Eurozone: A few reasons for the high saving rate

At the end of 2024, the household saving rate in the Eurozone was higher than it was before the COVID crisis. Among the four main economies of the Eurozone, France is no exception. Only in Spain and Italy has this trend been accompanied by an increase in investment in housing. In France and Germany, these additional savings are exclusively financial in nature. The factors at the root of the high financial saving rate will not prevent it from falling in 2025, but will contain it.

As a reminder, Keynesian theory defines savings as the portion of income that is not spent on consumption (gross saving in national accounts). The flow of gross saving is thus subdivided into a real component – investment in new housing – on the one hand, and a financial component – the share of gross saving not dedicated to investment in new housing – on the other. This is equal to the portion of income that is neither spent on consumption nor invested in new housing, in other words, the net lending position of households. Taking bank credit into account complicates the analysis somewhat, since credit flows are a resource, in the same way as income, likely to finance consumption, investment or financial investments. Under national accounting conventions, credit flows are treated as a negative use when calculating the saving rate: they are deducted from financial savings. As a result, the net lending position is in a sense the hinge between non-financial accounts and financial accounts. In theory it is equal to gross financial investment flows minus loans flows.

In France, since the third quarter of 2022, the proportion of their income that households spend on new investment has been falling, reflecting a fall in the real saving rate. This fall was initially offset by the rise in the financial saving rate until the end of 2023, but this has no longer been the case since 2024: the rise in the financial saving rate is greater than the fall in the real saving rate, leading to a rise in the overall saving rate. In the third quarter of 2024, this overall household saving rate stood at 18.2% of gross disposable income (compared with 17.2% in the fourth quarter of 2023), of which financial savings accounted for 8.8% (7.3%). That same quarter, in the Eurozone, the saving rate recorded its first fall after two years of uninterrupted rise (15.3% in the third quarter of 2024, after 15.6% in the second quarter and 14.6% in the fourth quarter of 2023).

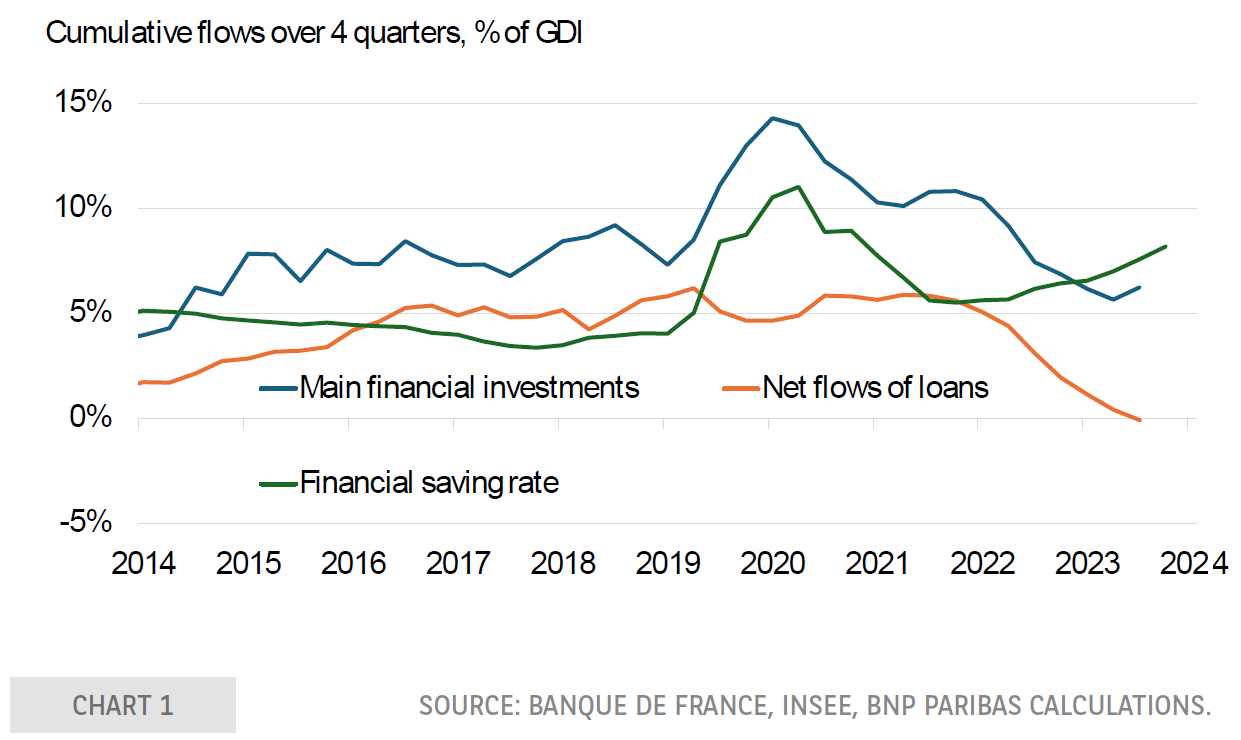

As our chart shows, the rise in the financial saving rate in France does not always coincide with the rise in financial investment flows (as a % of income, see chart). On the contrary, the latter have been falling since 2022 under the influence of the contraction in credit flows and the resulting decline in money creation.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.