Europe and the potential to go back into recession

European stock markets have traded cautiously mixed so far today. The GER30 is currently up 0.03% and the UK100 down -0.27%, while US futures are posting fractional losses. The US markets are closed for Martin Luther King Jr Day today, which is making for quieter trading conditions as investors are also questioning how much of Biden’s stimulus program will survive the approval process.

At the same time, new Covid-19 infection numbers may be falling and vaccination programs gathering steam, but hospital admissions and death counts remain high and there are still considerations to tightening social distancing restrictions even further, as officials are increasingly concerned about new mutations that may complicate the response. Better than expected GDP numbers out of China, which reported a solid expansion in economic activity last year, despite Covid-19, saw the CSI 300 and Hang Seng moving up 1.1% and 1.0% respectively.

European political developments

In Italy, the PM is facing a series of confidence votes this week and the wrangling in Rome over the use of recovery funds and the possible tapping of ESM monies to boost the healthcare system during the pandemic doesn’t bode well for the recovery that the EU’s recovery program is supposed to fund. Meanwhile the Dutch government resigned at the end of last week, although that will have little immediate consequence as an election is scheduled for next month anyway and the current government will stay on for now as caretaker. In Germany political developments have also dominated headlines over the weekend, as Merkel’s CDU voted in a new party leader, who will also have a strong claim to succeed Merkel as candidate for the next general election in autumn.

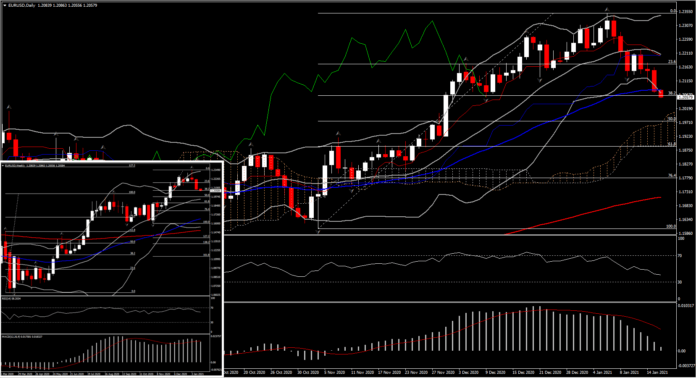

EURUSD is down again, earlier posting a near 7-week low at 1.2054, which extends a 2-week run lower. The pair has corrected from the 33-month peak that was seen last week at 1.2350. This has in part been a consequence of the Georgia runoff elections, which unexpectedly resulted in the Democrats taking control of the Senate, and which culminated in the President-elect confirming a massive $1.9 tln fiscal spending package. This raises prospects for both growth and inflation in the US economy, and, despite protestations from Fed policymakers in recent days, will bring monetary policy tightening nearer than it would have otherwise have been.

While the budget and trade deficits will shoot higher, the domestic economic stimulus should draw in foreign capital. That said, the global inflation trade, should it unfold (hinging on a return to societal normalcy this year), should still see the US Dollar weaken, given the relative value to be had in global markets compared to richly valued US assets.

As for the Eurozone, much of Europe is in a state of lockdown that, while less severe than the ‘mother’ lockdown last year, has the potential to send the economy back into recession. Italian politics has again flared up with a junior partner pulling out of the governing coalition, leaving Prime Minister Conte without a majority in government. The ECB’s board meets on monetary policy this week (Thursday). After the PEPP and TLTRO programs were bolstered in December, the central bank is unlikely to further top up the existing policy. The transformation of the PEPP volumes into a ceiling rather than a target has given the ECB some flexibility, although governments hooked on low rates will likely increase the pressure on the central bank not only to use PEPP in full but also to push out the end date of the program as far into the future as possible.

Markets will watch for comments on the Euro and the future of the inflation target amid the ECB’s ongoing strategic policy review.

Author

Having completed her five-year-long studies in the UK, Andria Pichidi has been awarded a BSc in Mathematics and Physics from the University of Bath and a MSc degree in Mathematics, while she holds a postgraduate diploma (PGdip) in