Fed Preview: Market Moving Policy?

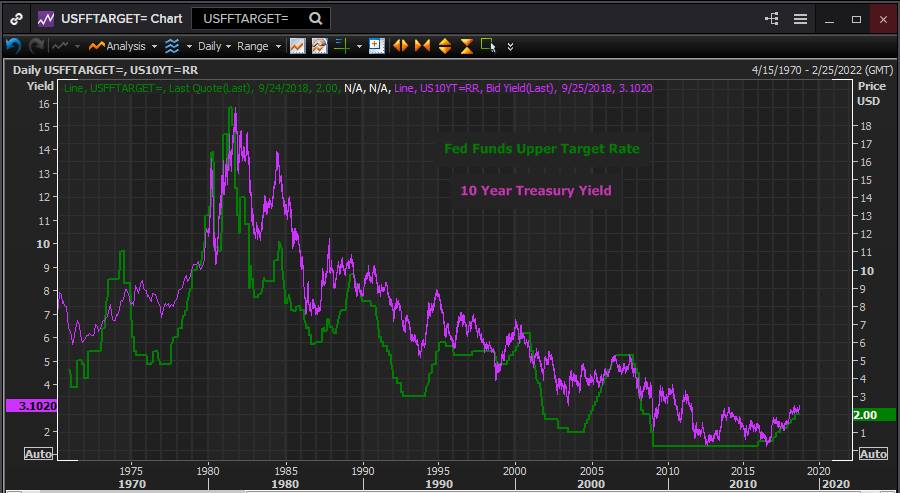

- The Federal Reserve will raise the Fed Funds upper target rate 25 basis points on September 26th, bringing the rate to 2.25 percent. It will be the third hike this year.

- This increase and to a large degree one in December are priced into currency levels

- With the Fed Funds and core inflation roughly equal Fed policy is neutral

- Market attention will be on the Fed’s prediction for 2019

FOMC

Wednesday’s Federal Open Market Committee (FOMC) vote to increase the Fed Funds target rate 0.25 percent is as near a certainty as is possible. The governors and Chairman Powell have been firm in their policy guidance, the economy is growing smartly, jobs are plentiful and wages are rising. With the core PCE index, the Fed’s preferred gauge, at 2 percent in August and a 1.9 percent average over the last six months rate policy is no longer accommodative. The statement will be parsed for any change in the inflation assessment from August 1st, “On a 12-month basis, both overall inflation and inflation for items other than food and energy remain near 2 percent. Indicators of longer-term inflation expectations are little changed, on balance”.

Future Policy

The most important question is the course of Fed policy in 2019. The economy seems to have moved into a higher growth pattern, 4.2 percent in the second quarter and a current GDPNow Atlanta Fed estimate of 4.4 percent in the third. The labor market is robust.

The key question is inflation, wages included. Core PCE price changes have climbed from 1.4 percent last August to 2 percent last month. Headline PCE was 2.3 percent in August and 1.5 percent last August. The Fed had been seeking exactly this result and wage increases for much of the past six years. Now that it has arrived will the governors take it a sign of a healthy economy and success at finally leaving the legacy of the financial crisis behind and let the economy run? Or will the recent acceleration excite fears that the economy and inflation are moving too fast? Informing the Fed’s considerations will be the dual questions of what is the correct level for the Fed Funds rate after the extraordinary exertions of the last decade and the long term decline in interest rates and inflation.

Projection Materials

At the last issuance of its economic projections in June the Fed’s economists increased the 2018 GDP estimate to 2.8 percent from 2.7 percent, lowered the unemployment projection to 3.6 percent from 3.8 percent and raised core PCE to 2.0 percent from 1.9 percent. The ‘forecast’ for the Fed Funds target also went to 2.4 percent from 2.1 percent in March. Both equate to one more rate increase this year, to 2.5 percent in December.

The Fed has been at pains to point out that these materials are not forecasts but just the consensus of internal estimates. Nonetheless markets tend to treat them as Fed forecasts.

U.S. GDP is currently running at 3.7 percent for the year, including the Atlanta Fed estimate for Q3. It will be interesting to see how far the new Fed estimate recognizes this. At the last release on June 13th second quarter numbers were not available.

The projection for the Fed Funds rate in 2019 in the June materials was 3.1 percent, up from 2.9 percent. That increase implied one additional 0.25 percent increase next year, bringing the total to three. Assuming the rate will be 2.5 percent after the December meeting, three increases would be needed, adding 0.75 percent, to bring the rate to 3.25 percent at the end of next year, encompassing the 3.1 percent projection. This estimate of what the Fed calls the “projected appropriate policy path” will be the most important piece of information in tomorrow’s statement and materials. If it rises so will the dollar.

Charts: Reuters Eikon

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.