivotal.

Normal or double? That is the dilemma for the Federal Reserve (Fed), which is set to kick off its rate-reduction cycle this week. The dilemma between a 25 and 50 basis points (bps) cut is only one of the components for the world's most powerful central bank, which will decide about rates alongside two main peers. Here are the main events of the week.

1) US Retail Sales to provide last hint before the Fed

Tuesday, 12:30 GMT. With uncertainty ahead of the Fed decision, this critical report on the health of the US consumer will help shape expectations. After a jump of 1% in July, headline retail sales are expected to have risen by 0.2% in August. That would reflect a moderation in consumer spending, pointing to a soft landing for the US economy.

A small drop in Retail Sales would be welcome as it would raise the chances of a 50 bps cut, but a big drop would already worry markets of a looming recession. A surprising second consecutive leap would be good for the economy but bad for stocks, as the possibility of a 50 bps cut would fade away.

For the US Dollar, the stronger the better, while Gold would benefit from a weak figure.

2) Fed decision uncertainty is extraordinarily high

Wednesday, decision and forecasts are at 18:00 GMT, and the press conference is at 18:30 GMT.

This Federal Reserve (Fed) decision stands out for two reasons. First, the world's most important central bank is set to cut interest rates for the first time in more than four years. Secondly, there is uncertainty about the size of the cut. The Fed likes to convey its moves in advance, and this time is different.

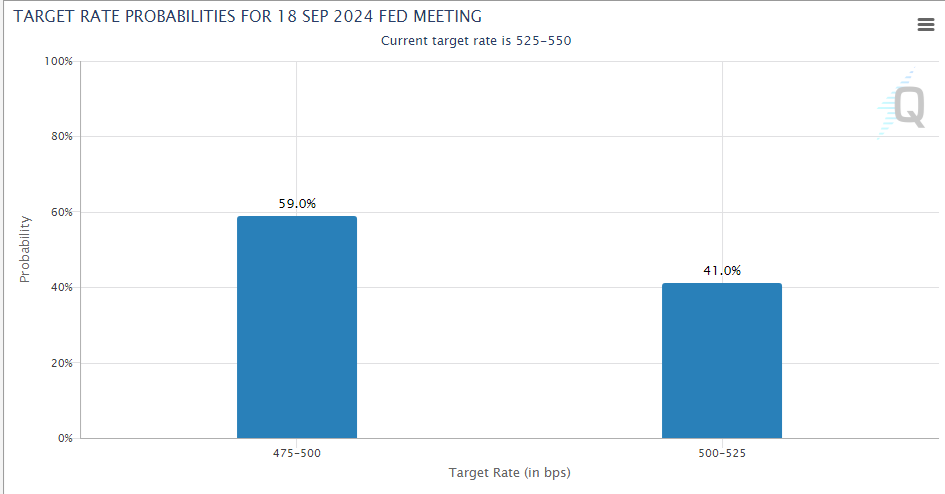

With roughly a 50-50 chance of either a standard 25 bps cut or a large 50 bps reduction, the decision is the No. 1 market mover. Basically, stocks and Gold will jump up on a 50 bps cut, while the US Dollar would benefit from a 25 bps slash.

Fed pricing. Source: CME Group.

The Fed's forecasts – also known as the “dot plot" – will have the second word. I expect the Fed to balance any decision. A 25 bps cut would probably be accompanied by an outlook for more aggressive cutting down the line, while a 50-bps cut would be followed by caution about the next moves.

In such "hawkish big cut" or a "dovish small cut" scenarios, the reaction would be whipsaw – investors jumping to one side before more than reversing the initial move.

In case a 50 bps cut comes with promises to cut rates fast, fears of a recession would come in, weighing on market sentiment. Similarly, a hawkish stance on top of a 25 bps cut would disappoint investors wishing to see lower rates. I think a balanced outcome is more likely.

The accompanying statement will also try to find a balance.

Then comes Fed Chair Jerome Powell and his press conference. He will be asked if he still believes a soft landing is on the cards. Investors need a confident "yes" for reassurance. Dodging the question or expressing fears of a recession would weigh on sentiment.

It is essential to note that the Fed decision consists of several phases in its responses, meaning volatility could be high for long days.

3) BoE may hold rates, voting pattern matters

Thursday, 11:00 GMT. The Bank of England (BoE) is widely expected to leave interest rates unchanged after August's cut. While headline inflation has dropped, core prices have not been crushed just yet.

UK core PCE. Source: FXStreet

While economic growth stalled in July, the UK labor market lifted its head, reducing the need for any instant stimulus for the economy.

Moreover, the Monetary Policy Committee (MPC) voted to cut rates by the slimmest of majorities in August – five in favor, four against. That was a "hawkish cut," which implied a high probability of a pause this time.

Assuming a no-change decision, the focus is on the voting pattern. The economic calendar points to an expected 7:2 split in favor of keeping rates stable. A surprisingly wider majority would lift the Pound Sterling (GBP), while a narrower one would weaken it.

It is essential to note that the decision comes one day after the Fed decision, and the reaction in GBP/USD will also reflect a comparison of both decisions.

4) US jobless claims to trigger high volatility

Thursday, 12:30 GMT. Regardless of what the Fed decides, Chair Jerome Powell will insist that the Fed is data-dependent and will surely repeat his stance from August about focusing on the labor market.

That puts the focus on every jobs-related data point. While weekly Unemployment Claims figures can suffer from noise, they can serve as the "canary in the coalmine" for a potential quick deterioration in hiring.

A figure of around 230,000, as seen in recent weeks, is on the cards. Any jump above 240,000 would scare investors, while a drop under 200,000 would be encouraging.

5) BoJ to give a nod to Yen strength

Friday, early in the day. The Bank of Japan (BoJ) is the only central bank in the developed world that is still fighting inflation. For years, officials in Tokyo battled deflation, implementing a long spell of negative rates. They are now catching up with the rest of the world.

The BoJ's rate hike earlier this year – even if only to 0% – and its hawkish rhetoric have boosted the Japanese Yen (JPY). The currency also received occasional support from the Ministry of Finance (MoF), which has intervened to boost its value.

BoJ Governor Kazuo Ueda and his colleagues are set to leave rates unchanged, and may reiterate their willingness to raise rates further ahead. They would benefit from the stronger Yen, which lowers import prices – especially energy.

If the Fed is dovish and the BoJ is hawkish, it could turn into another spectacular fall for USD/JPY – dragging other Yen crosses down along its side.

Last word

This is an explosive week. Please trade with care, especially around the Fed decision.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.