Five Fundamentals for the week: Currencies set to rock on diverging central bank decisions

- The European Central Bank is set to cut rates by 25 basis points, extending the downtrend in borrowing costs.

- Australia is set to stand out by holding rates unchanged.

- US CPI figures will likely point to stubborn underlying inflation.

The only way is down – but not in the land down under. Central banks in the Eurozone, Canada and Switzerland are on course to cut rates this week, ahead of a similar move in the US next week. Inflation data in the world's largest economy stands out as the main macro data release.

Before diving into central banks, a quick word about the Middle East. The dramatic collapse of the Syrian regime is a historic moment and may open opportunities – as well as risks – for the war-torn country and the region. However, markets will likely ignore developments. A power struggle for control of Syria is up next, with little immediate chance of escalation – at least not one that would impact Oil prices.

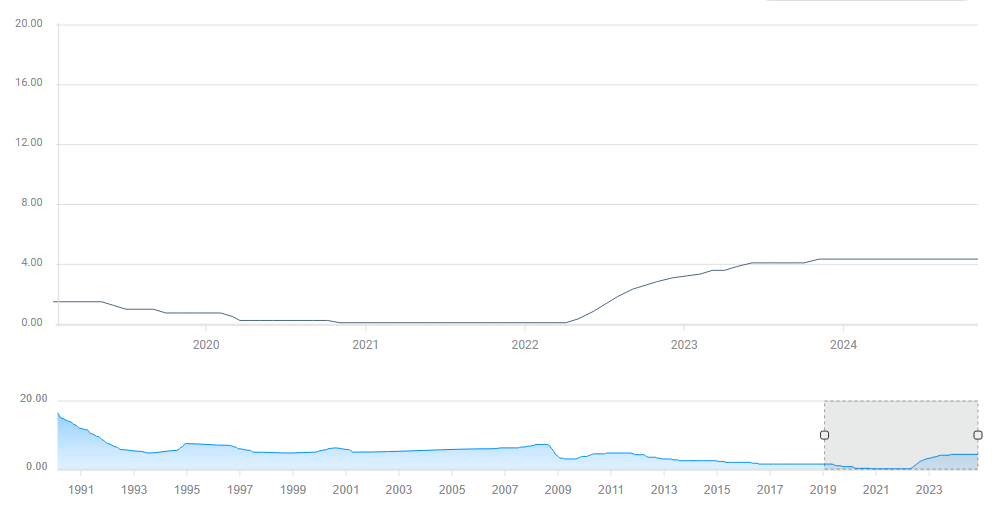

1) RBA set to keep rates unchanged despite worries about China

Tuesday, 3:30 GMT. The Reserve Bank of Australia (RBA) is set to keep rates unchanged at 4.35%. RBA Governor Michele Bullock is a hawk, and she also has good reasons to hold borrowing costs at elevated levels.

The RBA has yet to cut rates in this cycle:

RBA interest rate. Source: FXStreet.

Australia's unemployment rate stood at 4.1% as of October, a low level. Inflation has dropped from the highs, but there is no risk of deflation like in China, the country's main trading partner.

In case Australia holds rates, the Australian Dollar would rise during the week, especially as other central banks decide to cut rates. In the less likely chance of a rate cut, not only would the Aussie suffer, but investors would take note that even the relatively robust Australia is worried – hurting global Stocks.

2) Core CPI remains the focus of the US inflation report

Wednesday, 13:30 GMT. For three months in a row, the core Consumer Price Index (core CPI) hit 0.3% MoM, reflecting an annualized increase of 3.6% in each of these months. That is not what the Federal Reserve (Fed) wants to see, but more of a drop toward 2% in underlying price rises.

Another such increase would probably not hold the Fed from its expected 25 bps cut next week, but it would raise the path of borrowing costs for 2025. That would boost the US Dollar (USD) and weigh on Gold and Stocks.

While inflation has been mostly defeated and the Fed focuses on jobs, any surprise in core CPI would move markets, especially if the surprise is 0.2% off expectations.

3) BoC expected to cut by 50 bps after Canada reports jump in unemployment

Wednesday, decision at 14:45 GMT, press conference at 15:30 GMT. Contrary to the RBA, the Bank of Canada (BOC) is expected to stand out by going further along the rate-cutting trend. The economy of the North American country is hitting several bumps on the road.

Canada's recent jobs report showed a disappointing increase in the unemployment rate to 6.8%, moving further away from the US. America's president-elect, Donald Trump, has threatened to slap tariffs on Canada if it doesn't curb incoming migration, adding to the nation's political crisis.

Governor Tiff Macklem and his colleagues will likely paint a relatively bleaker picture of the local economy, justifying the cut, but may refrain from committing to imminent further rate cuts. In such a case, the Canadian Dollar (CAD) may experience a bounce on a "buy the rumor, sell the fact" response.

If Mackelm signals further rate cuts in early 2025, the Canadian Dollar would suffer, and it could also adversely affect the Greenback – the BoC's forecasts are also based on the outlook for the US, as the vast majority of Canadian exports go to America. Pessimism about the US could have wider implications.

4) SNB may surprise with stable outlook

Thursday, 8:30 GMT. The Swiss National Bank (SNB) meets only once per quarter – and it has a tendency to surprise markets. In the past five rate meetings, its decisions caught markets off guard in three cases – all to the dovish side.

Switzerland has low inflation and a depressed interest rate of 1%, and economists now expect a further cut to 0.75%. However, the SNB may decide to take a break from further moves.

One of the reasons for lower inflation came from the strong exchange rate of the Swiss Franc (CHF), a result of tensions in the Middle East. Now that tensions have subsided somewhat, the Franc has been on the back foot, making a rate cut less imminent.

In case the SNB surprises by leaving rates unchanged, not only would the Franc rise, but the Euro could also benefit, as it would imply a tougher stance from the European Central Bank (ECB).

If the SNB cuts rates as expected, there would be a negative impact on the Franc, but not as big as a surprise decision to keep rates on hold.

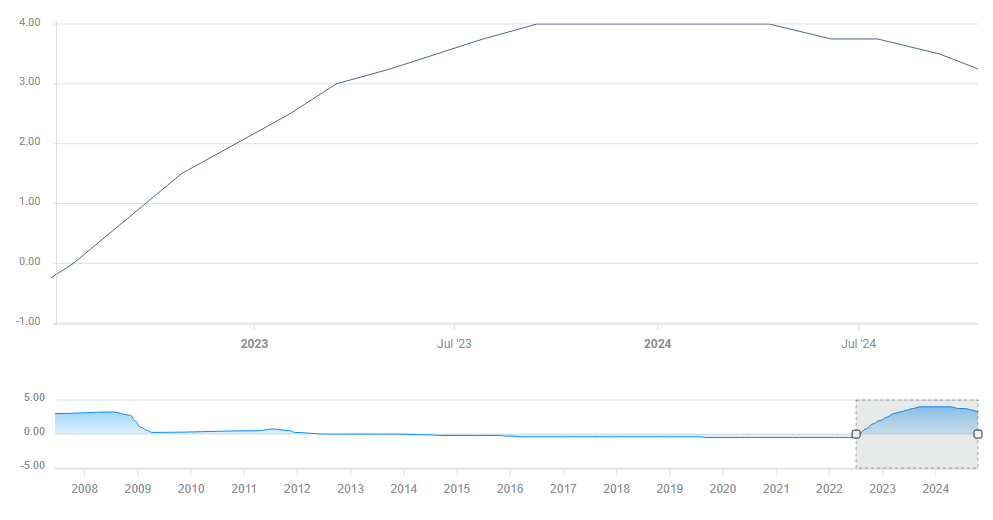

5) ECB may hurt Euro with uncertain outlook

Thursday, decision at 13:15 GMT, press conference at 13:45. Third rate cut in a row? That is the expectation from the ECB. However, projections of larger rate cut have largely faded. While inflation dropped in the old continent, recent figures have shown stability. Moreover, growth has somewhat exceeded expectations, showing that not all is doom and gloom.

ECB Deposit rate. Source: FXStreet

On the other hand, Europe suffers from political instability in Germany and France, the largest countries. The French government collapsed and Germany is heading to elections in February. Both economies are struggling.

There is also growing uncertainty about the policies of the next US administration. I expect the Frankfurt-based institution to cut rates by 25 bps as expected, but its forecasts and message may be mixed and uncertain, with so many moving parts.

What do markets do in the face of uncertainty? They punish the related assets. Even if the ECB refrains from a more significant cut and refuses to commit to further big moves, I expect the Euro to suffer, extending its recent decline.

Final thoughts

The fact that central banks are moving at different paces increases uncertainty and volatility. Trade with care.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.