Fed minutes help safe havens again with Jackson Hole eyed

Market Overview

The minutes of the July meeting of the Federal Open Markets Committee (FOMC) have given markets pause for thought over how aggressive a cate cutting cycle might be from the Fed. The FOMC minutes reflected a split on the committee over the path of rate cuts. Some members calling for 50 basis points of cut, some calling for no cuts at all. However, broadly the message is that the cut was a “mid-cycle adjustment” and not the start of a significant cutting cycle. Now, of course, the Fed meeting came before Donald Trump threw the cat amongst the pigeons once more and re-ignited the trade dispute. The Fed is very mindful of how the global slowdown could infect the US economy. So in effect the minutes could quickly be usurped by Jerome Powell’s key note speech at the Jackson Hole Economic Symposium on Friday. The reaction on markets has been interesting, especially on Treasuries. The 10 year yield barely budged, but the 2 year yield jumped, to an extent that the 2s/10s spread is close to inversion once more. This flattening suggests that the market is questioning whether the Fed is doing enough to prevent potential slowdown turning into a recession. There has been a marginal dollar strengthening on a safe haven bias, with the yen gaining ground again. This has weighed slightly on equities too. So, once any volatility from today’s flash PMIs is digested, the focus will be squarely on Fed chair Powell.

Wall Street closed higher with the S&P 500 +0.8% higher at 2924, however, US futures have rolled back slightly this morning by -0.2%. This has seen Asian markets mixed to slightly weaker (Nikkei -1 tick, Shanghai Composite -0.2%), whilst European markets are edging slightly lower too (FTSE futures -0.2% with DAX futures -0.3%). In forex, there is a mild edge of USD gains, but JPY continues to perform well. In commodities, gold is consolidating with a mild negative bias, whilst oil has dropped mildly too.

The first look at growth for August comes as the flash PMIs for the Eurozone and US are in focus on the economic calendar today. The early European session is dominated by a string of country releases, but the Eurozone-wide data is at 0900BST. Eurozone flash Manufacturing PMI is expected to slip back to 46.2 (from a final reading of 46.5 in July) and continue its sharp decline, whilst Eurozone Flash Services PMI is expected to also slip back but remain in expansion at 53.0 (down from a final reading of 53.2). This would be a drag on the Eurozone Flash Composite PMI which is expected to fall to 51.2 in August (down from 51.5 in July) which would suggest that Q3 Eurozone growth remains stagnant. In the afternoon the US Flash PMIs are at 1445BST. US Flash Manufacturing PMI is expected to hold up in marginal expansion with 50.5 (up from a final 50.4 in July) however, US Flash Services PMI are expected to slip slightly to 52.8 (from 53.0). It will also be interesting to watch the Eurozone Consumer Confidence at 1500BST, which although is expected to drop back slightly to -7.0 (from -6.6) has shown signs of stabilizing in recent months having bottomed at -7.9 earlier in the year.

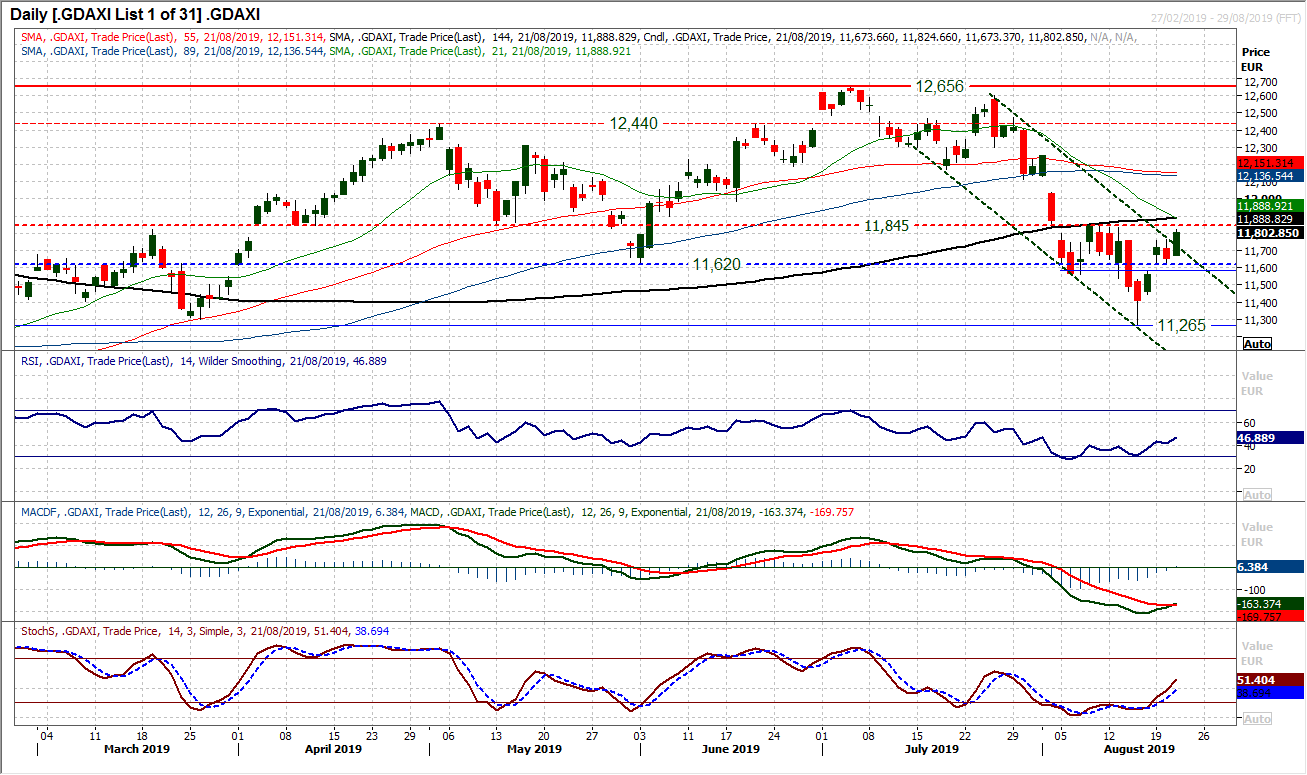

Chart of the Day – DAX Xetra

The DAX has been volatile in the past couple of weeks, with a series of bull and bear moves, however, are we starting to see signs of recovery forming? This comes after yesterday’s strong positive candle which with a two week closing high, puts pressure on the key resistance at 11,845/11,865 once more. Importantly, the support of the key low at 11,620 has held throughout this week, but there now seems to be a move being dragged higher by improving momentum. Stochastics are advancing following a bull cross, whilst MACD lines are also threatening to cross higher, with RSI at a three week high. A move on RSI above 50 would really suggest the bulls are gathering a head of steam. However, it is important not to pre-empt a breakout on a market which has been so negative in the past month. Futures are ticking mildly lower early today which suggests the bulls will need to work hard for the breakout, however, a close at a two week high is encouraging. A close above 11,865 would suggest a change of trend and a recovery formation. It would mean that the 11,620 support grows in importance too for the bulls to build from. Initial resistance above 11,865 is at 12,035 and then 12,115.

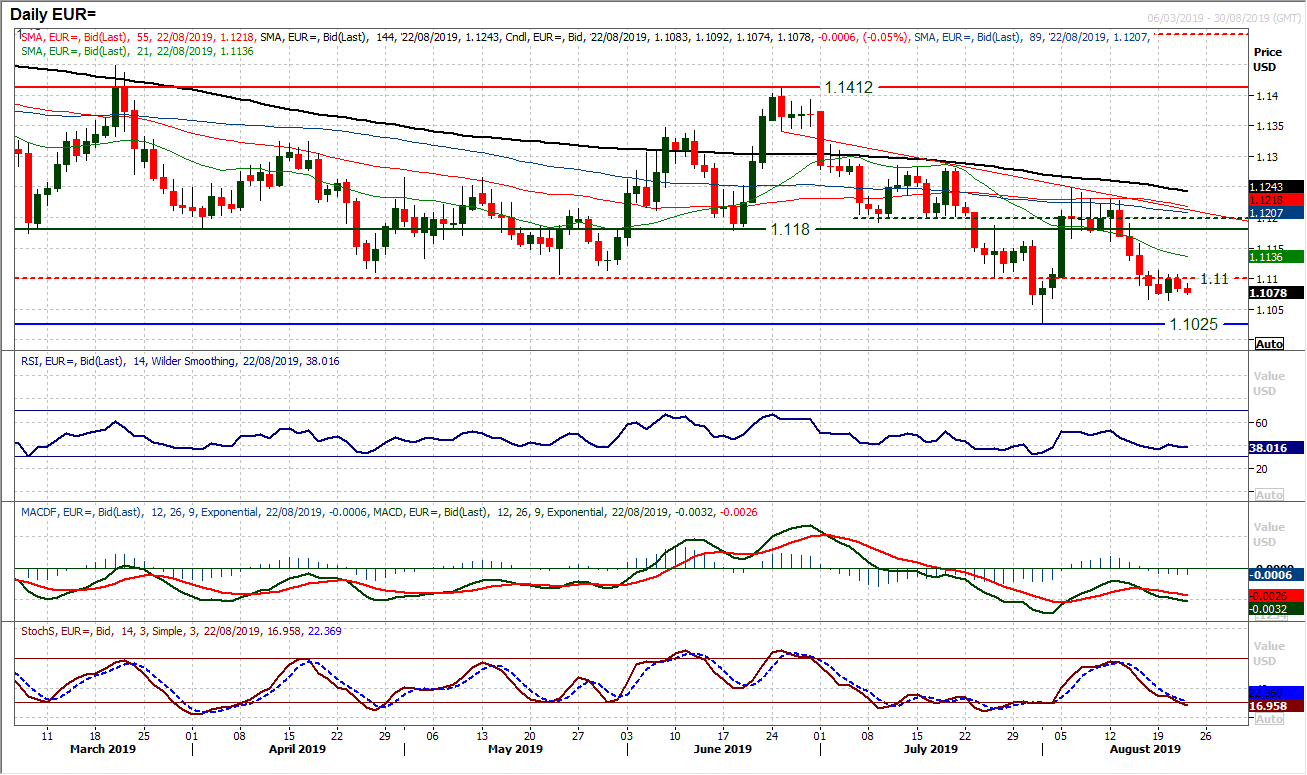

EUR/USD

The selling pressure may have eased slightly in the past couple of sessions, however there is still a lack of recovery traction. The Fed minutes last night pulled mild strength through the dollar and dragged EUR/USD back from $1.1100 once more. The move seems to be bolstering the initial resistance of $1.1100/$1.1120 overhead and has added a marginal negative bias into today’s session. We believe this is fairly well reflective of EUR/USD across a medium term basis too. The outlook for edging lower without decisive selling pressure. Rallies continue to be restricted and pressure on supports will continue. Momentum indicators are subdued with RSI holding around 40, MACD lines relatively stable but well below neutral and Stochastics drifting lower. Subsequently, the near term low at $1.1065 is being eyed this morning, a breach of which opens $1.1025 key support. Hourly indicators point to a negative bias, but also be mindful that the hourly RSI is showing a ranging outlook and we do not expect any trending move to take hold at least until Jerome Powell’s Jackson Hole testimony on Friday.

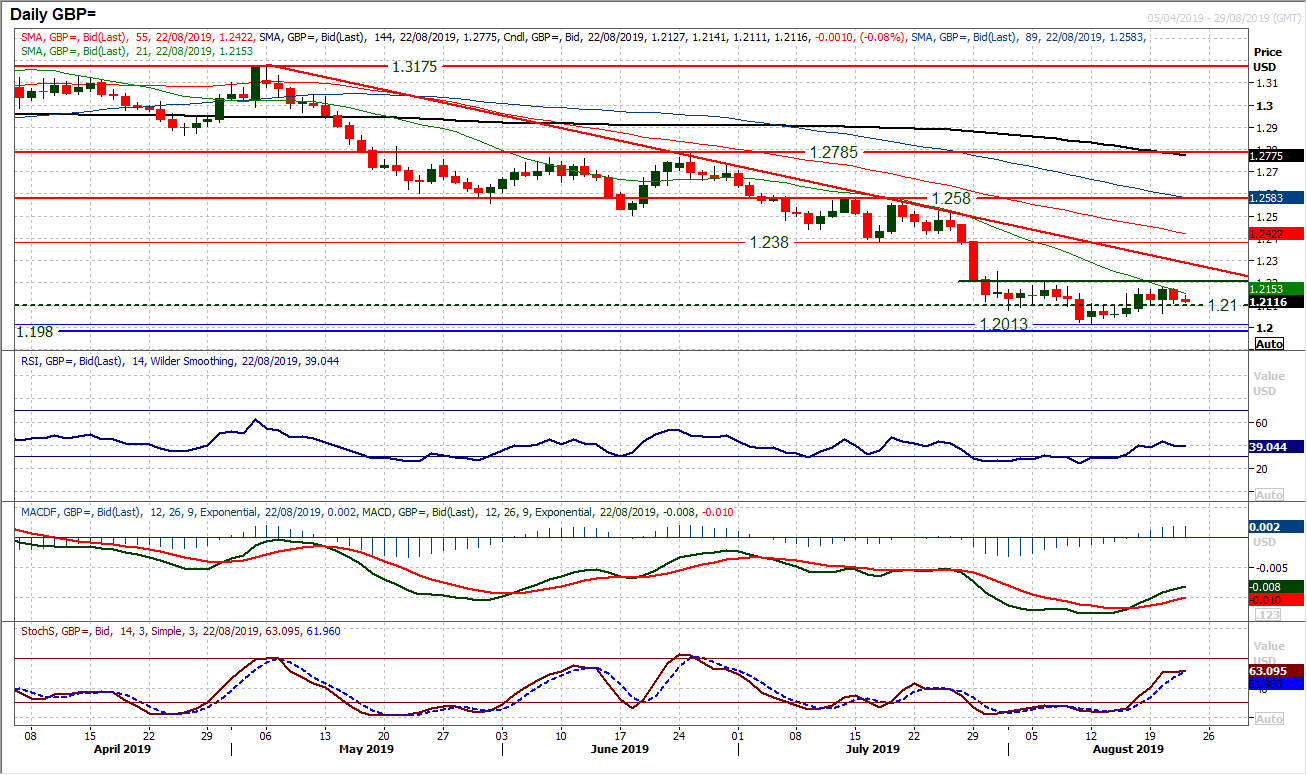

GBP/USD

The near to medium term outlook on Cable is increasingly rangebound. This week we have seen an array of contradictory candles that have restricted the near term recovery to under the resistance $1.2210/$1.2250. Additionally though there seems to be a basis of support which is also forming between the recent low around $1.2015 and $1.2065. There has been a moderation of momentum indicators with the RSI around 40 whilst unwinding improvements on MACD and Stochastics are tailing off now. We continue to focus on the 21 day moving average as a basis of resistance, currently falling around $1.2150. A close back under $1.2100 (which has been something of a near term pivot) would add a negative bias to this consolidation, but for now, this is a market looking for signals. The hourly indicators are very much ranging in configuration.

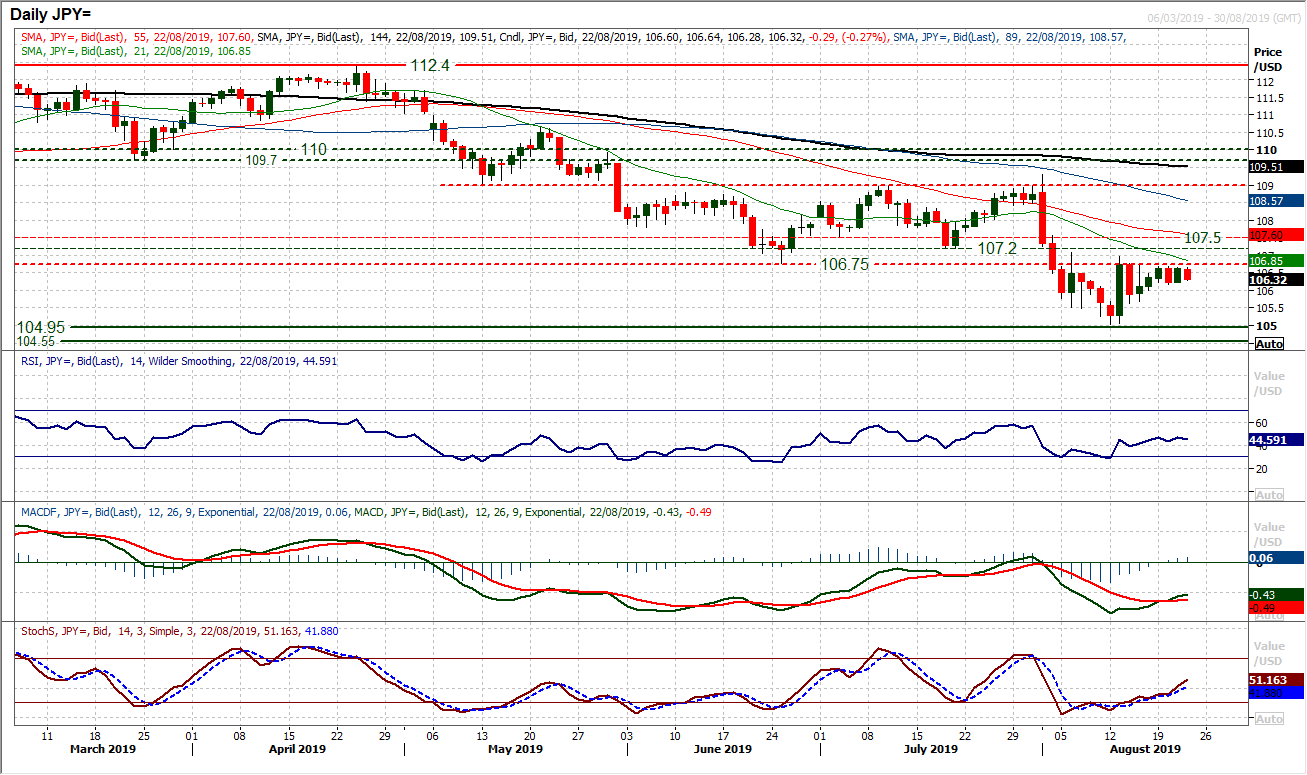

USD/JPY

A sense of consolidation has taken hold in recent days with the resistance consistently forming under the old key low at 106.75. This remains an important barrier to gains, playing out as the bottom of the overhead supply band 106.75/107.50. Another intraday pull higher yesterday appeared to run out of steam once more under the resistance as the bulls seem unwilling to take a view (probably ahead of Powell’s Jackson Hole speech on Friday). The lack of conviction in the unwinding move higher on momentum suggests that this is consolidation rather than a call for a decisive recovery). This is reflected in the lack of direction coming through on the hourly chart as the hourly RSI oscillates between 35/65 and the hourly MACD lines hover around neutral. Initial support at 106.15 with 105.65 key to protecting the 105.00 low.

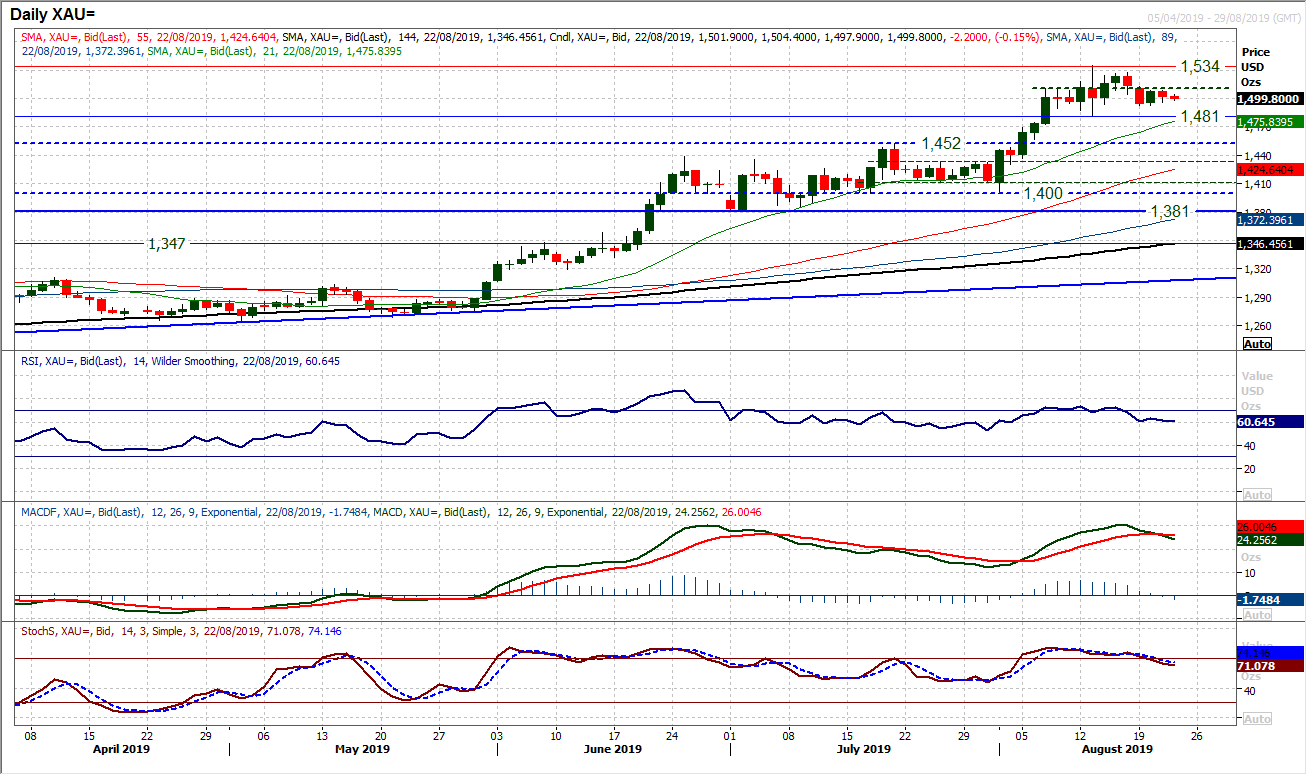

Gold

The consolidation on gold between $1481/$1534 continues with traders happy to keep their powder dry for now. There is a mid-range pivot around $1510 which is a gauge for positive or negative intent within the range. So trading marginally below $1510 means there is a mild negative bias for now. This comes with the slight near term negative drift on MACD and Stochastics, but there is little to really be overly concern with whilst the initial support at $1492 protects $1481. Although the risk would be a small top pattern completing below $1481 (which would imply around $50 of correction), we remain buyers into weakness on gold and a breakdown is not our base case scenario. The hourly chart momentum indicators continues to reflect a range play for now, with the hourly RSI oscillating between 30/70 and continued protection of support at $1492 yesterday. It is likely that the market is in wait and see mode until Jerome Powell’s Jackson Hole speech.

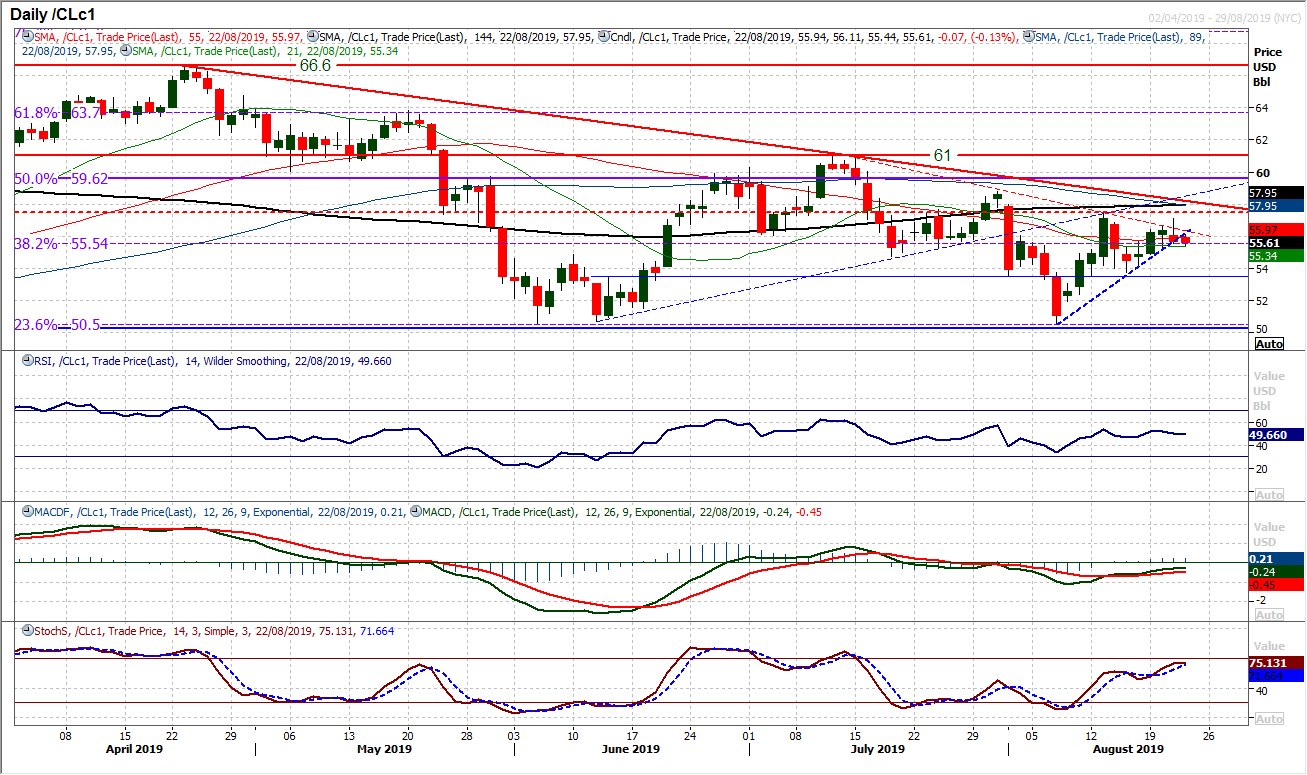

WTI Oil

A bearish “shooting star” candlestick (albeit a small one) is a one day reversal signal and is a warning sign that the market may once more be setting up for renewed weakness. There has been a downtrend of the past five weeks which was intraday breached yesterday by early gains, but the market did not find much solace in either the EIA crude inventory drawdown or the Fed minutes. Selling into the close and the market is creeping lower again today. WTI may have been in recovery mode near term but has been trending lower across several other time horizons. So with the momentum indicators never really getting going into positive configuration, the risk is that this rebound has been a bear market rally and that selling pressure is never too far away. A failure at $57.15 bolsters resistance of the lower August high at $57.50. A close back under the 38.2% Fib at $55.55 would be a bull concern whilst under $55.30 breaches a run of higher lows. Support at $53.75 protects retest of the key low at $50.50.

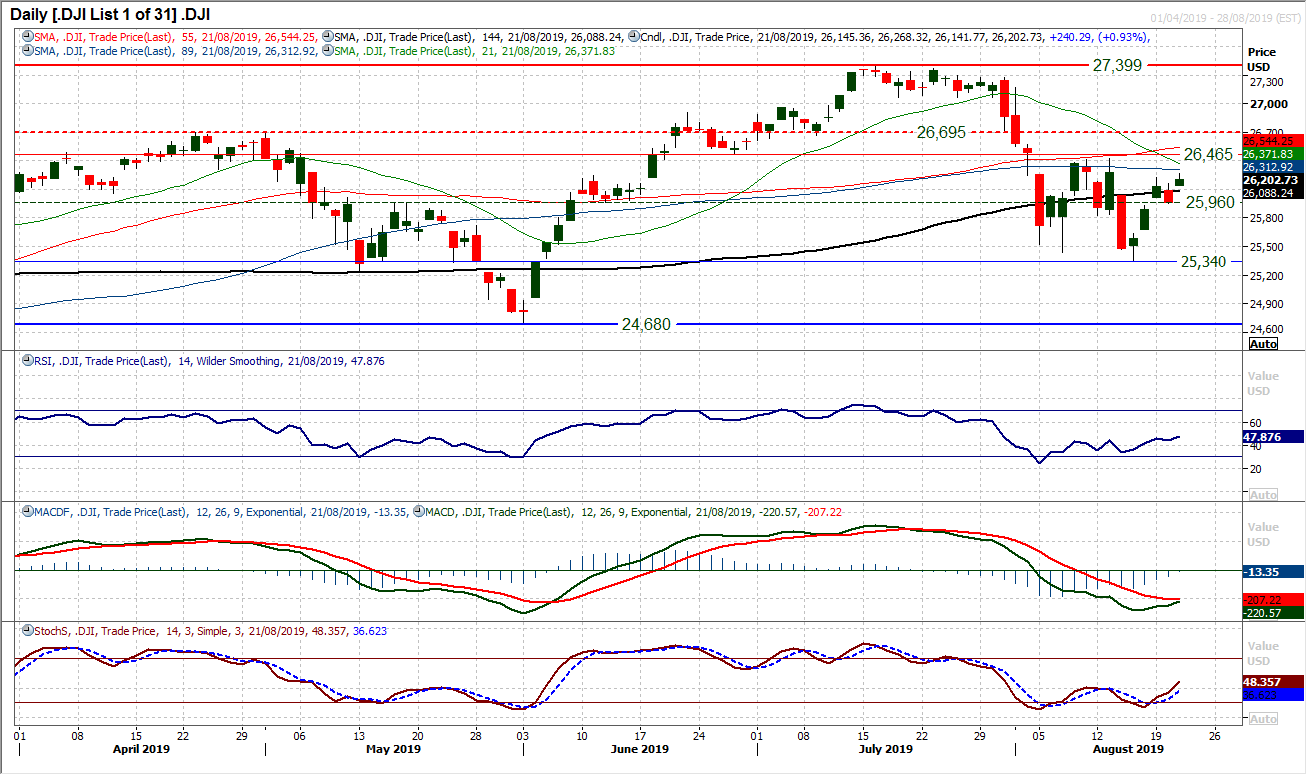

Dow Jones Industrial Average

The bulls reacted positively yesterday to the disappointment of Tuesday’s negative candle. However, as the market initially found strength early in the session, the Fed minutes have just added an element of caution back into the market. There is still a clutch of positive momentum signals bubbling under the surface, but this remains a market being held back. The RSI rising at three week high, but under 50 still is a reflection of this. The MACD lines are threatening a positive cross, whilst the Stochastics are edging higher but also still below 50. In essence the key to the outlook remains the 26,425/26,465 resistance band that has held the Dow back for much of August. If this can be overcome then the bulls will be advancing well. Another failure would re-emphasise the range 25,340/26,425 and keep the shackles firmly on a recovery. The hourly chart indicator reflect the near term positive bias but within a ranging outlook.

Author

Richard Perry

Independent Analyst