Everywhere you look there is criticism of central banks – Are they responsible for the mess we see now?

Outlook: This is a big data week. We get German CPI tomorrow and the eurozone on Wednesday, both expected up a notch. In the US, we get Jolts tomorrow (10.475 million forecast), the ADP estimate of private sector jobs and the real thing on Friday, probably a slowdown from 528,000 in July to 300,000 new jobs in August. ADP (Wednesday) has been away for a few months tidying up its data bases (or something) and we admit we didn’t miss it.

As for a recession reading, we get the Dallas and Chicago regional Fed reports but the important figure will likely be the ISM manufacturing PMI for August on Thursday. It’s forecast down at 52.0 from 52.8 in July but not below the boom/bust line of 50, which is what we got from the S&P version last week. Prices paid might be interesting.

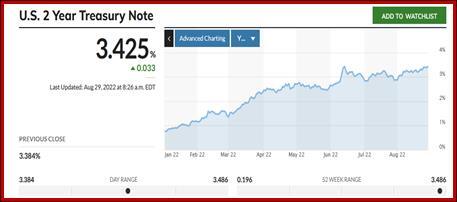

As we saw in the recent past, Powell’s speech is going to get parsed to the bone this week. We say it doesn’t need much interpreting–it was clear as can be. We know because two-year Treasury yield rose to the highest since 2007. The chart is year-to-date.

Powell’s speech at Jackson Hole on Friday was notable for a few things, starting with its brevity–less than ten minutes. That’s a message in its own right–get it right this time, people.” “People” is not the term Powell had in mind, of course.

Powell emphasized that bringing inflation down is the first priority, even if that brings “some pain” in its wake. He mentioned Volcker, in case the dovish wishful thinkers might miss the message. In fact, they tried to see it that way in the first few minutes and it was fascinating to watch the yields, equity indices and dollar gyrate wildly on the Bloomberg TV screen. Wall Street finally got the message and the Dow fell over 1000 points. (Note that in Europe, the ECB is naming it “sacrifice.”)

Everyone knew exactly what he meant by “some pain”–squeezing businesses that need to borrow so much that they lay off workers and/or stop hiring new ones. In a word, unemployment. The Fed can’t reconcile unemployment at historic lows with a slowing economy that will cut demand and therefore inflation. It’s more complicated than that, of course (can the Fed somehow raise the participation rate, for example?), but that’s the bottom line. The Fed will keep at it “until the job is done,” meaning a rise in unemployment AND decline in inflation. Don’t forget the unemployment comes first and inflation lags by as much as 6-9 months, maybe more. Those who expect a rate cut in 2023 are doomed to disappointment, although a few seem to be still around.

Powell said the size of the September hike hinges on the totality of the data; the July data was welcome but the Fed needs to see more.

Powell promised to “use tools forcefully” and to take “forceful and rapid steps,” which likely means 75 bp at the Sept policy meeting plus another 100 bp before year-end. There’s not a dovish gene in this animal. And in case there are any still wishing for a dovish message, we have a parade of Feds this week to reinforce the Powell narrative. Today brings Brainard, tomorrow brings Barkin and Williams; Wednesday it’s Mester and Bostic, and the list is not complete. New Dallas Fed president Logan may stick his toe in the water, too.

Everywhere you look there is criticism of central banks–do they fall into line when a president or prime minister leans on them (the autonomy issue)? Are they responsible for the mess we see now or can we blame Putin? As for blaming fiscal policy–all those handouts–there is a germ of truth in there but the total deficit is falling, not rising, and it doesn’t matter anyway–the Fed claims responsibility for managing inflation and has no say over fiscal matters.

We wonder if a new issue is not about to appear–a central bank raising rates when a recession has already shown its face--? This is the problem in front of the ECB, which meets next week on Sept 8. One plausible reason for the euro to resist falling (and hard) is that there is chatter (from Austria and the Netherlands) of a 75 bp hike instead of the 50 bp already hinted. One report says there is a 50% chance of 75 bp.

But eurozone inflation is going to go up, not sideways or down. For the eurozone as a whole, headline CPI is forecast up to 9.0% y/y from 8.9% and core to 4.1% from 4.0%. Spain is likely to get 10.5%, and Germany, 8.8% (from 8.5%), France and Italy will get some relief from July but remain scary high (France 6.7% and Italy, 8.2%).

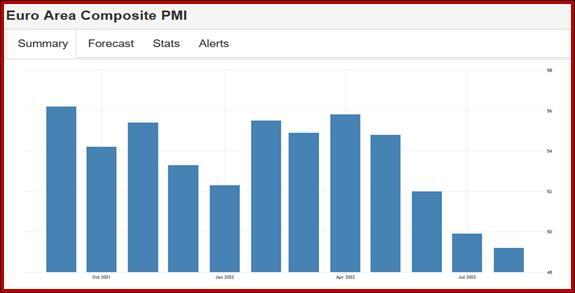

Whether the ECB raises rates by 50 bp or 75 bp on rising inflation, it’s still confusing to have rate hikes when the economy is so clearly trending downward. The S&P composite PMI last week fell to 49.2 in August from 49.9, better than forecast but still below 50. The chart from Trading Economics says it better than words. And we still don’t know the final effect of climate damage and energy costs. In a nutshell, there is no reason whatsoever to go long the euro and stay there. We should see spikes in the euro to relative highs as positioning-driven aberrations. Chances are good any new highs in the pound should be viewed the same way, especially now that the public is girding its loins to refuse to pay the new energy costs, inflation will exceed 13.2% and the country is likely to get a new PM without the technical know-how to design a solution.

Political Tidbit: If you or I or anyone else stole government documents, held them haphazardly in an unsafe place and lied about having them, we’d be in jail within days. It remains to be seen whether Trump will be indicted, and if he is indicted, whether it will make a bit of difference to his cult followers. Experts say it will not, because Trump supporters are more enthralled by sharing his grievances than committed to the law and the Constitution.

Somewhere in all the commentary–citing the perspicacious Evelyn Waugh, perhaps-- we found a breath-taking comparison. Trump is copying the political ploy of the British kings throughout history, although almost certainly unwittingly. The kings made allies of the general public against the lords of the realm, who so often tried to unseat them and sometimes succeeded. Think of today’s big businesses and capitalist cronies as the equivalent of the duke or this shire or the earl of that. Henry the 8th liked to don a non-royal disguise and mingle with the hoi-polloi; Queen Elizabeth the First had copies of her portraits distributed among the people. Princess Diana was the pinnacle of royalty showing empathy and support for the masses.

It has always seemed odd that Trump, who so obviously doesn’t give a fig about ordinary people (e.g., stiffing his contractors) got positioned as a “populist.” He’s not a populist but certainly a master at expressing grievance against the Establishment. That he then organized a giant tax cut for that same Establishment seems to go unnoticed in the hue and cry over his “unfair” treatment by another arm of that Establishment, the Justice Department. Silly point: if you give enough money to Trump now, you can get “Great Maga King Status.”

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat