Firm productivity gains helping the inflation fight

Summary

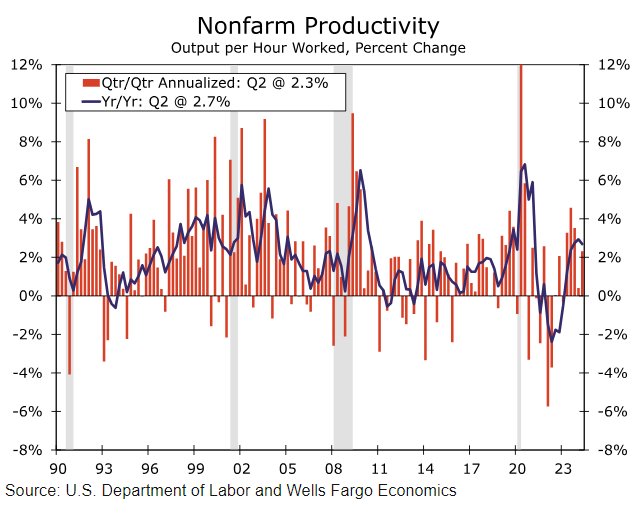

Nonfarm labor productivity increased at a stronger-than-expected 2.3% annualized rate in Q2, bringing the year-ago change to 2.7%. The pickup helped tamp down growth in unit labor costs. Unit labor costs are now growing less than 2% on trend and provide further evidence that inflation pressures from the labor market are easing.

Working smarter

Productivity optimists received another indication of improving labor efficiency today. Nonfarm labor productivity, measured by output per hour worked, increased at a 2.3% annualized rate in the second quarter. The better-than-expected outturn comes on the heels of a meager 0.4% rise in the first quarter and brings the year-over-year percent change to 2.7% (chart). Through Q2, labor productivity growth has averaged 1.6% this cycle, a touch stronger than the past business cycle's 1.5% average (2007–2019).

The firming in productivity growth is notable because it has scope to improve the economy's potential rate of growth. As we wrote in a series earlier this year, potential GDP growth is primarily determined by two factors: the labor force and labor productivity. Both factors were growing at historically weak rates before the pandemic and were expected to continue on lackluster paths through mid-century. Yet the recent momentum in productivity suggests those expectations are going a little stale. We suspect remote work and broadening adoption of artificial intelligence will be supportive of solid labor productivity growth in the coming years, which could meaningfully boost economic growth without leading to higher inflation.

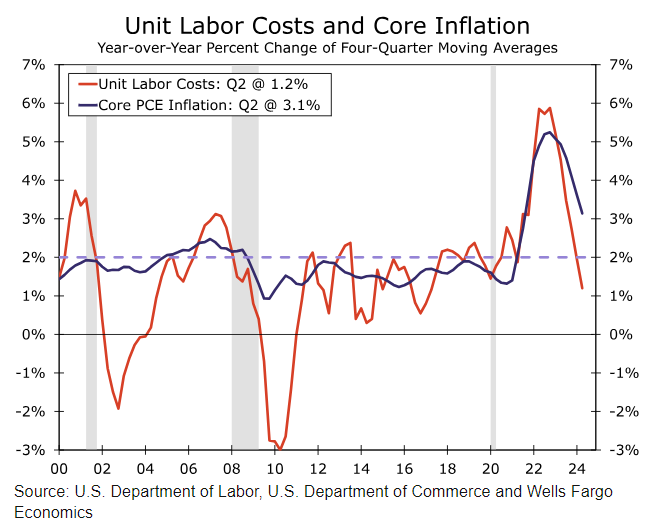

Indeed, the pickup in productivity in Q2 helped tamp down growth in unit labor costs (ULCs), which can be thought of as the productivity-adjusted cost of labor. Compensation per hour worked rose at a 3.3% annualized clip in Q2, but ULCs rose at a more modest 0.9% pace as employees were able to produce more in a given hour of work.

We are hesitant to take too much signal from a single release because productivity data tend to be volatile on a quarter-to-quarter basis. When smoothing annual growth with a four-quarter moving average, however, the trend in ULC growth is firmly down (chart). The tamer run-rate of unit labor costs, taken together with the moderation in nominal compensation costs per the Employment Cost Index in Q2, adds further evidence that inflation pressures from the labor market are easing. Amid the softening labor market and subsiding inflation pressures—thanks in part to productivity gains—we expect the Federal Reserve to embark on a series of rate cuts beginning at its next meeting on September 18.

Author

Wells Fargo Research Team

Wells Fargo