EUR/USD Price Forecast: Looking at US CPI rather than the ECB

- EUR/USD alternated gains with losses around the 1.1700 region on Wednesday.

- The US Dollar also traded in a vacillating mood amid declining US yields.

- The ECB is expected to keep its interest rates unchanged on Thursday.

The Euro (EUR) went nowhere fast on Wednesday, with EUR/USD stuck around the 1.1700 mark. The lack of momentum mirrored the US Dollar (USD), which also drifted as traders kept to the sidelines ahead of Thursday’s US CPI report and the European Central Bank (ECB) meeting.

The US Dollar Index (DXY) couldn’t build on Tuesday’s gains, remaining subdued after US Producer Prices undershot forecasts and speculation of a Fed rate cut at the September 16–17 meeting held steady.

Trade tensions cool, but tariffs still sting

Global trade nerves eased a little after Washington and Beijing extended their truce for another 90 days. President Trump delayed tariff hikes until November 10, and China held fire in return. Still, most levies remain in place: US imports from China are taxed at 30%, while Chinese shipments to the US face a 10% charge.

Washington also inked a new deal with Brussels. The EU agreed to cut tariffs on US industrial goods and widen access for American farm and fisheries products. In exchange, Washington slapped a 15% tariff on most European imports. In addition, car tariffs could follow, depending on upcoming EU legislation.

French politics add to eurozone uncertainty

Politics grabbed the headlines in Europe. French Prime Minister François Bayrou lost a confidence vote on Monday and handed in his resignation to President Emmanuel Macron on Tuesday, reviving political jitters in the bloc’s second-largest economy.

Fed keeps September cut firmly on the table

The Fed left rates unchanged at its last meeting, with Chair Jerome Powell pointing to risks in the labour market but noting inflation remains above target. That keeps the door wide open for a cut this month.

Weaker US Producer Prices reinforced that view, as did Tuesday’s revision of Non-Farm Payrolls by the Bureau of Labor Statistics (BLS), which showed the economy created 911K fewer jobs in the 12 months through March than initially reported.

Markets are still leaning towards a 25 bps cut on September 16–17, though bets on a bigger move are inching higher.

ECB expected to hold fire, Lagarde in focus

The ECB is widely expected to keep interest rates unchanged on Thursday. Markets will zero in on President Christine Lagarde’s press conference for any hints on the bank’s policy path. The release of the ECB Staff Macroeconomic Projections will also be closely watched.

Euro longs shrink

Positioning data from the Commodity Futures Trading Commission (CFTC) showed non-commercial net longs in the Euro slipping to two-week lows near 119.6K contracts in the week to September 2. Institutional net shorts eased to 171.3K, while open interest climbed for a fourth straight week to around 846K contracts.

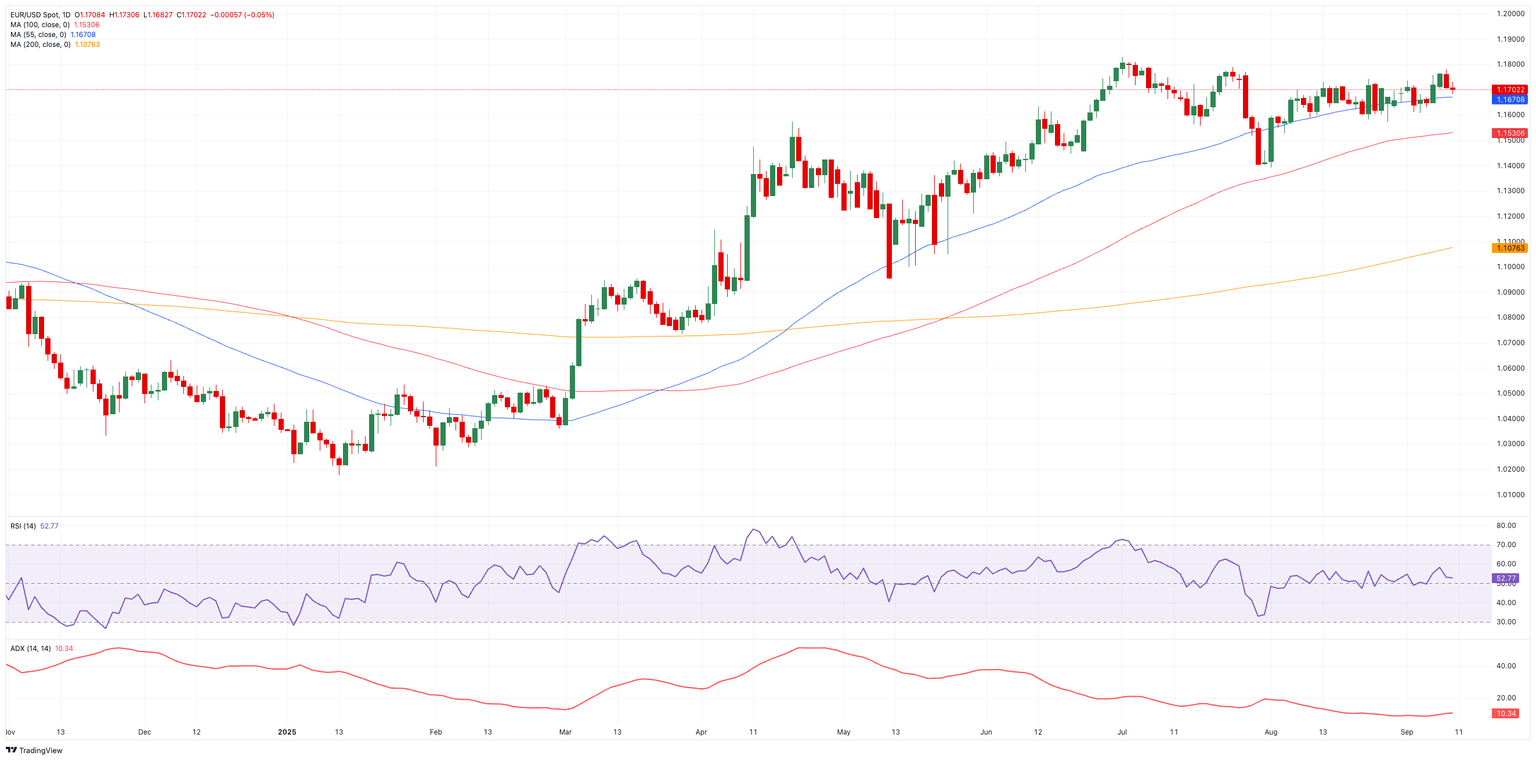

EUR/USD technical outlook: still rangebound

EUR/USD remains boxed into a wide 1.1400–1.1800 range. On the topside, resistance sits at the September high of 1.1779 (September 9), then the weekly peak at 1.1788 (July 24), followed by the 2025 ceiling at 1.1830 (July 1). A breakout above would bring the September 2021 high of 1.1909 into view, with the psychological 1.2000 level further ahead.

Short-term support lies at the 100-day Simple Moving Average (SMA) at 1.1535, prior to the August trough at 1.1391 (August 1) and the weekly floor at 1.1210 (May 29).

Momentum signals continue to show a mixed outlook: the Relative Strength Index (RSI) has eased back towards 53, suggesting buyers are still hanging on, while the Average Directional Index (ADX), near 12, is indicative that the current trend lacks muscle.

EUR/USD daily chart

What’s next for EUR/USD?

For now, EUR/USD looks set to stay in consolidation mode. It will likely take a fresh catalyst, whether from US data, a firm move by the Fed, or another twist in trade policy, to break the pair out of its range.

ECB FAQs

The European Central Bank (ECB) in Frankfurt, Germany, is the reserve bank for the Eurozone. The ECB sets interest rates and manages monetary policy for the region. The ECB primary mandate is to maintain price stability, which means keeping inflation at around 2%. Its primary tool for achieving this is by raising or lowering interest rates. Relatively high interest rates will usually result in a stronger Euro and vice versa. The ECB Governing Council makes monetary policy decisions at meetings held eight times a year. Decisions are made by heads of the Eurozone national banks and six permanent members, including the President of the ECB, Christine Lagarde.

In extreme situations, the European Central Bank can enact a policy tool called Quantitative Easing. QE is the process by which the ECB prints Euros and uses them to buy assets – usually government or corporate bonds – from banks and other financial institutions. QE usually results in a weaker Euro. QE is a last resort when simply lowering interest rates is unlikely to achieve the objective of price stability. The ECB used it during the Great Financial Crisis in 2009-11, in 2015 when inflation remained stubbornly low, as well as during the covid pandemic.

Quantitative tightening (QT) is the reverse of QE. It is undertaken after QE when an economic recovery is underway and inflation starts rising. Whilst in QE the European Central Bank (ECB) purchases government and corporate bonds from financial institutions to provide them with liquidity, in QT the ECB stops buying more bonds, and stops reinvesting the principal maturing on the bonds it already holds. It is usually positive (or bullish) for the Euro.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.