Even if we buy into the inevitability of recession, we have no evidence the Fed will chicken out

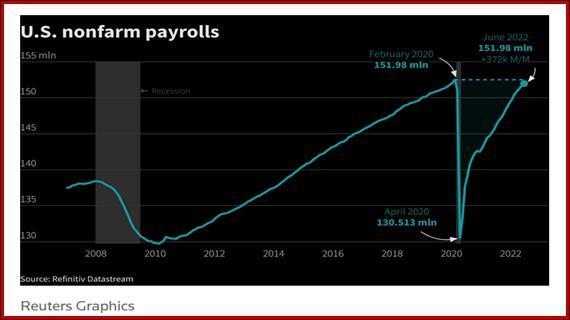

Outlook: Jobless claims rose by 6,000 on the weekly and 4-week moving average bases, not enough to impress one way or the other. Nonfarm payrolls will likely be a different kettle of fish, if only because players desperately want evidence that conditions are changing in response to the Fed’s massive hikes so far, with hiring decisions likely predicated on the expectation of more to come.

As usual, the price outcome depends on the contrast between the expected and the actual. The consensus is 250,000 but Trading Economics has 290,000 (vs. 372,000 last time), implying a significant drop–exactly what the Fed seeks. But if TE is right, it’s still a drop but perhaps not enough to convince the market the Fed will indeed be staying its hand come 2023.

We are surprised that the bond boys are sticking to the idea that evidence of recession sometime soon is going to spook the Fed and force it to retreat into halting hikes and even reversing direction in early 2023. Even if we buy into the inevitability of recession, we have no evidence the Fed will chicken out.

Oxford Economics agrees–Rates markets are pricing in too early a rate cut in the Fed funds rate in 2023H1, and too flat a path in 2023H2. Historically, rate cuts start at least half a year after rates peak and tend to fully reverse previous cumulated rate hikes, taking the target rate well below neutral.

“We see a more aggressive path for rates cuts than is priced in by markets, but only starting in 2023H2 as the Fed takes time to be comfortable with inflation trending lower.”

To confuse matters, the Bloomberg economists see recession “by the beginning of 2024 with 100% probability.” This implies resilience for another 12-15 months while the bond market’s dove camp wants super-bad data now so rate cutting can start a full year earlier than Bloomberg foresees.

Now that’s messed up. And while nobody doubts the yield curve will remain inverted for some time to come, the forecasts of peak inflation/recession arrival are all over the place. We see the 10-year yield creep up a bit and then collapse in the face of massive uncertainty.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat