Fed Chief Powell is becoming cowardly

Outlook

Yesterday Goldman published a note saying the Trump tariffs will raise inflation and unemployment, and drag growth nearly to a standstill. The inflation forecast for this year is 3.5%, unemployment to 4.5%, and GDP a mere 1%. “We continue to believe the risk from April 2 tariffs is greater than many market participants have previously assumed.”

The probability of a recession in the next year is now 35% (from 20%). Finally, Goldman now expects three rate cuts this year, in July, Sept and Nov.

The final University of Michigan consumer sentiment survey has inflation out one year at a whopping 5%, up from 4.3% in Feb. Since headline PCE is 2.5%, that means a doubling of inflation. The headline reading of 57.0 is down 11.9% from Feb and down an amazing 28.2% from a year ago. It’s the third drop and covered all party lines. The American consumer is not as stupid as politicians think.

Or the Fed. Fed chief Powell is becoming cowardly. Last week he said of inflation "there may be a delay in further progress over the course of this year." This is seen as downplaying the tariff effect. It was also taken as a hint the Fed will postpone rate cuts. We are not so sure. Trump wants rate cuts and the swift trip toward recession is a dandy excuse.

The Trump administration is one outage after another—grabbing foreign students off the streets and imprisoning them with no due process, Musk paying for votes in an election in the Midwest (definitely illegal), etc. So far the courts are mostly ruling against Trump but that doesn’t bother—or stop—him. This can only get worse.

Forecast

For forecasting purposes, too much depends on the verbal garbage spilling out of the White House. As noted on Friday, Trump rhetoric is now on a par with actual macro data (if it quacks like a duck). US yields “should” be moving down by more than they are, and the dollar “should” be weaker as the US is now fully the Bad Guy on the stage. It’s likely that Trump will pull in his horns in the next few days and pretend he was only “negotiating,” the equivalent of the 4-year old yelling and stamping his feet. This could give the dollar some relief. So don’t bet the ranch.

Tidbit about Gold: The importation of physical gold from London has been so massive that it screwed up the trade figures, something the Atlanta Fed somewhat belatedly acknowledged.

We recently saw a forecast of $4000/oz. Is that realistic on any planet? Well, maybe. The easy idea is that tariffs are going to trigger inflation. Another is that just about every country has high and growing deficits, implying a future contraction that will damage growth. The worst idea is that a full-bore trade war could trigger a global recession. This is shades of the 1930’s and Roosevelt grabbing all private gold by Executive Order 6102 in 1933. (Gee, who do we know who likes executive orders and never mind that order was repealed in 1974… he can always invent a new one).

ECR Research talks about these issues and concludes “The strong rise in gold is also driven by the fact that many central banks and sovereign wealth funds are growing increasingly wary of holding large sums in the U.S. or Europe. In the event of a tariff war escalation, there are fears that the current U.S. administration could freeze or even confiscate foreign assets. This makes gold a particularly attractive alternative, since it can be stored domestically.”

Food for Thought: Here is an issue that is not going away and of immense interest to FX: will foreigners keep buying Treasuries (and the dollar)?

It start with this:

As long as the US dollar remains the world’s key international currency, the convenience yield of holding dollar-denominated assets will likely forestall a large-scale sell-off. But this stability hinges on one crucial assumption: that US institutions remain strong and credible enough to preserve confidence in Treasuries.

The essayists say “… cracks are beginning to show. Between September 2024 and January of this year, interest rates on ten-year Treasuries climbed by 100 basis points, even as the US Federal Reserve cut short-term interest rates by the same amount. The economists Rashad Ahmed and Alessandro Rebucci attribute these developments – which they call a “reverse conundrum” – to declining foreign official demand for dollar-denominated safe assets, driven by rising concerns over US sanctions and asset freezes.

China in particular is diversifying. “Bottom of Form

Europe is quietly picking up some of the slack. UK holdings of US Treasuries – which totaled just $207 billion a decade ago – have more than tripled, reaching around $740 billion at the start of 2025. Likewise, EU countries’ holdings grew from $931 billion to over $1.5 trillion over the same period. Most of this increase in demand likely comes from private investors seeking higher yields.

“… If global investors abandon US sovereign debt altogether, the dollar’s status as the world’s leading reserve currency would be in jeopardy (though the currency might still be used for international trade transactions). … As the dollar appreciates and Treasury yields rise, the opportunity costs of holding Treasuries falls, making them more appealing to investors.

“In other words, reductions of countries’ Treasury holdings are subject to a self-correcting dynamic, which limits the scale of any sell-off. This means that foreign investors are more likely to adjust their holdings gradually, rather than rush for the exit. So, while foreign holdings of US Treasuries may well decline, fears of an imminent collapse in demand for US Treasuries are probably not warranted.

“… As long as the US dollar remains the world’s dominant international currency – facilitating trade and cross-border financial flows and serving as countries’ main reserve asset – the convenience yield of holding dollar-denominated assets will likely forestall a large-scale sell-off. But this stability presupposes that US institutions remain strong and credible enough to preserve confidence in Treasuries. At a time of sharply rising political and institutional uncertainty, this is hardly a foregone conclusion.”

The departure of foreign buyers from Treasuries will be a long, drawn-out process, assuming it happens at all. We can’t expect to see it after only two months in office of a new president. Okay, how many months? We will pick nine, to year-end. Even then, it will be only a minor start.

That’s because of the US superiority in sheer size, variety, depth, liquidity and global acceptance. Those things are not being challenged by any other country or group to any significant extent. The EU doesn’t even have a joint eurodollar bond market to speak of. It has a bond market—denominated mostly in dollars. It’s not just merchants preferring the dollar—it’s also reserve managers with no hard alternatives. Everyone may be repelled by Trump and his insulting bullying, but dumping the dollar—sometimes named de-dollarization--is not realistic. Yet. It would take a triggering event to get that ball rolling, like ending the international swap lines we wrote about last week, or a series of such events. It reminds one of the kings who squandered Spain’s wealth and hegemony, starting with Philip II and later, Charles IV. Good thing we don’t have a king.

Tidbit: The usually perspicacious Bloomberg editor Tracy Alloway doesn’t much like FX. On Friday she wrote “As mentioned previously in this space, currency volatility has remained pretty low in the face of all these headlines and big potential global changes. You can see just how low in the below chart, showing JPMorgan’s Global FX Volatility Index. Currencies have remained relatively quiet even as bonds have been moving around. That’s weird too.”

We looked high and low for that index. We do that periodically. We never find it. What we do find is VXY, “a volatility-weighted index of three-month ATM options of the exchange rate of the G7 currencies against the US dollar. This index was developed by JP Morgan in 2006 to monitor currency volatility.” That’s about all you find before plunging down the rabbit hole of electrical intricacies and music. VXY seems to be quite exotic and nobody writes about it, nor relies on it for gleanings of what’s ahead.

We say the VXY index is worthless to the strategic day-trader. For one thing, it’s options, and it is well established that past vol is a lousy predicter of future volatility. For another, G7 is the wrong set. It excludes Australia and Switzerland (does contain Canada, UK, France, Japan, the UK and US)-- but does include Italy. We adore Italy for a thousand reasons, but Italy doesn’t have a different currency from France and Germany.

That means the index is really the pound, the Cad and the euro. Why don’t they say that instead of the misleading but important-sounding “G7”? Even the euro is problematic, because it waxes and wanes separately against the pound, CHF and yen.

So, bottom line, the VXY is not a reliable or accurate indicator of “currency volatility.” Ignore the chart safely.

Bloomberg also has a set of volatility indices that are not available on our subscription. As far as we can tell, the vol is based heavily on forward premium/discount and other metrics. These are supposed to lead to “insights.” Maybe they do, but the cost is prohibitive, and we’d really like to see a track record…

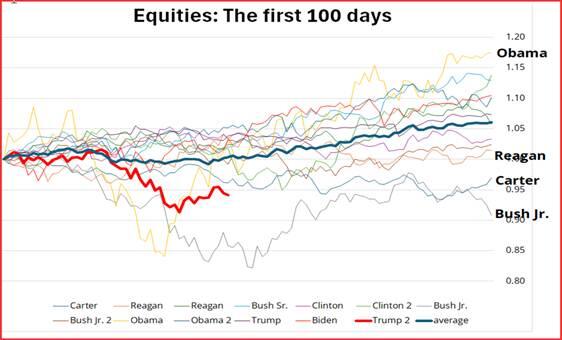

Tidbit: The stock market is not the economy. But see the chart from Brent Donnelly’s “Speedrun.” Donnelly also points to bonds doing nothing much and pointing out “It’s hard to have a strong view on bond yields when prices are sticky/rising and economic growth is about to dump.”

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat