Fed’s hawkish pivot may be closer than markets expect

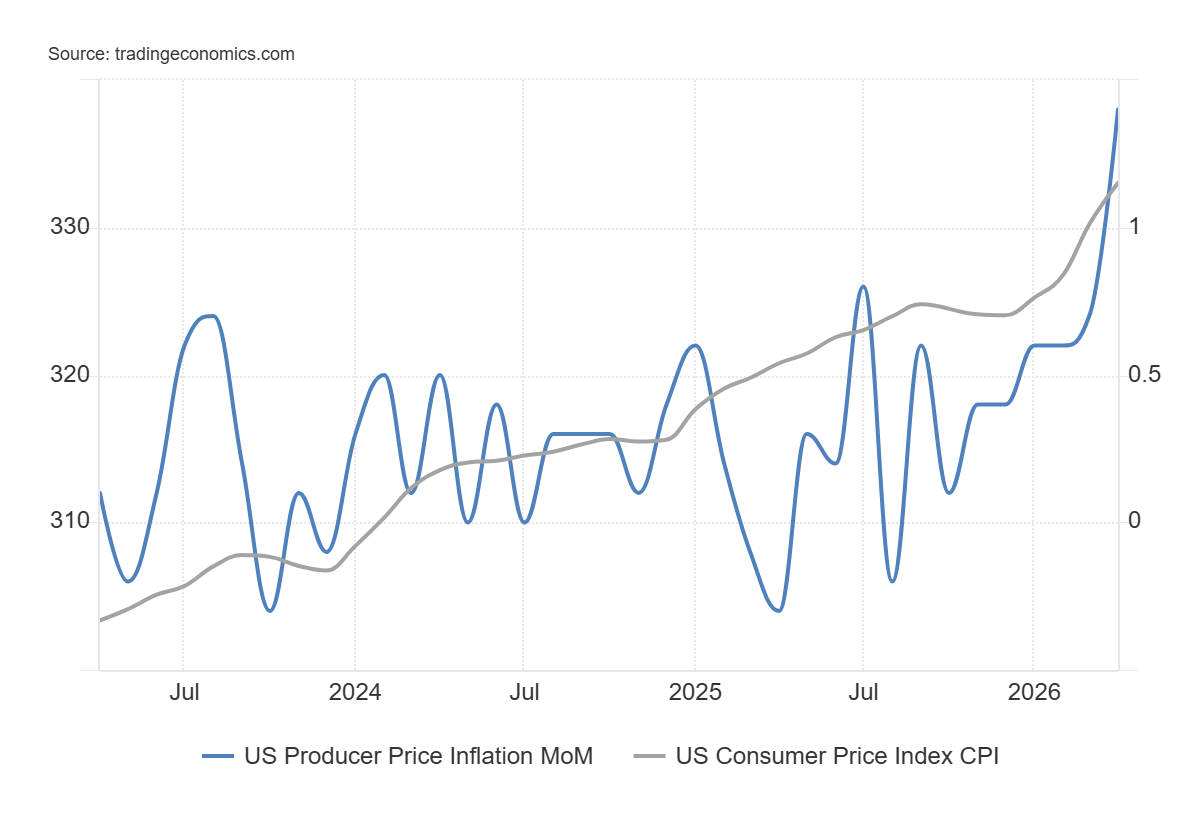

A 6% Producer Price Index print, the hottest in nearly four years, landed on a market that has spent most of 2026 quietly preparing for the wrong policy regime. The assumption being made by markets is that the Federal Reserve (Fed), faced with a labor market that has added effectively no net jobs in 12 months, will not have the stomach to hike interest rates even if inflation keeps screaming higher.

Boston Fed President Susan Collins took aim at that assumption on Wednesday in remarks to the Boston Economic Club. Newly confirmed Fed Chair Kevin Warsh ran on a platform of dismantling it. The House Financial Services Committee (HFSC) is now examining a bill that would surgically remove the legal basis for the dovish read. The market has noticed each piece individually. Futures pricing suggests it has not yet connected them.

The print that closed the dovish door

The April Producer Price Index (PPI) was not the kind of release that allows for a dovish interpretation. Headline producer prices rose 1.4% MoM, nearly triple the 0.5% consensus and the largest monthly increase since March 2022. On a YoY basis, PPI accelerated to 6%, far above the 4.9% consensus and the hottest reading since December 2022. Core PPI, which strips out food and energy, climbed 1% MoM and 5.2% YoY, also smashing forecasts of 0.3% and 4.3%. Energy did much of the heavy lifting, with gasoline prices up 15.6% as the war with Iran continued to squeeze global Oil flows.

However, the comfortable "this is just Crude Oil" framing collapsed when the services component within PPI figures rose 1.2%, the broadest gain since March 2022. Inflation is sticky and accelerating; the crisis in the Strait of Hormuz is aggravating the problem, but the problem goes way beyond Crude Oil. The latest Consumer Price Index (CPI) inflation figures, released on Tuesday, already set the table. Wednesday’s PPI print confirmed the meal.

The labor side isn't the brake the market thinks it is

The standard counterargument is that the Fed cannot hike into a softening labor market, and on the surface, the data backs that view. April Nonfarm Payrolls (NFP) beat consensus at 115K, but the internals were ugly. The household survey added 358K newly unemployed and 445K newly involuntary part-time workers, roughly 803K Americans into fresh labor-market distress in a single month. The three-month payroll average sits at just 48K. Labor force participation slipped to 61.8%, the lowest reading since October 2021. Underemployment hit 8.2%. The Bureau of Labor Statistics (BLS) itself framed the prior 12 months as showing "little net change." This is the data the market is leaning on when it prices roughly a 40% chance of a hike by year-end and effectively zero probability of a cut in June.

The trouble is that the Fed has spent the last three weeks publicly telling traders that it no longer treats this data as the constraint it once was. The dovish read assumes the Fed will protect the labor market. The Fed has stopped saying it will.

Collins, the dissenters, and a new Chair

Collins's remarks to the Boston Economic Club on Wednesday were the most direct statement yet. While stressing it was not her base case, the Boston Fed President said she "could envision a scenario in which some policy tightening is needed to ensure that inflation returns durably to 2% in a timely manner." The line that should have moved markets harder than it did was sharper: "more than five years of above-target inflation has reduced my patience for 'looking through' another supply shock." That is the rhetorical prerequisite to a hawkish pivot, not the consequence of one.

At the April 29 Federal Open Market Committee (FOMC) meeting, Dallas Fed President Lorie Logan, Cleveland Fed President Beth Hammack, and Minneapolis Fed President Neel Kashkari dissented on the easing bias embedded in the post-meeting statement, arguing the next move could just as easily be a hike as a cut. Newly confirmed Fed Chair Warsh, set to take over when Jerome Powell's term ends Friday after a 54-45 vote, told the Senate he intends to pursue "regime change" at the Fed, including a smaller balance sheet and tighter Treasury coordination. The institutional drift toward an inflation-only Fed is happening regardless of what the rate curve thinks.

Six words from Capitol Hill

The political backdrop is moving in parallel. The HFSC is examining H.R. 5396, the Price Stability Act of 2025, which would amend Section 2A of the Federal Reserve Act by striking "maximum employment, stable prices," and inserting "stable prices". Six words. That is the entire statutory edit required to remove the employment leg from the Fed's mandate. The bill is unlikely to clear the Senate in its current form, and probably will not need to. Its existence and committee progress matter for a different reason: they lower the political cost of a hawkish pivot.

A Fed Chair who hikes into a softening labor market under a dual mandate takes career and institutional risk. A Fed Chair who hikes into a softening labor market while Congress is publicly debating whether the labor mandate should even exist takes far less. The bill is not the spine of the hawkish case; it is the cover.

Why the curve is still asleep

Futures pricing of roughly 40% hike odds by year-end sounds, on first read, like the market is taking the threat seriously. It is not. That is hedge pricing, not base-case pricing. A 40% probability paired with effectively zero cut probability for the next two meetings describes a curve that has priced out cuts but not yet priced in hikes. The gap between those two states is where the next leg of volatility lives: if the Fed pivots in June, or even credibly signals a pivot, that 40% needs to move quickly toward 60-70%.

Front-end yields would jump, the US Dollar would extend gains, rate-sensitive equities would reprice lower, and gamma would be in short supply. The setup is asymmetric because the dovish surprise has nowhere to go. Absent an immediate labor-market collapse, there is no credible path to a June cut. The hawkish surprise has multiple paths: a hot May CPI on June 11, a labor reading that is merely "less bad", a fresh escalation in the Strait of Hormuz, or simply Warsh signaling at his first FOMC press conference on June 17.

Three registers, one direction

The outgoing Fed Chair adds one more wrinkle: with Powell's awkward afterlife staying on as governor through January 2028, Warsh inherits a seat at the table with the architect of the old regime sitting across from him. That should complicate the regime-change narrative. In practice, with Collins and three regional dissenters already aligned with the hawkish camp, Powell looks more likely to be outvoted than vindicated. The dual mandate has stopped being a constraint at the personnel level. The bill is making it not a constraint at the statutory level.

The data has stopped being a constraint at the economic level, because the Fed has already chosen which side of its mandate to weigh. The Fed has told traders, in three separate registers, what it intends to do. The question is no longer whether to believe the dovish read; it is how long the curve can keep pretending it still matters.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joshua Gibson

FXStreet

Joshua joins the FXStreet team as an Economics and Finance double major from Vancouver Island University with twelve years' experience as an independent trader focusing on technical analysis.