How Kevin Warsh upended the game plan for Gold

Something is breaking inside the Federal Reserve's new strategy, signaling a massive regime change for macro markets. Under the leadership of newly appointed Fed Chair Kevin Warsh, the traditional framework of forward guidance and predictable rate paths could be dismantled soon. For Gold traders, this structural shake-up means the historical inverse correlation between real interest rates and Gold is officially back, forcing a market repricing.

A regime change at the Federal Reserve

It wasn't just a chair swap. This wasn’t just replacing a challenged Jerome Powell with a fresh face in Kevin Warsh: It was a system swap.

For over a decade, markets operated on a simple framework. The Fed would telegraph its intentions through something called forward guidance. You had the Summary of Economic Projections – every FOMC member forecasting where they expected inflation, employment, and GDP to go. Within it, you had the dot plot – every FOMC member publishing where they expected rates to go. You had the policy statement, carefully worded, obsessively parsed. You had press conferences after every meeting. And above all, you had predictability.

That entire structure is now gone. Kevin Warsh didn't walk in and tweak Powell's system; he aims to dismantle it. He announced that he will create task forces – five of them: each one assessing Communication, Balance Sheet, Data, Productivity and Jobs, and an Inflation Framework review. These aren't just advisory panels. They will provide the new inputs that the Fed will follow.

Warsh also chose not to provide his interest-rate expectations in the dot plot. No more published rate path from the most powerful person in the room. He wants flexibility and agility – words that sound more Silicon Valley than Washington, DC. The statement? Cut down to half the length, from over 300 words to just about 150. What about press conferences? They could be gone, or not. He may only speak when he decides he has something to say. More unpredictability.

All this takes us back to the Alan Greenspan era, 25 years ago. Warsh admires Greenspan. Again, history repeats itself. Before the Global Financial Crisis made the Fed commit to carefully dictating all its thinking to the markets, the Fed used to work like this: short statements, short pressers, and just focus on the data.

The only thing different from the Greenspan era is that inflation is now surging. But think about what all that means. Markets have spent a decade learning how to read the Fed: entire trading desks, hedge fund strategies, macro newsletters, and analysis tools are built around Fed-watching. And that edge just evaporated.

The market's first reaction said everything: violent repricing. Something broke inside the market’s structure. Gold crashed. The US Dollar surged. Stocks topped. All led by 2-year Treasury yields moving up – which is the market saying: we no longer expect a rate cut coming soon. Rather, expect a hike.

Why is the Gold and real rates correlation back

Kevin Warsh basically turned the Fed upside down – under his leadership, the FOMC will likely publish reduced statements, provide no forward guidance, and he might even bypass press conferences after meetings. But what does this mean for the markets going forward? And more specifically, what does it mean for Gold traders?

Now here's where most retail traders get this wrong, because the misunderstanding is expensive. People say Gold goes up when rates go down. That's only half true. And the half they're missing is what's going to cost them.

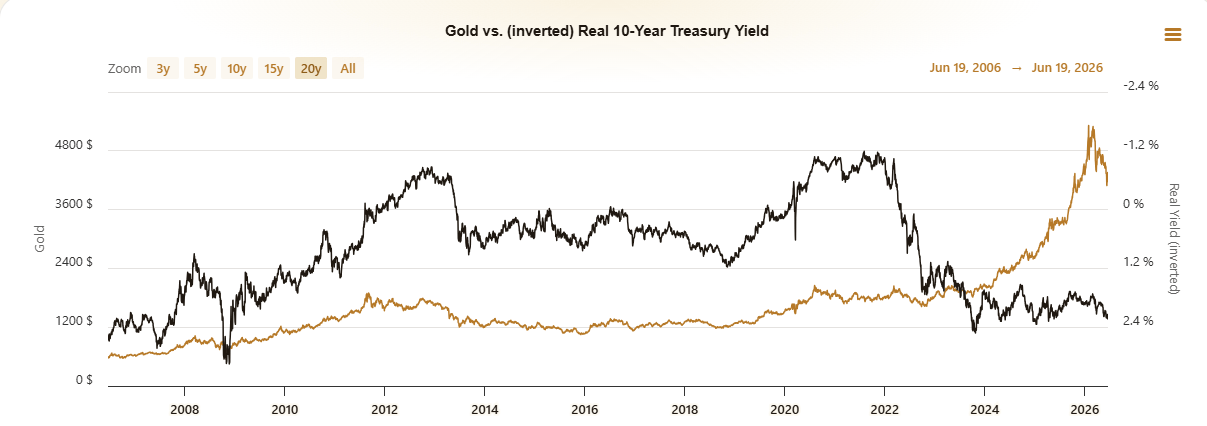

Gold doesn't move with nominal interest rates. It moves with real interest rates – that's nominal rates adjusted for inflation. When real rates are negative, holding Gold has no opportunity cost. You're not giving up yield by owning a bar of metal. But when real rates turn positive and rise – when you can earn real purchasing power from holding US Treasuries – Gold becomes expensive to hold. Historically, the correlation is tight, and it's inverse.

The relationship between Gold and the real yield on 10-year Treasuries is very strong. Now look at what happened over the past two years. That correlation broke. Gold skyrocketed even as real interest rates stayed elevated – because the market had a new driver: a crisis of confidence in the US Dollar itself. Trump is trying to fire the Fed chair, tariff chaos, fiscal deficits, and geopolitical noise. Gold wasn't trading on rates – it was trading on the US Dollar's lack of credibility.

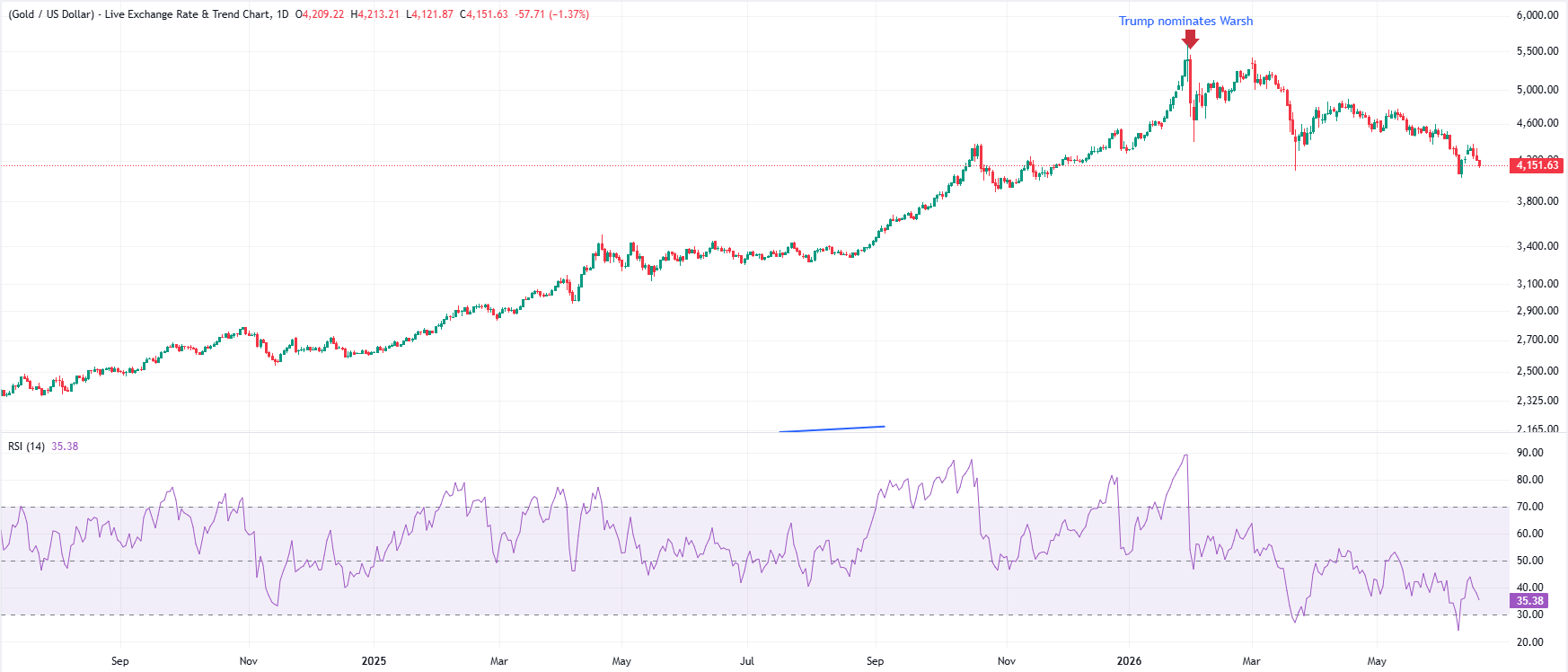

Here's what Warsh might have changed. Gold peaked the day before Trump nominated him as the new Fed chair, last January. Coincidence? Don’t think so. Macroeconomics is back to work. The Gold-real rates relationship is back. And that data is telling you something very clear: gold is not cheap here. It’s still trading above $4,000, a level that was not reached until October 2025.

The political and economic contradiction facing Warsh

The first market assumption on Warsh might have been that he’s an inflation hawk, and that’s why Gold is down. But there's tension at the heart of the Fed – and it's the thing that makes this so tradeable. Warsh was appointed by Trump. And Trump wants lower rates. He's been vocal about it for years – lower rates to stimulate consumption, reduce the cost of US government debt, keep the economy moving. Jerome Powell refused for months, and Trump went after him publicly, relentlessly.

But when Warsh held rates and gave zero hints of a cut? The US President was quiet. He said Warsh is "guided by what he wants" – and just added that higher rates "keep the country down." That's not pressure. That's patience, at least for now.

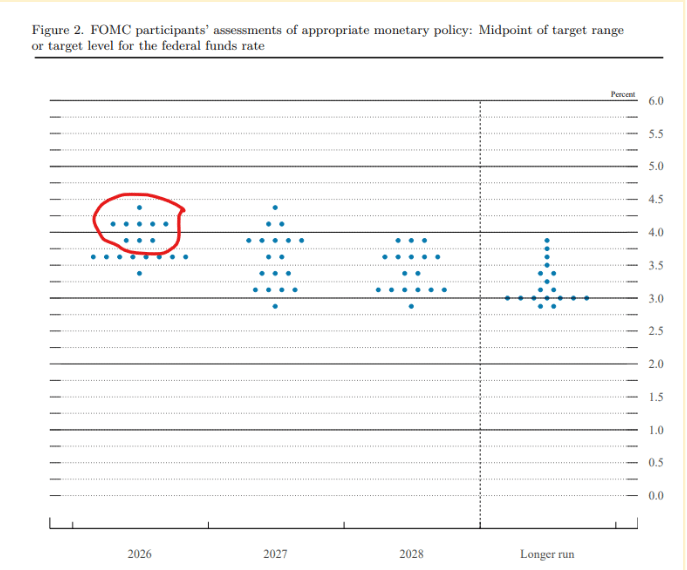

But look at the dot plot that the FOMC released on June 17. The little dots represent the current vision of each member of the Federal Open Market Committee. These are the people who decide monetary policy. Nine of eighteen members see higher rates by year-end. Core PCE is now projected at 3.6% – up from 2.7% previously. The committee is hawkish. The data is hawkish.

And there is a simple reason why they are: the energy shock from the Middle East conflict. Rising Oil prices are the visible part. But the delayed effects – jet fuel, petrochemicals, natural gas, fertilizers, helium – feed into goods inflation in Q2, Q3, and Q4. The pipeline is full. The higher inflation prints are coming. So, how long can Trump wait until he’s unsettled again about what’s going on at the Fed?

Warsh is caught between a rock and a hard place. He needs and wants to get inflation down – he's said it plainly: "Inflation is a choice. You bet it is." But his political principal wants rates cut. And something, eventually, will have to break. The genius – or the danger – of his new system is that it gives him maximum cover. No chair dot to defend. No forward guidance to walk back. Private data delivered by task forces that outside analysts can't fully scrutinize. A thin paper trail. He can change course from one meeting to the next and justify it as data-driven agility. Whether that's a feature or a bug depends on how much you trust him.

Shifting strategy: Trading the data, not the Fed

Trump nominated Warsh for his lower-rate stance, but in his first meeting, the new Fed chair sounded like an inflation hawk, and the market sold off. What's the actual trade here?

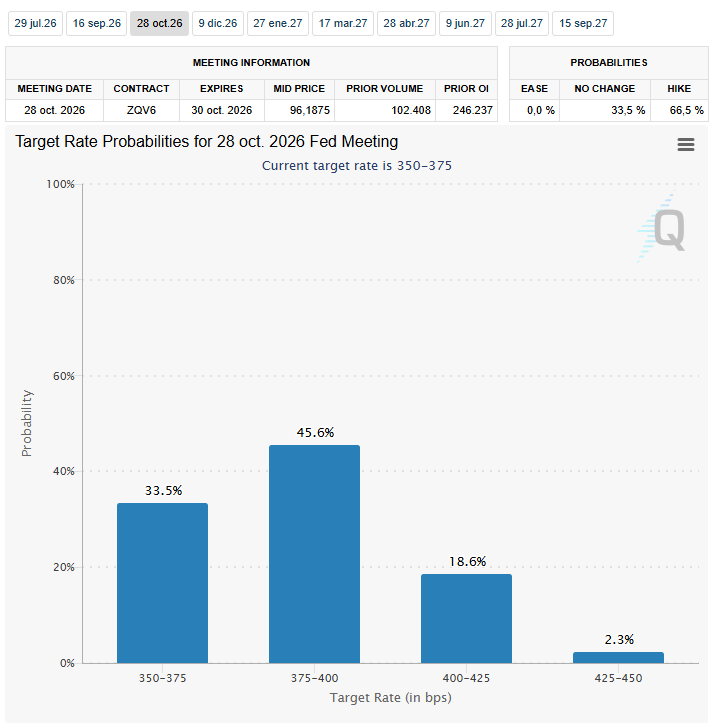

Stop trying to read the Fed; they’re not going to tell you what they will do. Trade the data instead. Every economic print between now and the next FOMC decision is the event. Front-end Treasury yields and the US Dollar are your leading indicators. Right now, both are signaling a rate hike by October – CME Group’s FedWatch tool is pricing it at a 60% implied probability of fed funds rates above the current 3.50%-3.75% range.

That backdrop is not friendly to Gold. Not here, not at these levels, above $4,000. But here's the trap to avoid. Not all the data is the same. Don't trade headline CPI. Headline inflation may well decline if oil keeps pulling back. That's a head-fake. Instead, Warsh gave us a clue back in April, during his confirmation hearing. He said he prefers to look at inflation with “trimmed averages.”

“Trimmed-mean averages” are alternative inflation measures released by regional Fed banks, such as the Cleveland Fed's 16% Trimmed Mean CPI and the Dallas Fed's PCE inflation rate. These figures exclude extreme readings above the 92nd percentile and below the 8th percentile, resulting in a much lower variance and smoother trends. In the context of an Oil shock like the current one, this might mean less weightage on skyrocketing energy prices. Does this mean lower inflation rates than the headline and core readings? Is this actually dovish, then?

It could be. President Trump wants lower rates, and Warsh might find some room to deliver them if he can ignore the undeniable spike in headline inflation imported from the Middle East.

So, circle CPI and PCE inflation releases on your economic calendar, but don’t focus on headline numbers. Instead, dig deeper into the data that Warsh and the FOMC members will scrutinize. If these Trimmed-Mean measures come in hot, the rate hike odds climb further, real yields push higher, and Gold has another leg down. If these surprise to the downside, you'll get a relief bounce.

Still, something will have to break. The Gold bull narrative was based on a Fed that was going to cut. Right now, that Fed doesn't exist. And we don’t know if it will. For almost two years, gold traded on fear – fear of dollar debasement, fear of fiscal collapse, fear that the US was losing its grip on global credibility. That fear trade was real, and it worked. But all trades eventually end. They end when something changes structurally. And what has changed is this: the Fed now has a chair who won't tell markets what to expect.

So, markets are back to what worked in the past. Real rates are rising. The US Dollar is finding its footing. And that historical chart between real yields and Gold is back in play. Game over for the gold bulls – at least for this chapter. Watch the data. Trade the prints, not the promises.

(This article was created with the help of an Artificial Intelligence tool and reviewed by an editor.)

Author

Dhwani Mehta

FXStreet

Residing in Mumbai (India), Dhwani is a Senior Analyst and Manager of the Asian session at FXStreet. She has over 10 years of experience in analyzing and covering the global financial markets, with specialization in Forex and commodities markets.