Fiction is ending now and the Euro is fading

Euro

One key reason for the euro to have firmed up in the first half of April was the dawning realization that the war was going to raise inflation and thus expectations of ECB rate hikes—while the US stays on hold or even cuts. That fiction is ending now—see the CME Fed funds futures section below—and the euro is fading. Support of a kind is the previous low at 1.1655, with the B band a little higher at 1.1688. A lasting break of one or both implies the party is over.

Outlook

Today we get the US trade balance, JOLTs, new home sales for Feb and March, the S&P final services PMI, and the ISM services, the preferred one. Tomorrow is nearly empty—only the ADP private sector jobs report. In the absence of reliable war news, real data may get more attention, probably JOLTs.

Yields are curiouser and curiouser. Yesterday the US 10-year hit a high of 4.4620%, which scared some of the horses, but this high is still not to the two previous highs, 4.5290 from 4/29 and before that, 4/4840 from 3/27. The dollar index rose, to be sure, but not commensurately.

To go probably a little too far, this can be interpreted as implying traders think Trump will chicken out of a serious bombing attack. It’s not the same thing as backing down, but it could imply that the ceasefire, ragged though it be around the edges, is still in place and neither side wants it to end. We can still have plenty of bad, awful, terrible things happen but it’s not outright war.

One possible reason for the yield to jump is that the Fed funds market is starting to re-think it’s “hold forever” stance. Remember that last week no change was seen in the Fed funds futures until next year. Now Chandler points out Fed funds futures have “swung in favor of a hike yesterday and is now pricing in slightly less than a 1-in-4 chance of a rate increase.”

The outlook for the Dec 9 Fed meeting has the probability of no change at 65.3%, for one hike at 26.2% (from zero a week ago) and for two hikes at 2.7%.

Never mind Mr. Powell staying on and Mr. Warsh potentially being a Trump sock puppet. The inflationary effect of the oil prices rise zooming through everybody’s inflation data can’t be ignored. It was always silly to imagine the rest of the world will be hiking while the US stays on hold or cuts. This is reality-checking and the CME is delivering the evidence, soft though it may be.

Forecast

We wrote yesterday “Now that we have some war news, and expectations of war news, risk aversion has to rise again and the dollar may well resume its safe-haven status. The underlying sentiment is anti-US and anti-dollar, but the prospect of real war, and now Fed rate hikes, crushes risk appetite.

We need to remember that anxiety and tension can become unbearable and traders do one of two things—freeze, or go the other way. Some of this is rational re-positioning but a lot of it is plain, old-fashioned nervous breakdown. We expect mini-reversals and/or sideways whipsawing and/or a big drop in volume and thus liquidity (hence gaps). In other words, nasty conditions.

That’s until a tipping point arrives, as it must. That is either Trump backing down or re-starting the shooting war. We have taken the view that the shooting war version is more likely, if only Trump’s vanity wouldn’t allow him to be named a chicken again. He has to live amongst the hawks he gathered around him and now must reap what he has sown.

Predicting Trump is a crazy way to forecast FX. We should stick to the relative interest rate diffs and central bank narratives. Bottom line, we expect the dollar to come back, potentially very fast, and swamp buy signals in the major currencies. We already see it in the EMs (peso and yuan). Run.

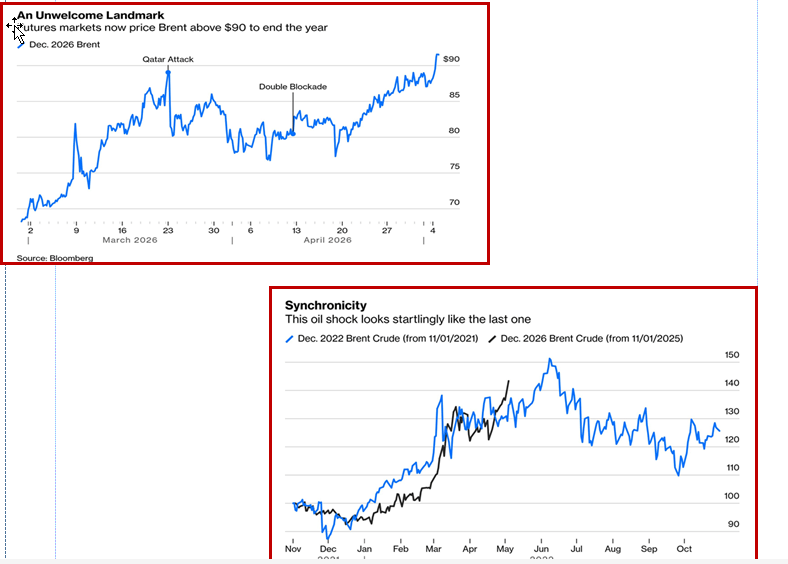

Tidbit: Bloomberg points out that the forecasts for oil prices have been perhaps too anchored to whatever is current. See the charts. Forecasts of $150 and $180 and now $200 are not unrealistic. $150 is particular seems to be about to come true.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat