Federal Reserve Preview: The Good, the Bad and the Ugly edition, three critical things to watch

- The Federal Reserve is set to leave its policy unchanged and acknowledge better conditions.

- Focusing on 9.5 million Americans out of work may serve as a dampener and a balancing act.

- Any stray dots in the bank's interest rate projections may cause turbulence.

"When you have to shoot, shoot, don't talk" – goes one famous line from "The Good, the bad and the ugly," yet that famous movie but the Federal Reserve has a different task this time. The world's most powerful central bank wants to convince markets it is unwilling to shoot up interest rates earlier than estimated and for good reasons. However, its task is complicated.

The Fed would like to bring investors to its views – growth is set to pick up without causing inflation nor triggering knee-jerk rises in interest rates. Federal Reserve Chair Jerome Powell said that the rapid rise in Treasury yields "caught my attention" but he seems more worried with the disruptive pace than the direction of travel.

The vaccine and stimulus-driven recovery warrants higher long-term borrowing costs – but don't shoot, talk first. In the March 17 meeting, the Fed publishes new forecasts, aka the "dot-plot" in which it provides collective views on growth, inflation, employment, and interest rates. These projections are set to determine the initial reaction, while Powell's press conference could alter the direction of travel.

Here is how the event may unfold, Clint Eastwood-style:

1) The Good – inflation just about right

Inflation can somewhat overheat to achieve full employment – that was the message of the bank's policy review. Base effects are set to boost year-over-year prices in the next few months, and both markets and everybody is willing to see through this near-term bump. But how far will the bank allow it to go afterward?

Rising growth prospects will likely push the Fed's long-term inflation forecasts, but these would probably stand around 2%, the bank's target. That would be a Goldilocks scenario.

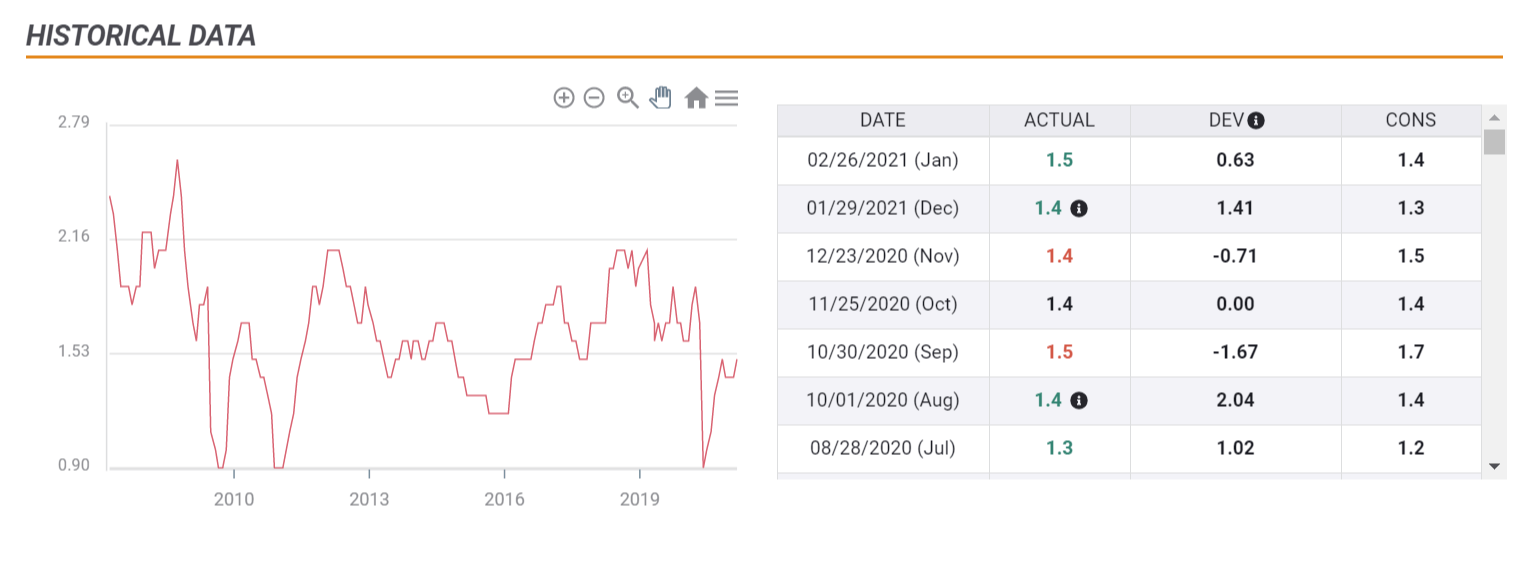

The Core Personal Consumption Expenditure gauge, which is the Fed's preferred inflation measure, remains tame:

Source: FXStreet

As the Washington-based institution has been falling short of its estimates for price rises for over a decade, seeing only modest rises would soothe market concerns about inflation and also interest rates. Forecasts for tame inflation are positive for stocks and adverse for the dollar.

In case the Fed boosts inflation forecasts, markets would fear rate hikes and in case they remain unchanged at low levels, investors would fear a gloomy growth outcome. Bringing the forecast to around 2% would be perfect, and that is the most likely outcome.

2) The Bad – Unemployment remains high

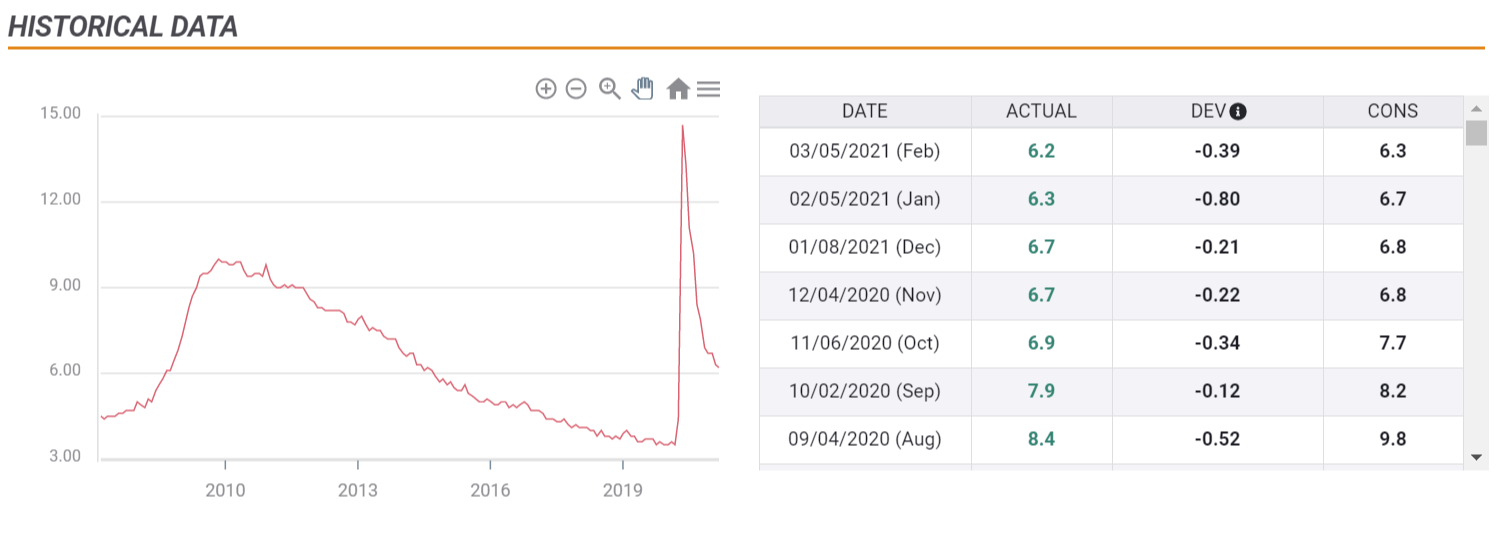

The Fed has moved away from focusing only on the headline unemployment rate and now looks at broader measures. These include how many have yet to return to their pre-pandemic jobs – somewhere around 9.5 million. Another gauge is the jobless rate among minorities such as Blacks, and the widest of measures, the employment-to-population ratio which fell off the 60% level.

Even if the bank pushes the unemployment rate projections down, it may stress that many people are out of work. Moreover, Powell is set to give it special attention in his press conference, as he did in recent public appearances.

Full employment is the second Fed mandate, alongside price stability. Balancing concerns of lingering joblessness with upbeat inflation and growth forecasts – the latter unlikely to raise any eyebrows – may keep markets in check. The rise in stocks and yields will likely remain tame.

US unemployment is falling fast, but it remains elevated by the Fed's broader set of measures:

Source: FXStreet

3) The Ugly – Interest rates

"Not even thinking of thinking about raising rates" – Powell's famous words echo in investors' ears but are growingly ignored. If the economy improves, can the Fed keep borrowing costs glued to 0% until 2023? Bond markets suggest the first hike will come in late 2022.

If President Joe Biden does not extend the Fed Chair's term, Powell will be gone early next year and the views of his colleagues will matter more. Hawks in the FOMC may markets already now and even if Powell stays on – by forecasting an earlier rate hike than expected.

While the consensus is set to remain for borrowing costs to remain at zero in the next couple of years, a small minority may bring expectations forward and rattle markets. If three or more foresee conditions necessitating an early hike, stocks would shiver and the dollar could shoot higher.

What happens if only one or two change their minds? That is where things may turn ugly. Markets may chop their way around and try to scrutinize every word that Powell says in his press conference. If he seems open to hikes under certain conditions, the "risk-off" scenario of a market sell-off applies. On the other hand, a "read my lips" style pledge to hold rates low until 2023 no matter what could keep markets happy.

Conclusion

Markets are at a juncture where they cheer growth but dread inflation that could come with it. The Fed has a fine balancing act and it may fail to stay on top of the tightrope.

More Five factors moving the US dollar in 2021 and not necessarily to the downside

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.