Fed lowers rate and hints at further easing this year

Fed cuts by expected 25 bps, projects two more cuts this year

Following a five-meeting pause – and the first cut since embarking on aggressive policy tightening in 2022 – the Fed lowered the target rate by 25 bps to 4.00% - 4.25% yesterday. The decision was mainly bolstered by growing concerns of a deteriorating labour market, with the Fed noting that unemployment has ‘edged up’ and ‘downside risks to employment have risen’.

Stocks and Gold initially popped higher following the announcement, with the USD and yields taking a leg lower. Moves were short-lived, with said markets recouping lost ground in a reasonably quick fashion. However, the USD Index was a notable winner on the day, strengthening against a basket of six major currencies and snapping a two-day winning streak. US Treasury yields also bear flattened, though remained within established ranges.

One dissenter

There was one dissenter in the ranks: the newly sworn-in Fed Governor Stephen Miran, who opted for a bulkier 50-bp cut. I thought there would be more dissenters, to be honest, with a couple voting to hold things unchanged.

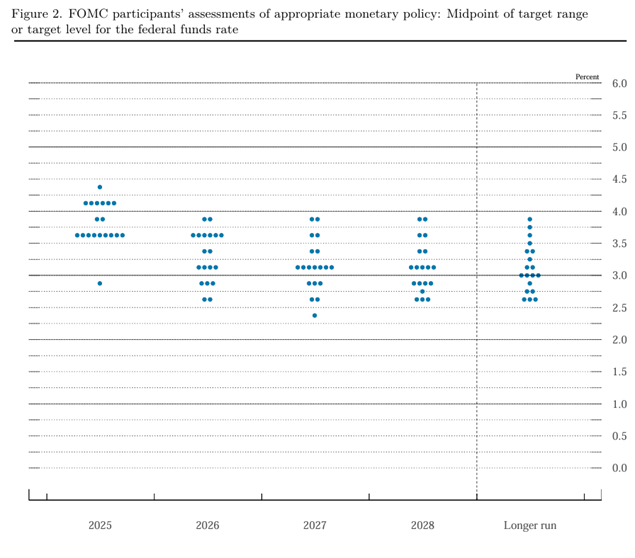

As shown below, the spread of the Fed’s dot-plot projections was quite telling, with a rather ‘lonely’ sub-3.0% this year. The dots are anonymous, but I think most have a pretty good idea who this might be. Fed officials also updated their projections to include an additional 50 bps worth of cuts this year, which is more than initially forecast in June, and signals a shift in focus from inflation concerns toward employment. This also aligns with market pricing, which currently implies 44 bps of easing by year-end.

The distribution of the dots for 2026 was also quite a picture, suggesting that Fed officials have little idea what next year holds. Let’s be frank, we all have our theories and models, but no one knows what next year brings.

Upgrade to growth, inflation expected to remain elevated

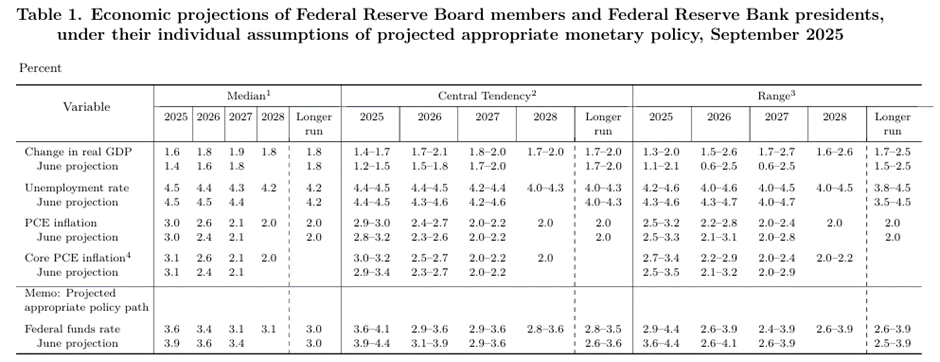

As displayed below, you will see that while US GDP was revised higher to 1.6% this year (from 1.4%), the Fed expects unemployment to remain unchanged at 4.5%, and inflation is expected to hold at 3.0% for the PCE and 3.1% for core PCE.

So, all in all, we have an upgrade to growth, along with inflation expected to remain elevated, but the Fed will cut rates by more this year?

Projections show that inflation is expected to remain above 2.0% until 2028, which is something reporters pressed Powell on, and whether this target is actually achievable given the Fed's expectation that inflationary pressures will remain elevated in the near term. This creates an uncomfortable dynamic of cutting rates while inflation remains above target, highlighting the challenge of balancing the dual mandate objectives.

You will also note that there is somewhat of a disconnect between what the Fed projects for 2026 – just one rate cut – and market pricing, which implies two rate cuts to 3.00% - 3.25%. This divergence suggests that investors will need to realign their expectations to factor in just one rate cut next year, which could weigh on risk assets, or the economic landscape will need to deteriorate sufficiently for the Fed to ease policy by more-than-initially projected. The USD’s modest strength yesterday may represent the beginning of a broader revaluation if the Fed's policy proves less accommodative than expected.

Powell’s presser

Despite the rate cut and subsequent policy easing priced in, Fed Chairman Jerome Powell emphasised the central bank’s meeting-by-meeting stance. It is also worth highlighting that Powell stressed that yesterday’s policy move was a ‘risk management cut’, noting that the situation has changed because of the labour market.

Regarding talks of a 50-bp cut, Powell said that limited support for such a move was seen among policymakers, despite the outlier.

BoE rate announcement in focus today

The BoE will take some of the limelight today at 11:00 am GMT, with the central bank widely anticipated to keep its bank rate on hold at 4.00% (98% probability). This is expected to be delivered in the form of a 7-2 MPC vote split, following the narrow 5-4 decision on the last meeting's rate cut. There is also likely to be a slowdown in Gilt sales, from £100 billion to £67.5 billion annually.

Heading into the event, inflation remains elevated – the August print revealed headline YY inflation remained at 3.8%, which is nearly double the BoE’s inflation target, while YY core inflation slowed to 3.6% from 3.8%. Alongside this, economic activity remains fragile, with the July reading flatlining, as well as wage growth moderating slightly to 4.8% from 5.0% (regular pay).

The BoE faces similar dual mandate tensions as the Fed, though with less dovish expectations, which could open the door for hawkish surprises. Therefore, any form of hawkish rhetoric from the BoE today could firm up bids for the GBP. An interesting chart I am watching closely right now is the GBP/JPY. As shown below, the cross recently breached a 1M resistance level at ¥200.15 and demonstrates scope to approach as far north as a 1Y resistance level of ¥203.24.

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,