Federal Reserve Rate Policy: The 2% solution

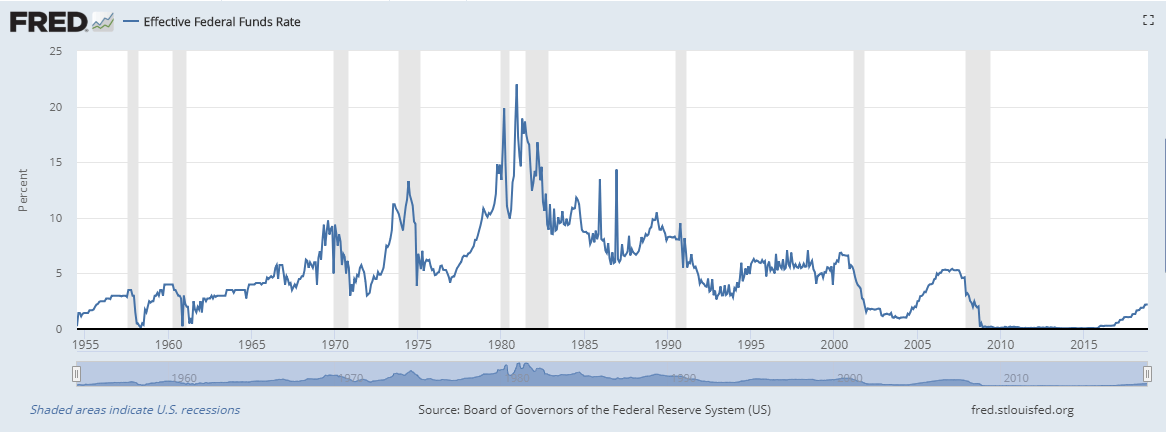

The intriguing question about Federal Reserve rate policy is not will the governors continue to raise the Fed Funds rate. They have made their expectations clear. Rates will go up for at least two more years. The more interesting question is what are the conditions that will make them stop?

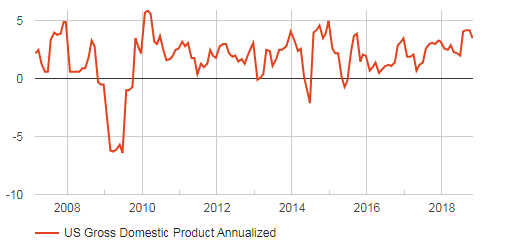

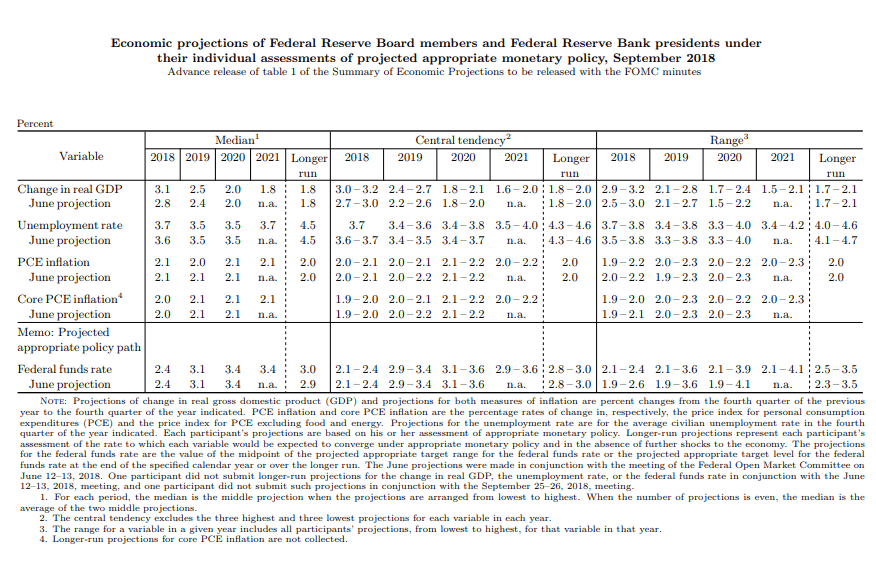

The bank issues its economic and rate projections four times a year. The latest was this past September. Bank economists and analysts anticipate GDP to expand at 3.1% this year. At the moment that appears to be a fair estimate. If the Atlanta Fed GDPNow program is accurate with its 2.9% fourth quarter estimate that would give GDP a 3.15% run this year.

When the FOMC adds 0.25% in December, as is uniformly expected, that would be the fourth hike this year to 2.5%. The governors’ rate projection for 2018 was increased in the June release to 2.4% from 2.1% and it formed the market expectations for rate policy.

Next year the bank anticipates growth will drop to 2.5%. The Fed Funds projection of 3.1% will require three 0.25% increases to cover it. At the end of next year, if the Fed’s expectation for economic growth are met the Fed Funds rate will be 3.25%.

Moving out one year the bank predicts 2% growth in 2020. That year the FOMC anticipates a 3.4% Fed Funds rate and one 0.25% increase to 3.5%.

In 2021 the economists see 1.8% growth and the governors anticipate no rate increases at 3.4%, the same as in 2020.

Beyond 2021, in what the projections call the longer run, GDP stays at 1.8% and the Fed Funds reverses to 3%, implying two 0.25% rate cuts.

In summary, growth in 2018 at 3.1% permitted four 0.25% increases taking the Fed Funds from 1.5% to 2.5%. In 2019 2.5% growth warrants three increases to 3.25%. In 2020 a 2% expansion elicits one quarter point addition to 3.5%. In 2021 a 1.8% expansion gets a flat Fed Funds at 3.4%. Out more than three years growth at 1.8% receives two rate decreases.

The accuracy of the Fed’s economic and rate predictions are not the question. The projections do not give any indication of where the neutral rate for the Fed Funds may be in the post-financial crisis world. They do however make the parameters of the governors’ economic threshold clear. Economic growth above 2% can tolerate increases in the Fed Funds, growth below cannot.

For a central bank that is akin to a barking hound.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.