Five Fundamentals for the week: Fed leads central bank parade as uncertainty remains extreme

- US Retail Sales kick off the week at full force, providing hard data about the impact of Trump's policies.

- The Fed's dot plot is critical to the next moves in markets.

- Central banks in Japan, Switzerland and the UK add to the volatile mix.

Central bank bonanza – perhaps its is not as exciting as comments from the White House, but central banks still have sway. They have a chance to share insights about the impact of tariffs, especially when they come from the world's most powerful central bank, the Federal Reserve (Fed).

1) US Retail Sales provide hard data of consumption dip (or lack thereof)

Monday, 12:30 GMT. Do consumer surveys reflect reality? In theory, polls of consumers provide an early indication of their shopping intentions and give investors a heads-up on how the broader economy is doing. In practice, the correlation between what people say and what they do is often non-existent.

This time could be different. US President Donald Trump's tariff and government-cutting policies have caused substantial dips in confidence, and it may also affect their consumption. Another related question is the timing. If consumption is indeed adversely impacted by Trump's tariffs, will the dip be seen in February's data?

The economic calendar points to an increase of 0.7% in headline sales after a dive of 0.9% in January. Any miss would cause worries, while a beat would cause some temporary calm.

Another figure to watch is the Retail Sales Control Group, which is the "core of the core." It dropped by a whopping 0.8% in January and will likely bounce, yet the scale is unknown.

2) BoJ expected to signal rate hikes after unions negotiated pay rises

Wednesday, early in Asia, press conference due at 6:30 GMT. The Bank of Japan (BoJ) has been going against the global trend of slashing borrowing costs, and for good reasons: borrowing costs are low, at 0.50%, and inflation is on the rise, not falling.

Moreover, Japan's labor market is highly unionized, and recent collective bargaining agreements point to substantial wage rises ahead of the new fiscal year, which begins in April. That implies an increase in core inflation, which the BoJ can tamper with via higher interest rates.

While the BoJ is projected to refrain from any moves at this juncture, Governor Kazuo Ueda will likely signal rate hikes ahead, boosting the Japanese Yen (JPY) and maintaining the downward trajectory of JPY crosses.

3) Fed's Powell stuck between a rock and a hard place

Wednesday, decision at 18:00 GMT, press conference at 18:30 GMT. Do tariffs mean higher prices and a need for elevated interest rates? Or will they cause a downturn that requires the world's most powerful central bank to cut borrowing costs? That is the dilemma for Fed Chair Jerome Powell and his colleagues, who make their decisions and projections on the backdrop of extreme uncertainty.

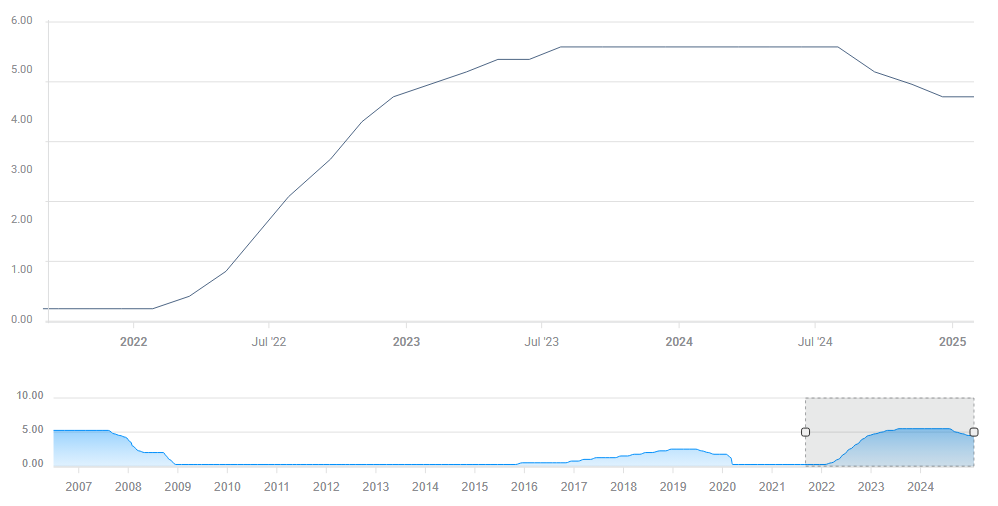

Federal Funds Rate. Source: FXStreet

The Fed is set to leave interest rates unchanged at the 4.25%-4.50% range, but their forecasts for future moves will be closely watched. The central bank last released its projections – aka "dot plot" – back in December, and the message was hawkish: only two rate cuts in 2025, half of the previous projection.

Since then, President Donald Trump has assumed his role and imposed a garden variety of tariffs: from global 25% levies on steel and aluminum, 20% duties on Chinese imports and erratic policy on Canada and Mexico. The biggest unknown is what happens on April 2, when the White House plans major "reciprocal tariffs."

Another source of uncertainty is the Department of Governor Efficiency (DOGE) and its firings. Will that lift unemployment? The Fed has two mandates: full employment and price stability. Any increase in joblessness would require lower rates.

I expect Powell and his colleagues to lean toward three interest rate cuts in 2025, marginally aligning with markets and leaving more room to operate if circumstances change. A small shift toward the dovish side would convey a message of confidence, while a bigger one would scare markets and solely focusing on inflation risks would cause investors to fear higher rates.

Stocks need this middle-ground "Goldilocks" scenario to thrive, the US Dollar (USD) needs a hawkish outcome, while Gold would benefit from a strong dovish message.

4) SNB set to further cut rates, putting indirect pressure on the Euro.

Thursday, 8:30 GMT. The Swiss National Bank (SNB) announces its decisions only once per quarter, making every event more meaningful. A mix of a slowdown in Switzerland and the surrounding Eurozone, alongside a relatively strong Swiss Franc (CHF), kept inflation down in the alpine country, allowing the SNB to slash borrowing costs again.

By reducing borrowing costs to 0.25% from 0.50%, interest rates in Switzerland would fall below those of Japan – and to the lowest in the developed world. That means the CHF could come under constant pressure. On the other hand, an SNB rate cut implies further such moves by the European Central Bank (ECB).

I expect a dovish SNB decision to drag the Euro (EUR) down in addition to the Franc, allowing for a correction for the common currency after several strong weeks.

5) BoE on course to hold rates high on expectations of defense spending

Thursday, 11:00 GMT. The Bank of England (BoE) faces its own "between a rock and a hard place" moment. On the one hand, the United Kingdom (UK) economy is struggling to grow, so rate cuts could support it, and would adjust to lower inflation. On the other hand, the UK government pledged massive defense spending, which implies stronger expansion and a need for higher borrowing costs.

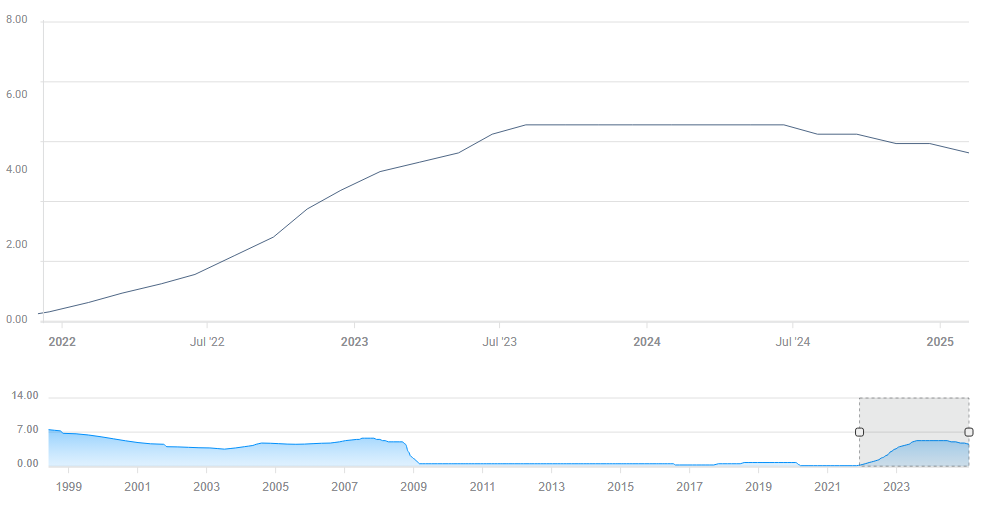

BoE interest rates. Source: FXStreet.

In addition, there is high uncertainty about the scope of US tariffs on the UK and their impact. This uncertainty implies leaving interest rates unchanged, but the Monetary Policy Committee (MPC) outcome will likely be split.

After all nine MPC members backed cutting rates last time, two are expected to support another such move this time, while seven others, including Governor Andrew Bailey, are projected to oppose the move.

If more members support reducing borrowing costs, the British Pound (GBP) would suffer, while a broader majority favoring a no-change decision would buoy Sterling.

Final thoughts

What about Trump's tariff policy? While headlines related to duties will likely pop up during the week, I expect them to be on the backburner this week. The next big decision on the topic is due on April 2, so markets will likely take a break and refocus on the topic next week.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.