“Europeanising” long-term individual savings

Speaking at a joint press conference in Germany on Tuesday, 28 May 2024, the French President and German Chancellor expressed their desire to create a “European savings product” to “bolster Europe’s competitiveness and growth”. This political will follows on from the Letta1 and Noyer2 reports and statements made by the French Minister of the Economy. It’s a new approach to getting Capital Markets Union back on the rails.

Households held around €29,800 billion in financial assets in the euro zone at 31 December 2023. Around one third (or close to €9,500 billion) of these savings was collected in the form of deposits and intermediated by banks as part of a risk and maturity transformation process to finance the so-called “real” economy, mainly in the form of loans and, to a lesser extent, in the form of debt securities held by banks. A second third (€9,200 billion) was allocated to equities and mutual fund shares. Lastly, a final third (€11,600 billion) was housed in life insurance and pension vehicles and invested in rate instruments.

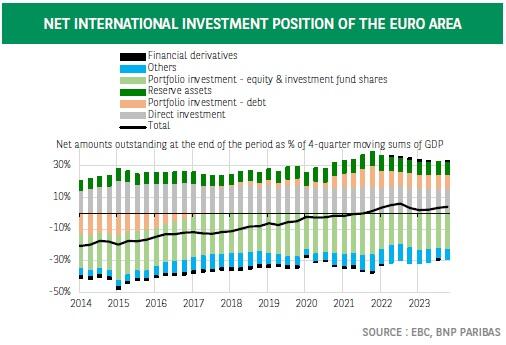

A large portion of these savings is “exported” outside the eurozone, while a fraction of European businesses’ equity is held by non-resident investors3. This paradox illustrates investors’ different preferences on either side of the Atlantic (see chart).

These capital movements certainly enable our open economies to raise finance in circumstances where closed economies would run into problems with investors’ local preferences, capital shortages or higher borrowing costs. But Europeans’ preference for lower-risk and lower-return assets is not without its consequences. Despite the euro zone’s more or less balanced net international investment position, non-resident investors capture greater value-added from the euro zone than that achieved by euro-zone investors in the form of returns on assets that they hold outside Europe’s borders.

It should also be noted that equity funding is a vital prerequisite for recently formed, innovative businesses to secure other external finance in debt form. It also enables more established businesses to finance large-scale projects, such as a disruptive technology. Innovation financing represents a source of European productivity and competitiveness gains and thus justifies the political desire to redirect European savings towards equity instruments. But savers cannot be commanded to want to invest in equities; they can merely be encouraged by tax incentives.In addition to the need for equity finance, future investments in the energy transition, the digital transition and artificial intelligence will create a growing need for long-term debt finance in the European Union.

There is a risk that interest rates will move higher in the event of insufficient long-term savings to cover these new needs. That’s why the right conditions need to be created upstream (through tax incentives for savings and by not overly constraining banks’ balance sheet with prudential requirements). Lastly, there’s a point that is crucial in our eyes (it’s been a feature of the European Commission’s line on Capital Markets Union since 2015 but was not addressed in the Noyer and Letta reports), and that’s risk sharing within the European Union. With such a mechanism in place, a country facing an idiosyncratic shock would suffer a smaller GDP contraction than the scale of the shock would suggest. The stabilising effect of revenue earned from financial assets issued in other Member States unaffected by the shock would help to smooth consumption4 to some extent.

The new European savings product would not represent a trial run for the European Commission. It would be perfectly aligned with the European Long-Term Investment Fund (ELTIF) introduced in 20155 and the Pan-European Personal Pension Product (PEPP) set up in 20196. The ELTIF aims to raise long-term financing for infrastructure projects, unlisted companies and listed SMEs, which issue equity or debt instruments. The PEPP, which targets retail savers, features a high level of flexibility (option of exiting with an annuity, capital or a combination of both), capped management and transfer fees and portability if a saver moves from one EU Member State to another. Given the failure of the PEPP initiative, the Noyer report calls for a decentralised (i.e., “national”) approach in the future European savings plan. It advocates for a European quality label, which could be awarded to funds – new or existing vehicles with suitable characteristics and meeting pre-agreed eligibility criteria.

Six core principles were laid down in the report: an investment horizon far into the future (maturity at retirement with scope for an earlier exit in similar circumstances to the French PERECO plans7 ), exposure to risk (possible capital guarantee but solely at maturity, excluding in the event of an early exit), guided management by default, membership by default for employees with an opt-out, a preferential tax regime (deductible from taxable income up to certain limits or a tax credit, or alternatively a partial tax exemption on exit gains, favourable treatment under inheritance law). In the absence of tax harmonisation, the product is likely to benefit at least from the most favoured tax treatment applicable in each Member State. Lastly, since the goal of these products is to channel European household savings into meeting investment needs within the EU, a minimum allocation of 80% to European assets is recommended.

While the 27 Member States have struggled to agree on securitisation, tax harmonisation or bankruptcy law, a consensus seems to emerge for the time being in favour of this European savings product. At long last, that could give the new-look European Commission after the June elections the chance to take a step towards Capital Markets Union.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.