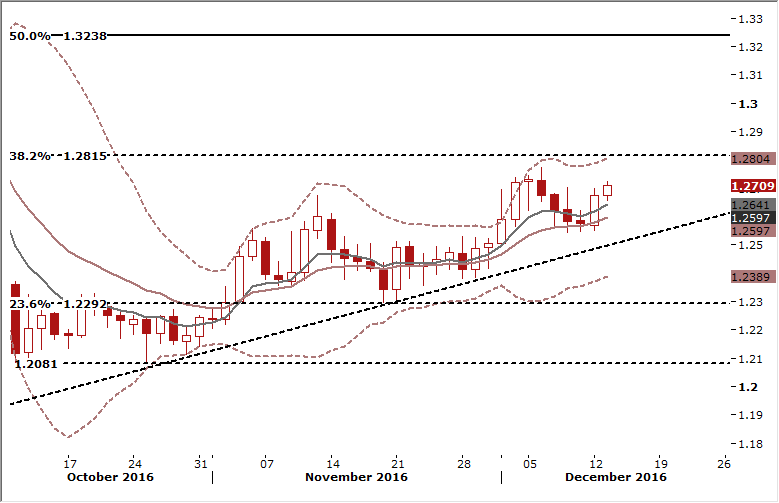

EUR/USD: Focus turns to Fed statement on Wednesday

-

Italy is ready to pump capital into Monte dei Paschi di Siena if the ailing bank fails to get the EUR 5 billion it needs to remain in business from private investors. "If the operation failed, the state would carry out a precautionary recapitalisation," the Treasury source said. "The bank's existence and its clients' savings will be preserved under any circumstances."

-

Italy's third-biggest bank is pressing ahead with a last-ditch attempt to raise the cash on the market this year despite a government crisis triggered by Prime Minister Matteo Renzi's resignation following his defeat in a December 4 constitutional referendum. However, its chances of success are slim and the state is likely to have to step in to make up for the shortfall.

-

The bank had sought a three-week extension to January 20 from the European Central Bank of a deadline for completing its capital raising plan, citing the political turmoil. However, this was rejected on the grounds that a delay would be of no use and it was time for Rome to step in.

-

The EUR/USD rose slightly helped by higher German bund yields and on relief as Rome was seen ready bail out Monte dei Paschi di Siena.

-

The Federal Reserve will finally pull the trigger again and raise its target rates by 25bp on Wednesday. With economic numbers coming in on the stronger side of expectations, a rate hike next week is a done deal. With a rate hike being fully priced in, the focus will be on the statement and the updated summary of economic projections. While financial markets have gotten excited about the prospects of fiscal stimulus by the incoming administration, we expect that FOMC members won’t incorporate such a scenario into their forecasts until it has been approved. As a result, there is not much need at the moment to materially alter the forecasts for GDP growth (2% in 2017 and 2018) or the inflation rate (moving towards 2%). The path for the unemployment rate could be adjusted downwards a bit, after last week’s sharp drop in the jobless rate to 4.6%, which has been the Committee’s median projection for year-end 2017.

-

We do not expect any major changes to interest rate projections (the “dots”). Instead, we anticipate that the median dots continue to indicate a gradual normalization of policy rates throughout the forecast period, with two hikes in 2017 and another three hikes in 2018. Amazingly, this would be the first time that the median dot for year-end 2017 would remain unchanged. Since the 2017 forecasts were first introduced in September 2014, the median dot for year-end 2017 has been lowered with each forecast update. The median dot for the longer run natural rate will most likely come down further to 2.75% from 2.88%, as it only needs one single Committee member to lower his or her forecast to move the median number.

-

In our opinion no position is justified on the EUR/USD from the risk/reward perspective. Technical analysis signals are mixed. Long tail on December 5 large candlestick signaled a massive rejection of downside, but this has subsequently been overwhelmed by upside rejection last Thursday.

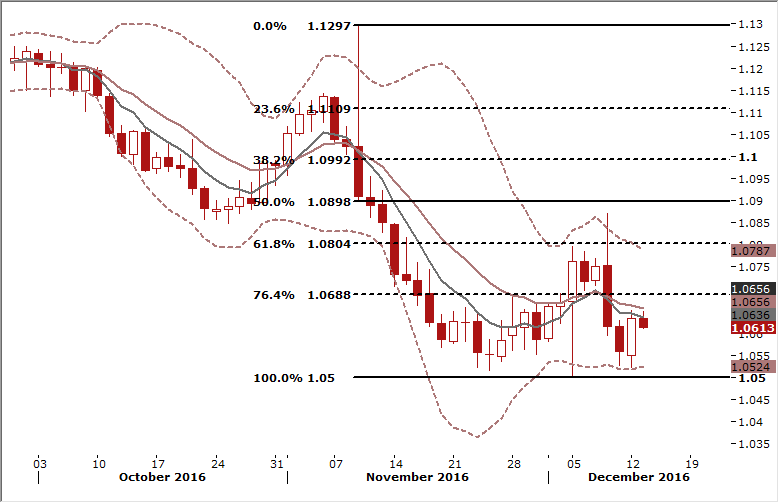

GBP/USD: Highest inflation since October 2014

-

British finance minister Philip Hammond on Monday backed the idea of a transition period to smooth the process of leaving the European Union, and said EU countries also stood to gain from a gradual Brexit. He reiterated his view that Britain's future controls on the flow of workers from EU countries should not cut off the supply of skilled staff needed by British firms.

-

Hammond's remarks are the latest to strengthen investor hopes for a "soft Brexit" that prioritises maintaining strong economic ties with Europe over the need for strong immigration controls.

-

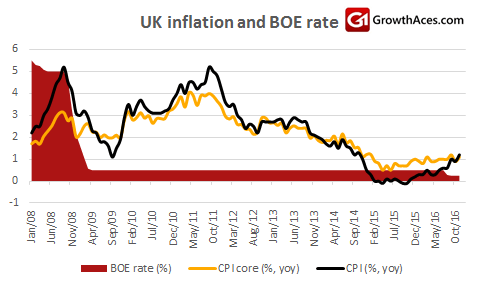

The Office for National Statistics said that consumer prices rose 1.2% yoy in November, above market expectations for a 1.1% rise. Inflation accelerated from 0.9% yoy in October.

-

Last month the Bank of England forecast that inflation would surge to about 2.8% by mid-2018, as sterling's big fall after Britain's vote to leave the EU pushes up the cost of imports. BoE Governor Mark Carney has said the central bank could tolerate some overshoot against its 2% inflation target, to help accommodate economic growth and employment.

-

British factory gate prices rose at an annual rate of 2.3% in November, the biggest since April 2012, compared with forecasts of a 2.5% annual increase. Prices paid by factories for materials and energy fell more than 1% on the month but were up by nearly 13% compared with November 2015 - the biggest annual increase since October 2011.

-

The Office for National Statistics also released figures for house prices in October which showed an 6.9% annual rise across the United Kingdom as a whole compared with 7.0% in September.

-

The GBP/USD is strengthening today after Hammond argued for staggered Brexit and after higher-than-expected inflation figures. Last-week corrective move was quite shallow, which highlights upside potential of this pair. Macroeconomic fundamentals suggest the GBP/USD is likely to appreciate also in the long term. We have placed our bid at 1.2620.

Author

Growth Aces Research Team

Growth Aces

GrowthAces.com is an independent macroeconomic consultancy. They offer you daily forex analysis with forex signals for traders.