Fed Chair Powell speech offers dovish vibe – PCE data in focus

Last week culminated in what was a widely anticipated speech by US Federal Reserve (Fed) Chairman Jerome Powell at the Jackson Hole Symposium. The week leading up to Powell’s address was mixed in terms of whether he would stand pat on his wait-and-see stance – which was somewhat reflected in commentary from Fed officials and rate pricing – or unearth a more determined dovish approach.

Powell struck more of a dovish ‘tone’ in his speech and signalled a potential rate cut as early as next month, but with some caveats. While largely emphasising that the jobs market is softening, he countered by warning that inflation risks remain tilted to the upside and that US President Donald Trump’s tariffs could spur lasting inflation. To directly quote Powell, this positions the Fed in a ‘challenging situation’.

Powell highlighted the unusual dynamics in the current labour market, describing it as displaying ‘a curious kind of balance’, resulting from a marked slowing in both worker supply and demand. He warned that ‘downside risks to employment are rising’ and emphasised that if these risks materialise, ‘they can do so quickly in the form of sharply higher layoffs and rising unemployment’. This focus on employment concerns marked a notable shift from the Fed's recent emphasis on inflation risks.

However, Powell also noted: ‘With policy in restrictive territory, the baseline outlook and the shifting balance of risks may warrant adjusting our policy stance’. Along with the comments about employment/inflation risks, this was a key part of his speech and was largely what the market focussed on. Yet again, though, he cautioned that the Fed would ‘proceed carefully’ given the stability of the unemployment rate and other labour market measures.

So, while – at least in the near term – things have taken a dovish twist, the river ahead appears far from being ripple-free.

It is important to note that we still have one more CPI inflation (Consumer Price Index) and jobs print to tackle before the next Fed meeting, which could complicate the picture. We also have PCE inflation data (Personal Consumption Expenditures) out this week, which I touch on below.

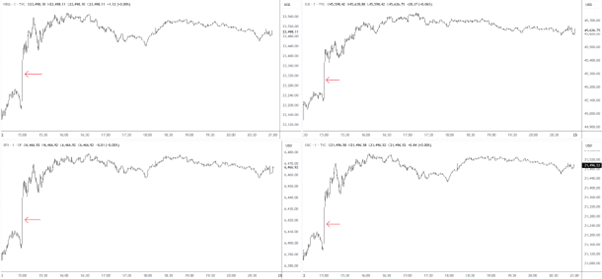

The speech sent the US dollar (USD) and US Treasury yields southbound, with Stocks catching a notable bid, as shown below. Interestingly, during his speech, investors all but fully priced in that the Fed would lower the target rate by 25-basis-points (bps) at September’s meeting. However, at the close of trading, market pricing has since retreated to 20 bps. Coupled with persistent inflation as well as rate-cut expectations, US Treasury yields bull steepened, with shorter-dated yields down almost 10 bps at the close of trading on Friday.

The US economic picture is a mixed bag

The timing of Powell's remarks follows the disappointing US July payrolls report, with May and June job totals reduced by a combined 258,000 positions.

The advance Q2 25 real GDP (Gross Domestic Product) reading revealed the US economy expanded at a 3.0% annualised pace; of note, we have the preliminary estimate out this week, which is forecast to show the economy grew by 3.1% (the estimate range spans between a high of 3.4% and a low of 2.9%).

On the inflation front, the July consumer price pressures were relatively tame, offering no nasty surprises. YY headline CPI inflation held steady at 2.7% in July, coming in just below the anticipated 2.8%. YY core CPI, which excludes volatile food and energy costs, accelerated to 3.1% YY, modestly surpassing both the 3.0% consensus forecast and June's 2.9% rate. This is considerably higher than the Fed’s 2.0% inflation target.

The July PPI inflation report (Producer Price Index), however, echoed a different vibe. Both the YY headline and core measures exceeded projections, with headline PPI jumping to 3.3% from 2.4% the previous month, while the core reading climbed to 3.7% from 2.6%. This is important, as higher prices on the wholesale side generally mean that these price increases will be passed down to the end consumer.

Is it now just a matter of time before we see further rises in inflation? I think so. But, like Powell noted during his speech, there was a reasonable case to be made that inflation would be ‘relatively short-lived – a one-time shift in the price level’. Time will tell how that plays out. The point is, inflation is rising right now, and the labour market is softening, in turn placing the Fed between a rock and a hard place.

You will recall that the latest Fed minutes underscored some division among the ranks at the central bank, with one camp forecasting a short-lived impact from tariffs; the other side, however, is cautious and is uncertain regarding the impact of tariffs on price pressures.

PCE data in focus

The perceived Fed pivot comes ahead of the July PCE data on Friday, which is what the Fed uses to target inflation, and the second estimate of Q2 GDP numbers this week on Thursday and Friday, respectively.

Expectations heading into the events show the YY headline PCE price index is forecast to rise by 2.6%, matching June’s reading, while core YY PCE is anticipated to rise by 2.9%, up from 2.8%. As for the Q2 GDP number, economists are expecting a modest uptick in output to 3.1%, up from 3.0%.

Following Powell’s speech, I believe the market will be closely watching the two noted reports to help validate the dovish Fed expectations.

Were PCE inflation to show a marked increase, this could call into question September’s Fed rate cut and consequently prompt investors to trim rate cut bets and potentially bolster a USD bid. This, of course, would be emphasised if the next jobs report came in better-than-expected.

However, if PCE inflation comes in weaker-than-forecast, you can expect a further dovish repricing/lower USD.

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,