Federal Reserve Preview: Squaring the inflation circle

- Fed Funds target range 2.25%-2.50% not in question for the FOMC

- How does the Fed design a rate policy for strong economic growth and weak inflation?

- Market focus will be on Chairman Powell’s statement and news conference

The Federal Reserve will conclude its two day policy meeting of the Federal Open Market Committee (FOMC) on Wednesday May 1st. The central bank will release its rate decision and policy statement at 2:00 pm EDT, 18:00 pm GMT. Chairman Jerome Powell will read a prepared statement and hold a news conference beginning at 2:30 PM EDT, 18:30 pm GMT

Fed Policy

The US central bank’s near and intermediate rate policy has become a moot topic. After the FOMC’s 25 basis point increase to a 2.5% upper target at last December’s meeting, Chairman Powell and various governors, in speeches and comments carefully moved the bank to a neutral stance, mostly by citing overseas risks to US economic growth.

The January FOMC statement made it official. “In light of global economic and financial developments and muted inflation pressures, the Committee will be patient as it determines what future adjustments to the target range for the federal funds rate may be appropriate to support these outcomes.

In the same second paragraph of the December statement it had said, “That some further gradual increases in the target range for the federal funds rate will be consistent with sustained expansion of economic activity, strong labor market condition and inflation.”

US Economy

The US returned to robust economic growth in the first quarter. Gross domestic product expanded at a 3.2% annualized rate, much faster than the 2.0% forecast and the 2.2% pace in the final three months of last year.

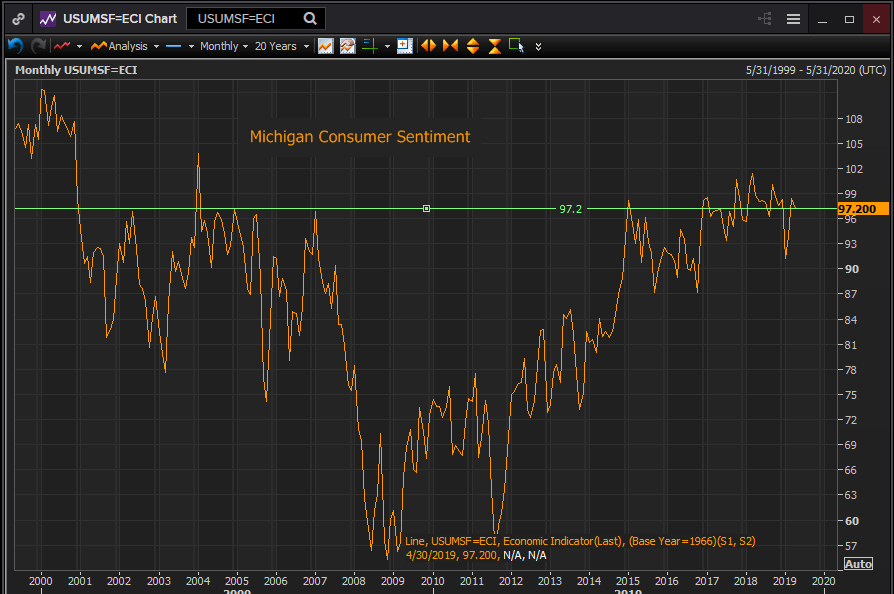

Consumer sentiment has recovered from its year end and shutdown plunge. The University of Michigan sentiment index scored 97.2 in April on par with its readings for the past two years and leaving the shutdown drop to 91.2 a one month oddity.

Reuters

The Conference Board index showed the same optimism. Its April measure was 129.2, well above January’s 121.7 and near the midpoint of the last two years.

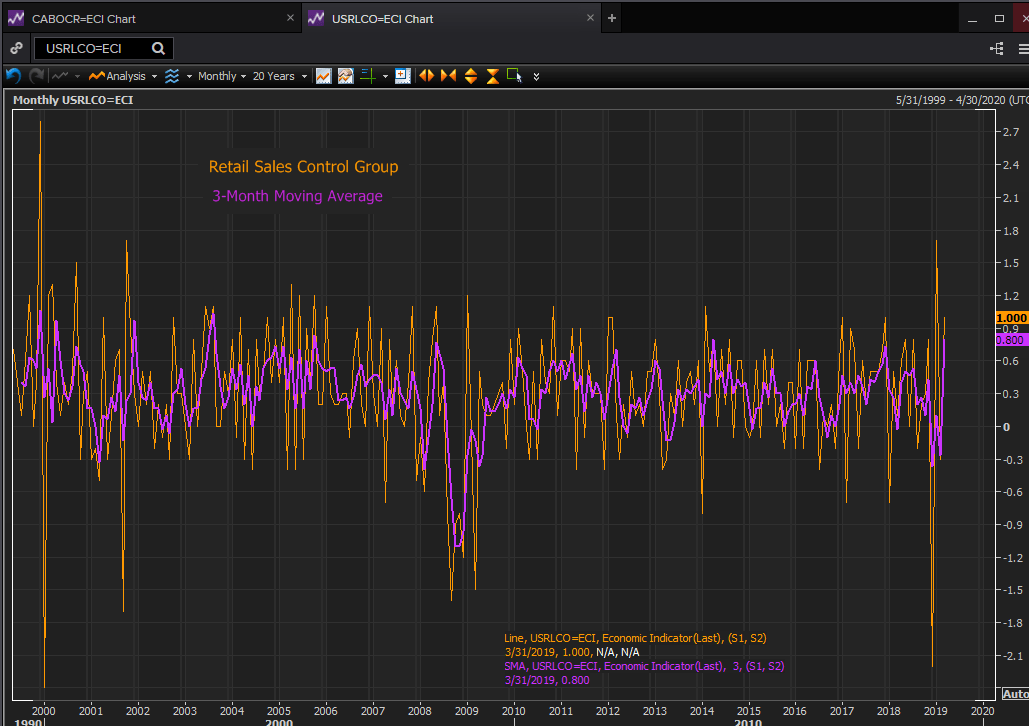

The consumer attitude was reflected in far better than expected retail sales numbers for March. Overall sales jumped 1.6%, the best reading since September 2017. The control group component of GDP climbed 1% in March, bringing the three month average to 0.8% its strongest performance in 14 years.

Reuters

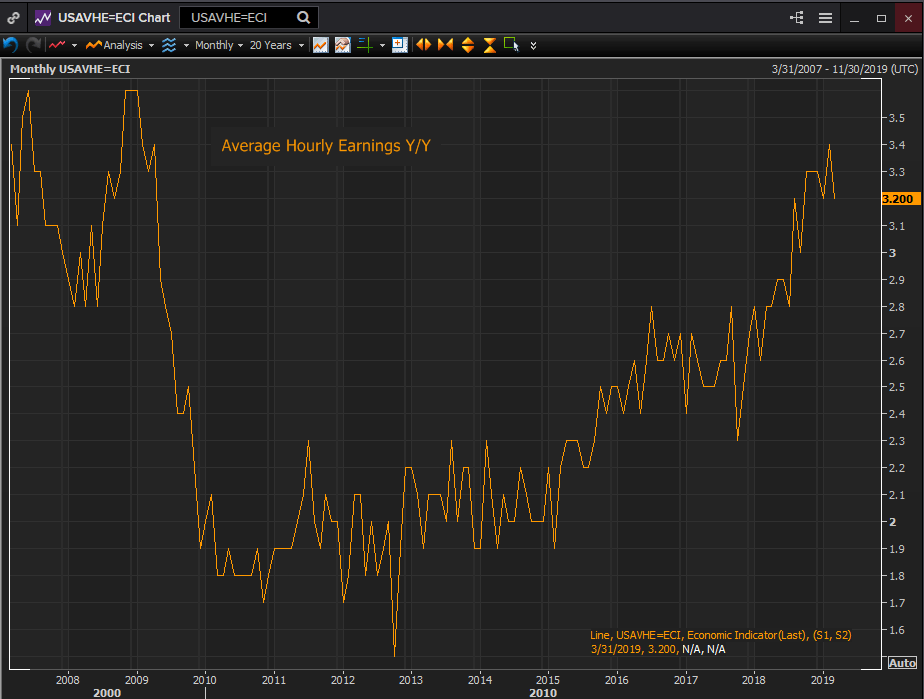

Consumers are responding to the continuing strength in the US labor market. Non-farm payrolls returned to trend in March with 196,000 new positions, relegating February’s 33,000 total to the occasional and unimportant category. Wages improved 3.2% on the year, just 0.2% below their decade high in February. April’s report, due on Friday, is expected to continue with 180,000 new jobs.

Reuters

Fed Economic Projections

The Fed’s GDP assessment in the March Projection Materials which proposes 2.1% this year, down from 2.3% now looks somewhat pessimistic.

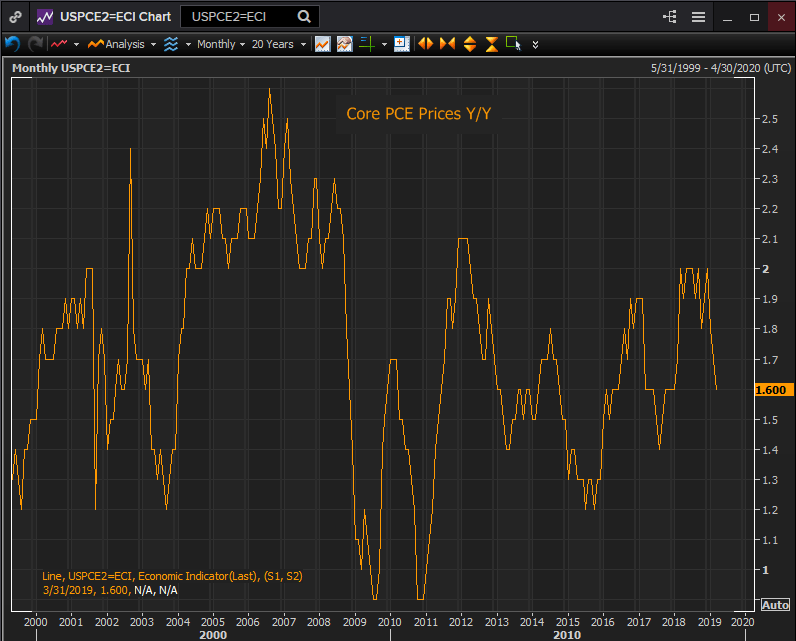

On the other hand the core PCE inflation estimate, 2.0% in 2019, appears optimistic. The core PCE annual rate in March was 1.6%. What is concerning from the governors’ point of view is the swift change in direction this year.

Reuters

Inflation had finally reached its long sought target of 2% in 2018. From March through December the annual rate hit the target in six of ten months, in three months the rate was 1.9% and in one 1.8%. Yet in a quarter with robust 3.2% growth and wage increases averaging 3.27% core prices fell 0.4%.

Fed Policy Redux

The central bank’s twin mandates of employment and price stability are a balancing act. In standard economics the tradeoff is between faster growth and inflation. Interest rates are the regulator, slowing down growth if the bank judges it is fomenting inflation and prompting or supporting economic activity if growth recedes. The assumption being that rapid economic growth eventually brings on inflation.

That notion, that the monetary tool can be used to control inflation, has been questioned, empirically if not theoretically since the financial crisis. The world’s central banks have been in the unusual situation of applying liquidity to their economies to support growth but finding that even when growth responded inflation did not.

The decline in the core PCE rate of 0.4% in three months when the US economy is expanding at 3.2% and wages are rising, is mild disinflation. It is not the deflation that central bankers so abjure. But is more than a curiosity. Since weak or declining inflation has been the peculiar and recurring problem of the post-financial crisis global economy it is a subject the Fed will not ignore.

One of the stated goals of the Fed’s quantitative easing was to bring inflation to 2%. But no sooner was the goal achieved than it has begun to slip away.

With US economic growth, at least for the moment, not a problem, inflation, or its absence will become the Fed’ interest. Will the Fed governors contemplate cutting interest rates to spur inflation when economic growth does not warrant such intervention?

If the current relationship between economic growth and inflation is weak or even nonexistent has the ability to affect one by manipulating the other become a modern version of the mathematical puzzle from antiquity of squaring the circle. It proved impossible to use geometry to create a square and a circle of equal area. Has inflation targeting become the problem?

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.